Preparing for an Inflationary Soft Landing

Investors need to consider that we may be entering a period not seen in the developed world in decades, similar only to those experienced in emerging markets.

Swan Bitcoin Market Update #43

This Insight Report was originally sent to Swan Private clients on November 10th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

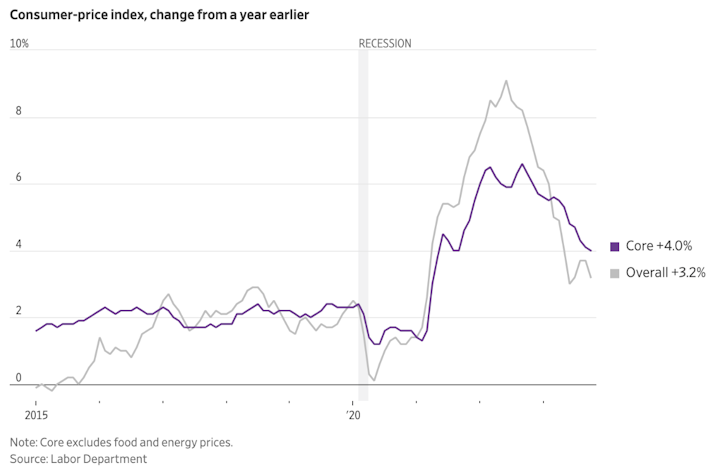

The highlight in markets this week came on Tuesday when October’s CPI data was released, showing year-over-year inflation had fallen more than expected. Furthermore, Core CPI — CPI minus food and energy — declined to its lowest level since 2021.

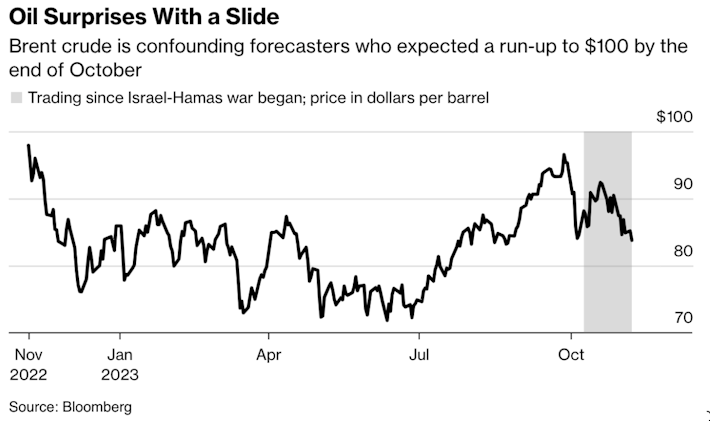

Much of the decline was attributed to falling energy prices. After many months of upward price pressure, the price of crude oil has sold off over the last month to the surprise of many market participants.

In the wake of this CPI print, investors everywhere began to wonder once again if the Fed had accomplished the impossible — bringing down inflation without causing a significant recession. This is the coveted “soft landing” that everyone has been talking about.

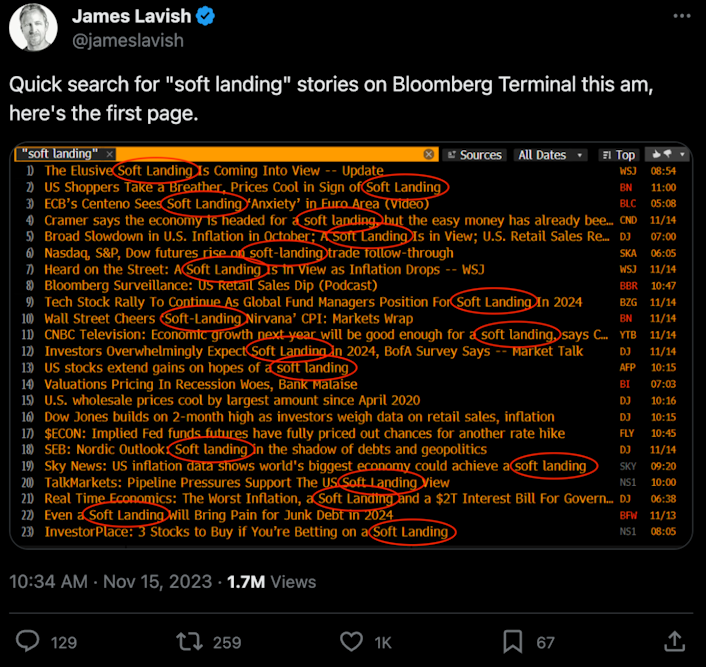

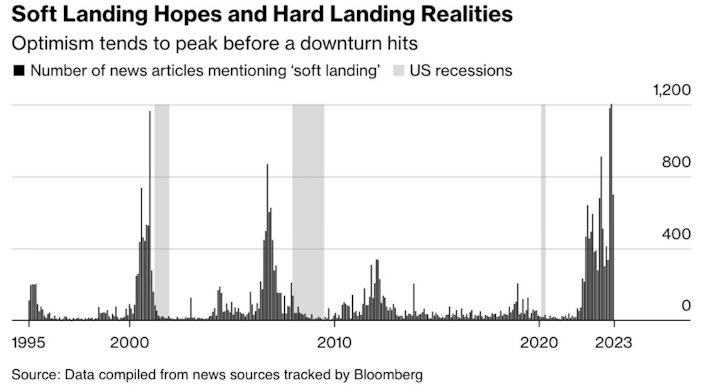

James Lavish highlighted below how mentions of “soft landing” littered his Bloomberg Terminal in the aftermath of the CPI release.

If this truly is a “soft landing, ” then the Fed has achieved something extraordinary. It has raised interest rates at one of the fastest paces in history in a highly leveraged economy without causing a significant recession. But is this just hopeful thinking?

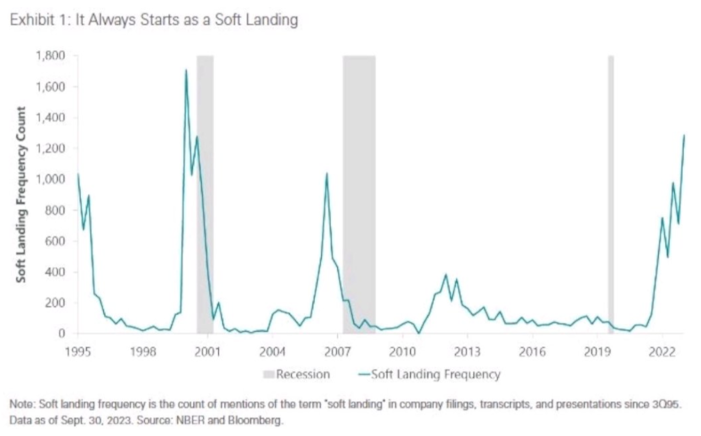

Below is a chart that analyzed mentions of “soft landing” in company documents and filings dating back to 1995. It found that the frequency of soft landing mentions has only spiked to these levels on two previous occasions, 1) Right before the Dot Com Crash, and 2) Right before the Global Financial Crisis.

Bloomberg shared a similar chart that shows how investor optimism about a “soft landing” tends to peak right before an economic downturn hits.

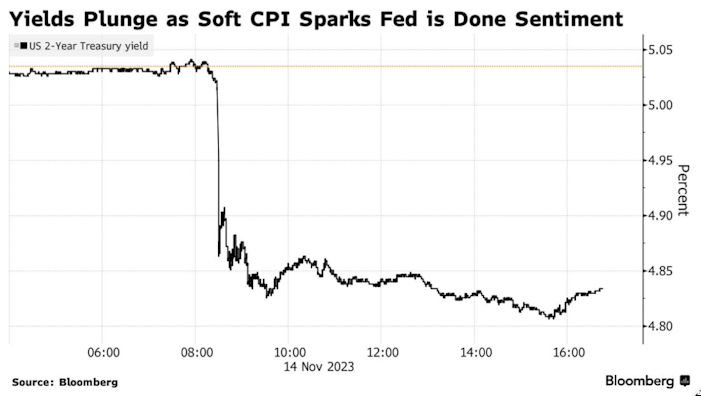

Nonetheless, investors saw this latest CPI as a sign that the Fed is likely done with rate hikes and, as a result, bonds and stocks have both rallied.

We saw yields drop across the entire yield curve as the market began to price in an increased probability that the Fed has reached the end of its hiking cycle.

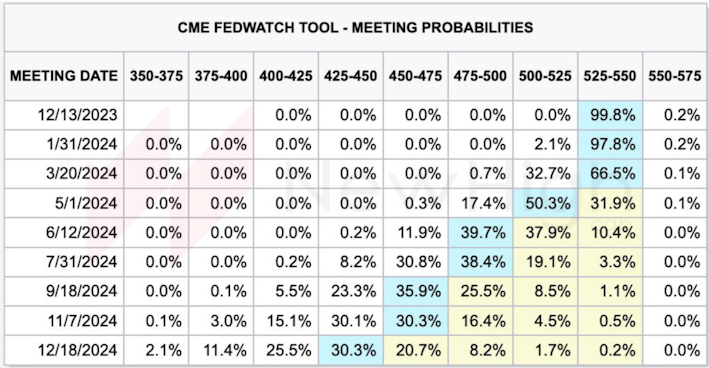

The futures market shows that investors are assigning nearly a 0% probability of another rate hike, with rate cuts set for May 2024. Before this CPI print, there was a 30% chance of another hike. The market thinks the Fed is done.

If the Fed is done with hikes, then investors might find current bond yields attractive. If this is the top for rates, then investors can lock in the high yield and then benefit from any rate cuts in the future if a deflationary recession does hit.

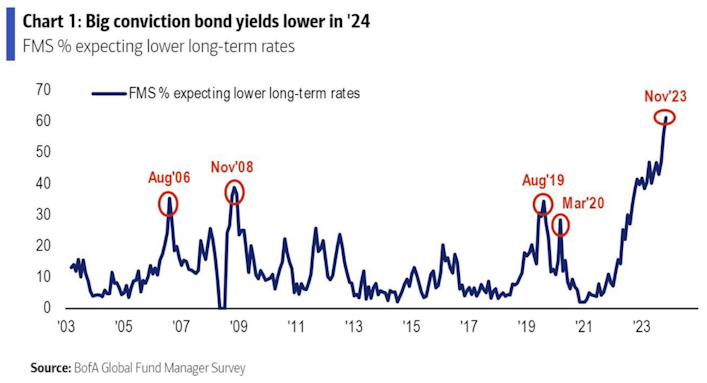

Right now, the market has high conviction that bond yields will be lower next year.

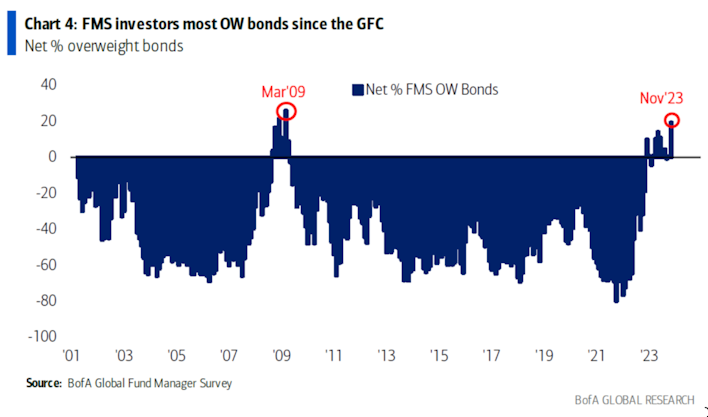

You also see this in the market’s positioning. Today, investors are the most overweight bonds than they have been since the Global Financial Crisis.

These investors are probably aware of what happens after the Fed finishes a hiking cycle. On average, it takes 8 months from the last Fed hike to the first Fed cut. That takes us to around May.

But are bonds really where investors want to be allocated to for the long term? These investors appear to be making a short-term trade that will capitalize on a Fed pivot in response to some future deflationary downturn. They are effectively trying to pick up pennies in front of a steamroller. But the question all of these investors overweight in bonds should be asking themselves is, “What if we are about to enter an inflationary recession, something not seen since the 1970s? What will yields do then?”

In recent memory, during a financial crisis, long-dated bonds have rallied as inflation collapsed. But what if bond yields remain elevated or even start climbing as inflation remains sticky? At that point, investors will begin to ask themselves, “Do I really want to lend money to a highly-indebted government running multi-trillion dollar deficits with inflation still at 4% for the next 30 years at these rates?”

The answer is probably not — at least not at these yields. They will demand higher rates for the amount of risk they are taking.

If long-dated bond yields rise in that scenario, then investors playing the Fed pivot will find themselves in a world of pain. Moreover, there are structural inflationary pressures that could keep inflation elevated even if the Fed begins to cut rates such as demographics, reshoring of supply chains, excessive government spending, and underinvestment in energy and infrastructure.

What investors need to consider is not that we may be having a “soft landing” or a “hard landing, ” but rather if we will have an “emerging market-style landing” as Lyn Alden alludes to in the Tweet below.

What does she mean by this? It means that you could have a situation where the United States never sees a true “hard landing” because policymakers are implementing an emerging market playbook.

Here’s what you could expect to see:

Excessive deficit spending

Rising bond yields

Currency debasement

Elevated inflation

Hot nominal growth, low real growth

Highly politicized monetary and fiscal policymaking

Weakening rule of law

Sound familiar? The Treasury is already running massive fiscal deficits, effectively running the emerging market playbook. If this continues, then inflation will remain elevated, and bonds will continue to underperform.

Another sign that we are divulging into an emerging market occurred this week when US Senator Markwayne Mullin and President of the Teamsters union Sean O’Brien almost got into a fistfight during a Senate hearing. This is the highly politicized economic decision-making that you often see in Emerging Market economies.

If the United States continues to function like an emerging market, then we should expect an emerging market-style investing environment — aka high amounts of government spending, increased uncertainty and civil unrest, and elevated levels of inflation.

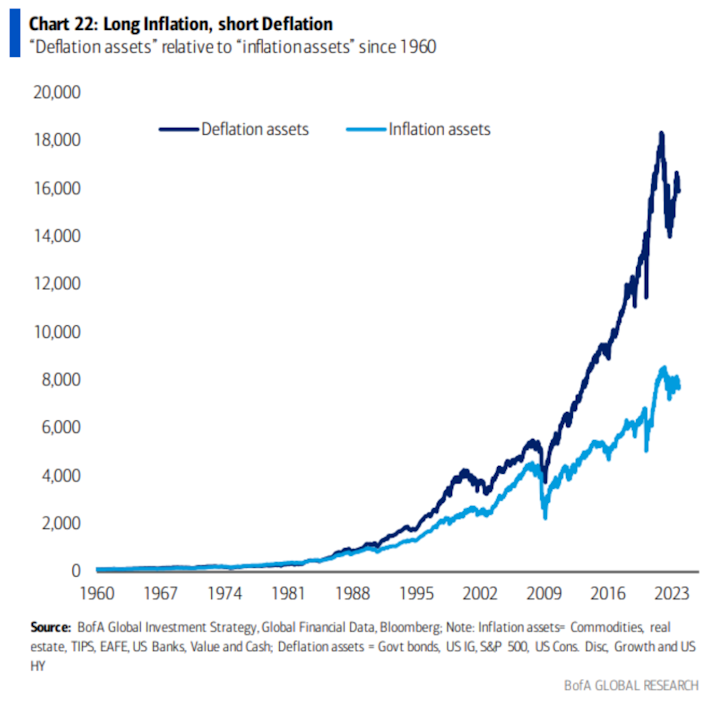

In that potential future, it is inflationary assets like commodities, real estate, precious metals, and Bitcoin that will likely outperform “deflationary assets” like bonds.

It’s not too crazy to think that inflationary assets will finally get their time in the sun given the last several decades. For the last 40 years or so, deflationary assets have significantly benefited from interest rates steadily falling. This long-term trend could all be changing.

If you believe in contrarian bets, then this next chart is for you. It highlights the relative price of real assets versus financial assets since 1925. You can see how we are at historic lows when it comes to the price of real assets against financial assets, that it appears to be carving out a bottom since 2021, and that the prices of real assets tend to spike during periods of increased geopolitical and economic uncertainty.

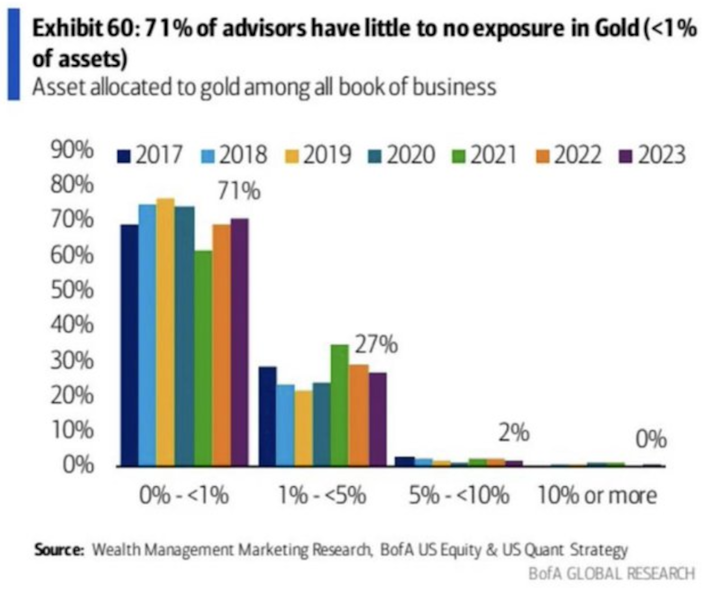

Further evidence that investors are woefully underallocated to real assets can be seen in the percentage of advisors with exposure to gold. A recent survey from Bank of America found that 71% of financial advisors have little to no exposure to gold.

This survey shows that there could be significant opportunity in the future if macro conditions provide a tailwind for real assets and asset managers begin to shift their allocation strategies in response to a sustained, inflationary environment, causing large inflows into these underallocated assets.

And what real asset has a value proposition like Bitcoin? Bitcoin has an investment case similar to gold given its scarcity and resistance to inflation and censorship, but also has the growth potential of a young tech stock.

Furthermore, just when the market expects the Fed to resort back to accommodative policies like rate cuts and Quantitative Easing, Bitcoin will be undergoing another halving.

If the timing aligns, then the contrast between the two monetary systems will once again be on full display. Whereas one monetary system will continue to debase the value of the money, the other will continue to preserve the scarcity that allows it to hold its value over time.

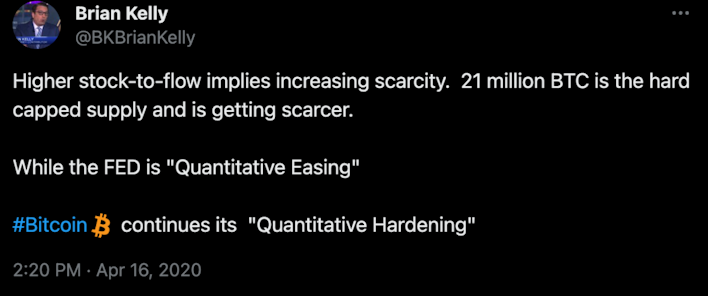

This occurred in 2020 when the Fed responded to the pandemic with massive Quantitative Easing programs and the Bitcoin halving occurred simultaneously.

This stark contrast between the monetary systems wasn’t even lost on CNBC hosts like Brian Kelly.

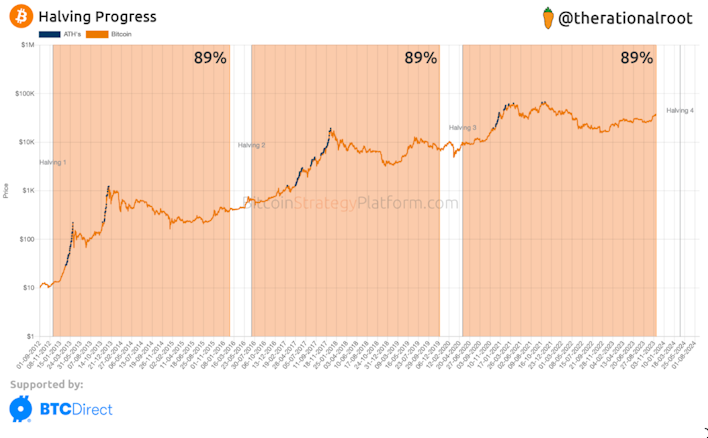

We are currently 89% through this current halving cycle. If the market is correct, we could be experiencing Bitcoin’s fourth halving right as the Fed has to pivot in response to some economic downturn.

If the Fed does begin cutting rates and inflation remains high due to public officials implementing emerging-market style policies, then Bitcoin could shine at that time.

Historically, long-dated bonds have been a place of refuge for investors. Today, we are seeing market participants pile into bonds as they expect the Fed is done with rate hikes, and a recession could be near. However, investors need to consider that we may be entering a period not seen in the developed world in decades, similar only to those experienced in emerging markets. In that world, in the long term, it is real assets like Bitcoin that will provide safe haven for investors, not paper financial products like bonds, no matter what the Fed decides to do with interest rates.

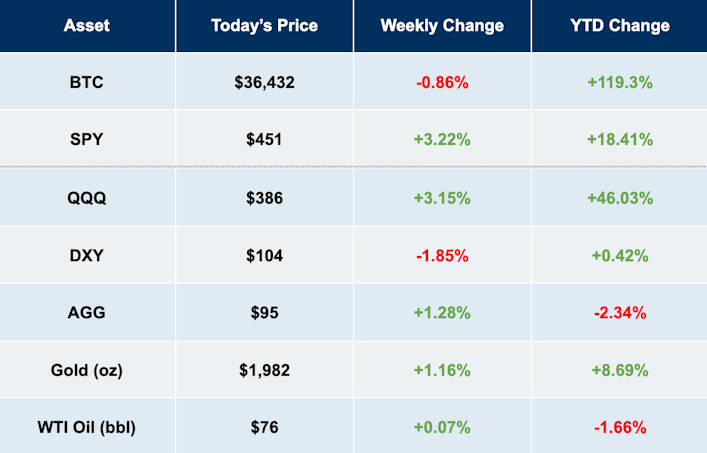

Market Overview

Tradingview, Prices as of 11/17/23

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

More from Swan Signal Blog

Thoughts on Bitcoin from the Swan team and friends.

Running the Numbers: How Fiat Pushed the American Dream Away from Millennials

Bitcoin symbolizes hope for a generation who increasingly feel as though their futures have been stolen from them by the traditional fiat system.

Best Bitcoin ETF Fees: Lowest to Highest (May 2024)

In this guide, we analyze and present the top 10 Bitcoin ETFs with the lowest fees for cost-effective investing.

Privacy, Executive Order 6102 & Bitcoin

Let’s keep pushing forward for the future we want to see, one in which both the price of Bitcoin and global freedom can go up together.