In this article

Ever since President Trump delivered his keynote address at the Bitcoin 2024 Conference in Nashville, discussions about a Strategic Bitcoin Reserve have dominated the internet, igniting debates about the role of digital assets in national reserves. At the same time, the broader digital asset community has been actively lobbying for inclusion in any future reserves. On March 2, 2025, President Trump took to social media and provided a glimpse into the current thinking of the administration by announcing his intent to establish a Crypto Strategic Reserve consisting of Bitcoin, Ethereum, XRP, Solana, and Cardano.

This decision initially seemed to mark the beginning of a broad nation-state accumulation of digital assets, placing several digital assets alongside traditional reserves such as gold and foreign currencies in global financial strategies.

This announcement raised many fundamental questions:

How have these assets performed over multiple market cycles?

What role should each asset play in a sovereign reserve strategy?

What makes an asset strategic, and what ethical considerations exist?

Does Bitcoin’s unique properties make it a truly superior reserve asset?

Then, on March 6, 2025, the tone shifted with the announcement of the “Establishment of the Strategic Bitcoin Reserve and United States Digital Asset Stockpile” Executive Order. The split between the assets in the announcement signaled a clear delineation in how the administration views them. The treatment of each is what truly made the line in the sand clear.

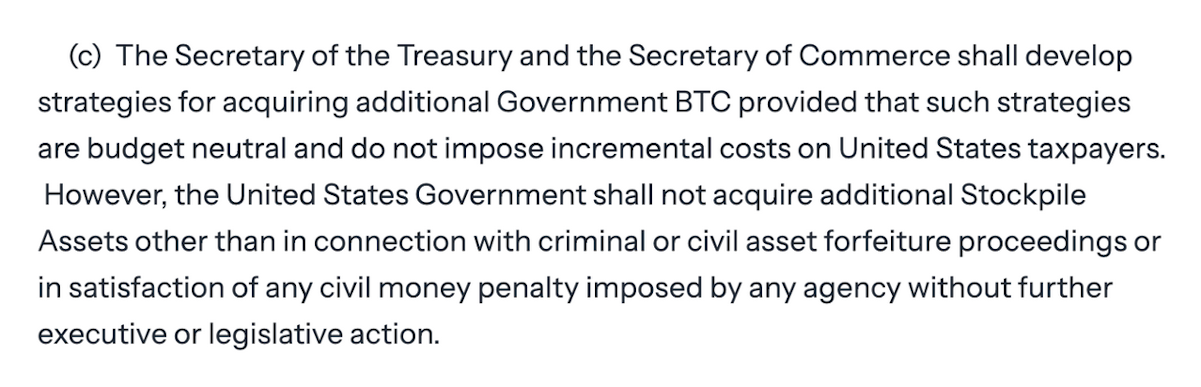

The Bitcoin Strategic Reserve establishes that Bitcoin in the Reserve shall not be sold. It also authorizes the Secretaries of Treasury and Commerce to develop budget-neutral strategies for acquiring additional Bitcoin as long as those strategies impose no incremental costs on American taxpayers. Perhaps more interesting is the use of the word “shall” in the phrasing.

While this may just seem like semantics to many, the use of “shall” in Section 3© of the executive order informs the Secretaries this is not optional, they are required to develop these strategies. It clearly signals an intention to add Bitcoin to the reserve over time. There are no such provisions for the Digital Asset Stockpile.

This clear differentiation is deafening. It tells the world that Bitcoin is truly strategic as a reserve asset, with The White House going as far as educating the world that Bitcoin is Digital Gold and elaborating on the benefits of a fixed supply. Additionally, it was even highlighted that the prior sales of Bitcoin by the United States have already cost the U.S. taxpayers over $17 Billion! Did we ever think we would see the day when the White House took over Bitcoin education efforts globally?

With this shift in policy, it is worth exploring whether the data backs up the decision of the Administration to separate the asserts. To do this, let’s analyze two historical model portfolios, one that begins on January 1, 2018, and another that begins on January 1, 2022. These starting points represent the first full year after bull market peaks of Bitcoin’s historical four-year price cycles. Working from these starting points allows us to examine the performance of each asset over time. This overview provides a data-driven glimpse into how these digital assets have evolved over time, offering insights into asset composition, long-term value retention, and other considerations for large-scale sovereign investments.

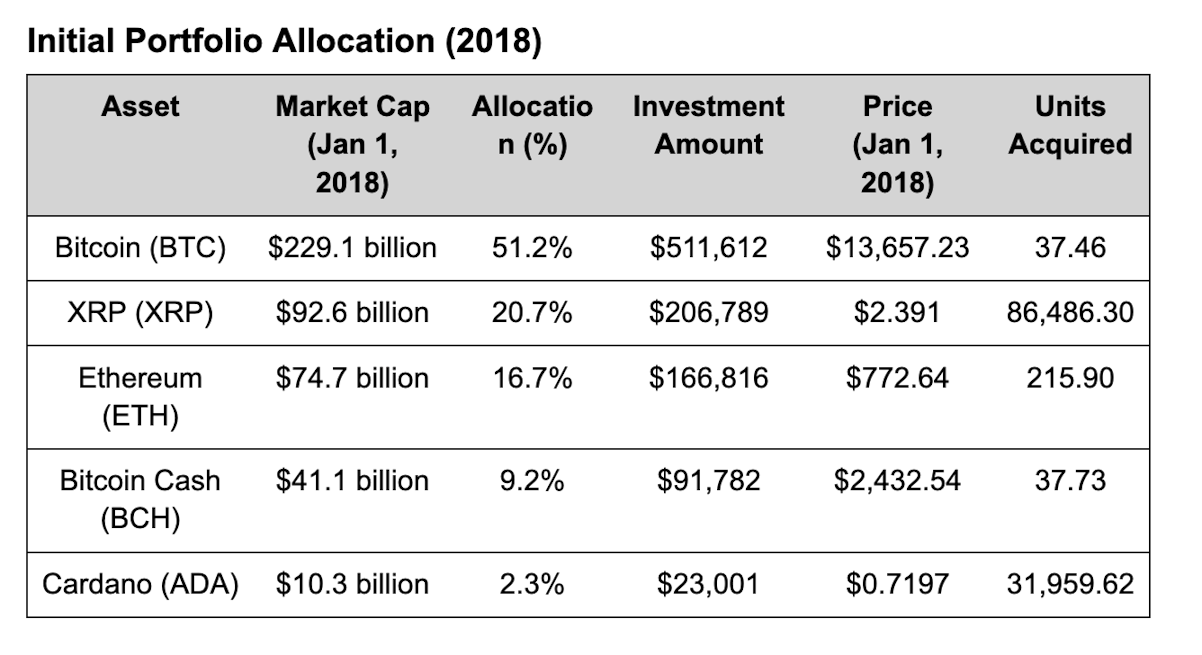

To build our portfolios, we will focus on the five dominant digital assets (excluding stablecoins and exchange tokens) by market cap to align with the initial indication of the first announcement made by President Trump about the “Crypto Strategic Reserve”. Once the assets are selected, they will be market cap weighted at initial inclusion. In taking this approach, we ensure we highlight the digital assets that have captured market share and excitement amongst investors, allowing us to follow their journey from each portfolio’s initial allocation to see how each asset performed up to the current day.

(Data Source: CoinMarketCap)

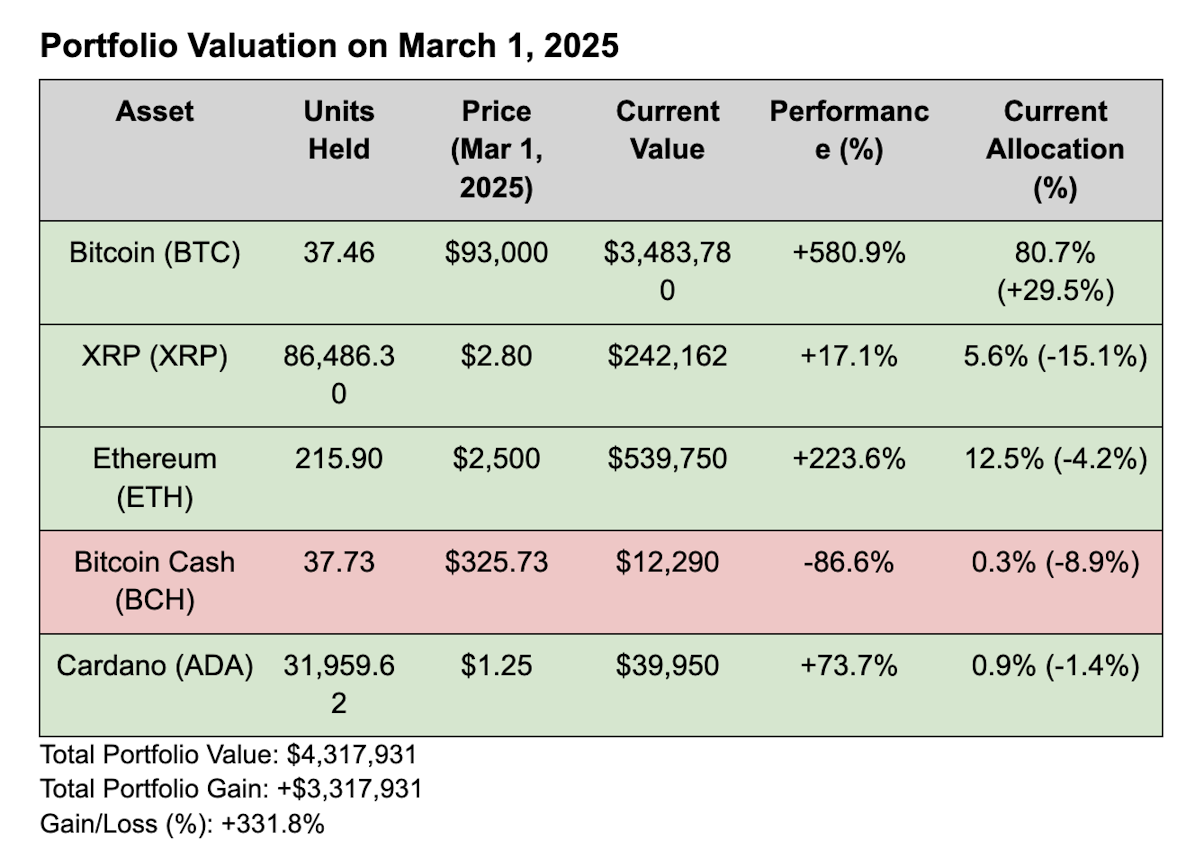

Total Portfolio Value: $4,317,931

Total Portfolio Gain: +$3,317,931

Gain/Loss (%): +331.8%

The first portfolio reflects allocations across Bitcoin, XRP, Ethereum, Bitcoin Cash, and Cardano, as these were the top five assets by market cap as of January 1, 2018. Over the past 86 months, a performance analysis reveals several key insights:

Four of the five assets gained at least some value since 2017, while the remaining asset, Bitcoin Cash, suffered catastrophic losses of 86.6%.

Among the appreciating assets, Bitcoin was the only one to increase its overall share of the portfolio, rising from 51.2% to 80.7% (+29.5%).

In contrast, despite positive returns, XRP and Ethereum saw their allocations decline (-15.1% and -4.2%, respectively) as Bitcoin absorbed capital, increasing its dominance.

This underscores a fundamental principle when evaluating a strategic reserve:

If the primary asset is also the best-performing asset, the reserve will naturally concentrate around it over time.

It also raises an important policy question for the U.S.:

If Bitcoin continues to dominate performance over the long term, would the U.S. resist the temptation to rebalance into underperforming assets by selling its best-performing store of value to diversify back into weaker alternatives?

Bitcoin (BTC): The clear leader in long-term value retention, appreciating 580.9% over this period. Bitcoin not only outperformed all other assets but also absorbed value from the declining altcoins, reinforcing its status as the premier choice as a digital reserve asset.

XRP: Over 86 months, XRP only managed to increase in value by 17.1%, ultimately resulting in XRP’s weighting in the portfolio being massively eroded over time as Bitcoin emerged dominant. XRP remains heavily reliant on regulatory outcomes and the influence of Ripple Labs, introducing centralization risks for any national reserve strategy.

Ethereum (ETH): A strong performer, delivering 223.6% returns, but still a distant second to Bitcoin. Its monetary policy shifts, centralized development leadership, and smart contract risks raise concerns about its suitability and dependability as a sovereign reserve asset. Despite Bitcoin’s outperformance, ETH did ultimately claim the #2 spot in the portfolio from XRP in the end.

Bitcoin Cash: Bitcoin Cash failed as a long-term store of value. Initially promoted as a “better alternative” to Bitcoin, it collapsed in value by -86.6%, proving irrelevant in the store-of-value conversation.

Cardano: Despite a modest 73.7% gain over the period, Cardano saw its weighting in the portfolio dwindle to below 1% of the total.

The takeaway here is clear: Bitcoin’s increasing dominance in the portfolio was not an arbitrary outcome but a reflection of its superior monetary properties and consistent long-term adoption trend as a store of value asset. Based on this portfolio, the administration got it right with the executive order.

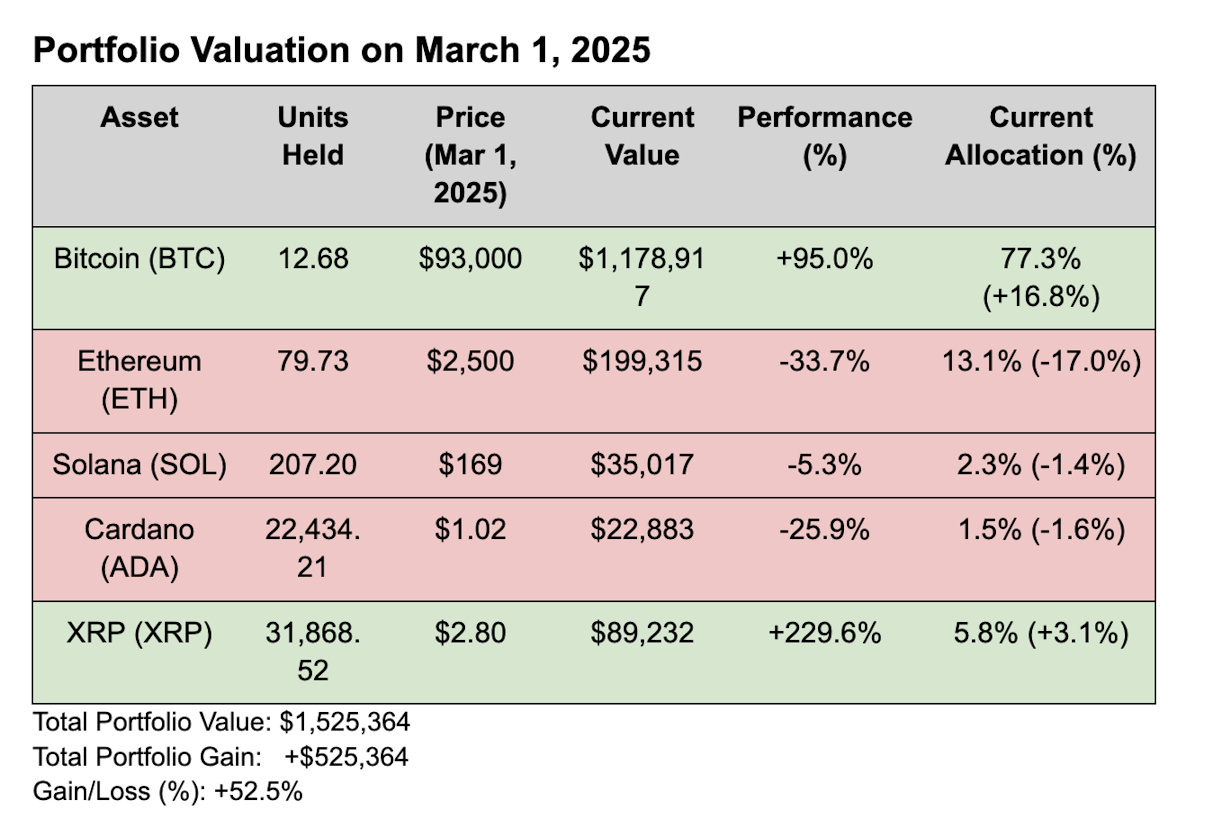

(Data Source: CoinMarketCap)

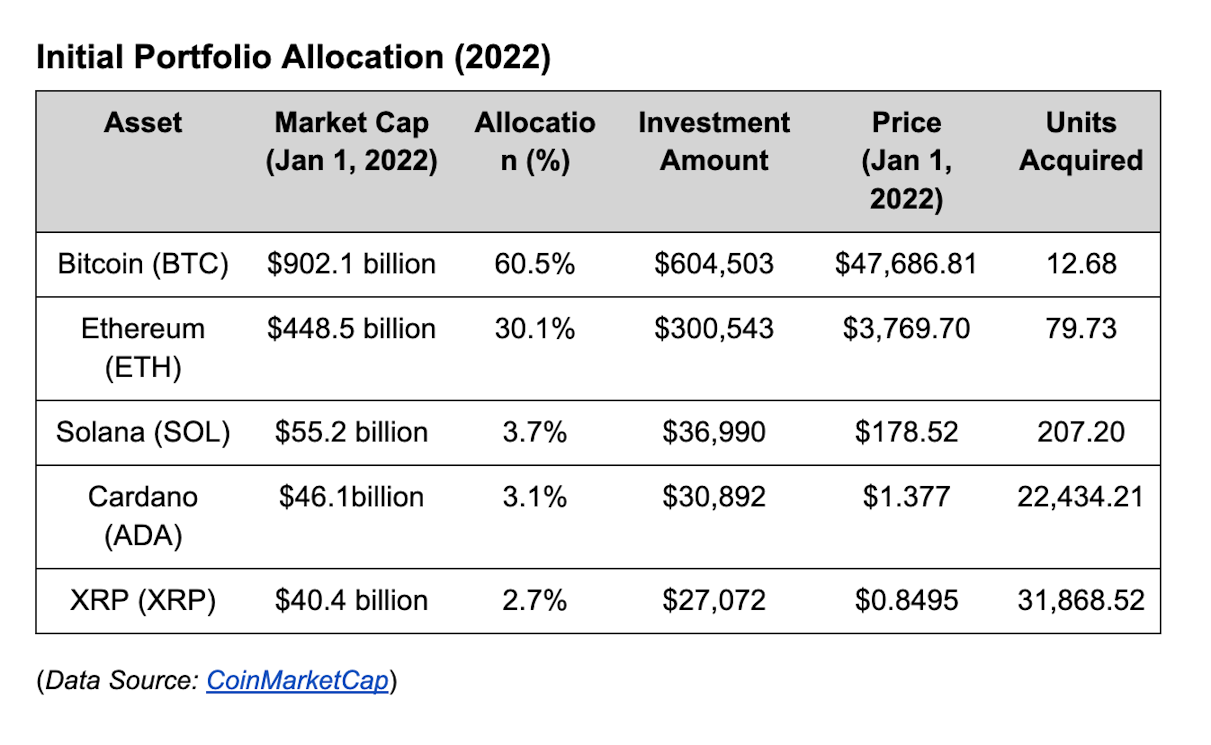

The 2022 portfolio is shorter at ~40 months and also represents a market cap-weighted initial allocation of the top five non-stablecoin, non-exchange-created digital assets as of January 1, 2022. By this point, the crypto market had already experienced multiple boom-and-bust cycles, allowing both projects and narratives to mature or fade based on their perceived long-term viability.

Notably, this portfolio mirrors the same assets initially identified by President Trump for the proposed Crypto Strategic Reserve, demonstrating that each asset included has at least remained relevant over this past market cycle.

When we look at the performance of this portfolio, we can make a few observations:

Only two assets, Bitcoin and XRP, achieved positive returns during this period, while Ethereum, Solana, and Cardano all suffered declines.

Bitcoin significantly increased its share of the portfolio, rising from 60.5% to 77.3% (+16.8%), while Ethereum’s share dropped from 30.1% to 13.1% (-17.0%), despite remaining the second-largest asset.

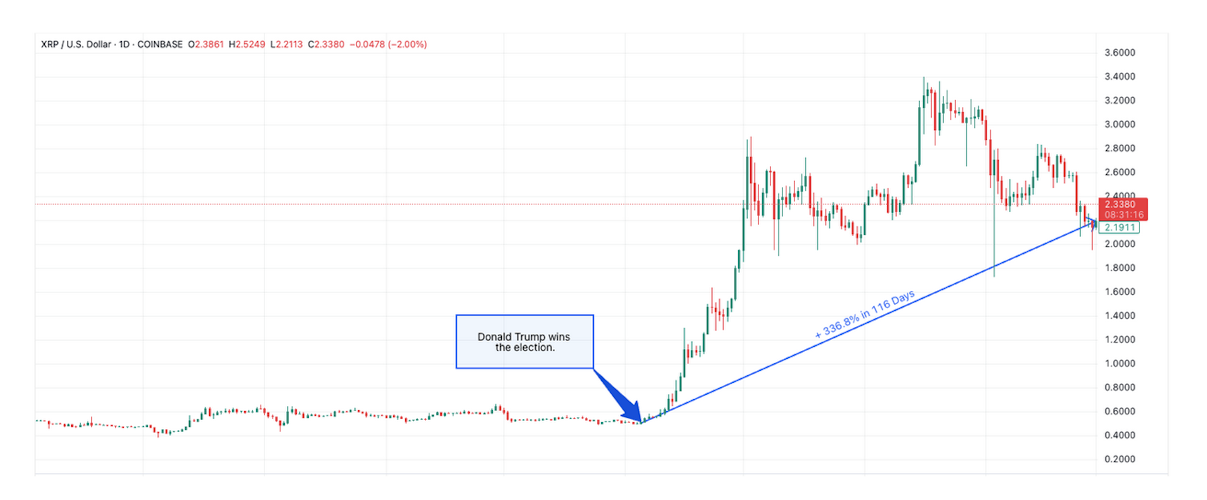

XRP delivered the highest individual return (+229.6%), but its gains were concentrated in the final 3.5 months of the period, as seen below.

Bitcoin (BTC): The strongest performer, appreciating 95% over the period. Bitcoin not only outpaced all but one other asset but also absorbed capital dominance, reinforcing its role as the anchor of any digital asset reserve strategy.

Ethereum (ETH): A disappointing underperformer, losing -33.6% of its value despite the reignited interest in cryptocurrencies and tokenization.

Solana (SOL) & Cardano (ADA): Massive underperformance, dropping -5.3% and -25.9%, respectively. While both networks were once heralded as Ethereum challengers, they have struggled to maintain adoption and suffered from network instability, governance risks, and ecosystem slowdowns.

XRP: The best-performing asset in the portfolio (+229.6%), though heavily skewed by late-cycle regulatory optimism following the Trump administration’s stance on crypto policy, which brought renewed regulatory optimism to the asset. Prior to the election results, XRP had suffered setbacks resulting in previously being delisted from trading on Coinbase and other exchanges as of January 2023 due to an SEC investigation, only to be reinstated in July 2023. Since relisting, the price had been a slow grind down until the election reignited hopes for a more favorable environment for the asset. However, despite the asset’s recent performance, one important question arises: Should the US really be bolstering the capital position of a single private entity?

This performance dynamic further reinforces the core principle of reserve asset management:

A well-structured strategic reserve must consider not just short-term performance but also long-term durability. What is the appropriate track record an asset should show in order to garner consideration for something as important as a strategic reserve?

When we take this principle into account, Bitcoin stands alone as the most appropriate Strategic Reserve Asset.

The 2021 portfolio underscores a repeating pattern seen now across multiple Bitcoin cycles:

Bitcoin continues to absorb dominance as weaker assets struggle for sustained relevance and investor capital.

The idea of diversifying reserves across multiple digital assets may introduce more risk than stability, as most altcoins fail to match Bitcoin’s long-term resilience as a store of value and seem entirely dependent on the hope of favorable treatment by governments instead of building a long-term track record of independent success and adoption.

If Bitcoin remains the best-performing asset, does a reserve strategy truly benefit from any of the others?

When we think of strategic reserve assets, the first that comes to mind is gold. For centuries, nations have maintained gold reserves as a pillar of economic stability and financial sovereignty. Gold’s scarcity, durability, and universal acceptance have made it the most trusted store of value across civilizations, allowing governments to hedge against currency devaluation, inflation, and economic crises. Unlike fiat currencies, which are subject to monetary manipulation and geopolitical risks, gold remains an apolitical asset that holds its value across generations. Its liquidity and deep global market allow nations to use it as a strategic reserve, reinforcing confidence in their financial systems and providing a safeguard against economic uncertainty. Additionally, gold’s lack of counterparty risk makes it unique as its value does not rely on any institution or government, reinforcing its role as a long-term financial anchor. This enduring reliability is why gold remains a cornerstone of central bank reserves worldwide, even as the global monetary system evolves.

Using this framework for reserve assets, the question naturally follows: which digital asset is best suited to be included in a national reserve? The logical answer is Bitcoin, and the administration got this right in the Executive Order by highlighting Bitcoin as “Digital Gold.”

Since its inception, the branding of Bitcoin as “digital gold” has established an undeniable link between the two assets. After all, Bitcoin was carefully engineered to perfectly embody the traits of a store of value, mirroring many of the qualities that have made gold indispensable: scarcity, durability, divisibility, fungibility, and non-sovereignty. Unlike gold, however, Bitcoin adds portability, verifiability, and an unforgeable monetary policy, making it arguably the first engineered perfect reserve asset. There is no credible argument against Bitcoin’s inclusion in a strategic reserve of digital assets. The debate was rather about which other assets, if any, deserve a place alongside it.

Bitcoin’s strategic importance is becoming undeniable. When Russia was cut off from the SWIFT network, nations worldwide witnessed firsthand the vulnerabilities of a financial system reliant on the U.S. dollar. This was an alarm bell signaling that nations must reevaluate their reserves to ensure they are not at risk of financial weaponization. As a result, countries are increasingly seeking alternative ways to transact outside of traditional monetary rails.

It should be no surprise that Bitcoin has emerged as a topic of serious discussion amongst BRICS nations, El Salvador, Bhutan, and others. Many of these nations have already established Bitcoin mining operations, recognizing the need to participate in the world’s largest decentralized monetary network and ensure they have hashrate within their borders. Unlike fiat reserves held in Western banks, Bitcoin cannot be seized, censored, or frozen by foreign powers. As a result, nations are securing optionality and quietly integrating Bitcoin into their financial strategies to protect themselves from geopolitical risks. Bitcoin is already an asset of strategic importance; it has not yet been formally broadly declared as part of national reserves. That shift is only a matter of time.

When one realizes that this shift is taking place, it is easy to understand the strategic importance of the United States’s participation in the Bitcoin network. This maneuver allows the United States to head off the activities of other nations that seek to lower the importance of the US Dollar globally by ensuring that they have a major stake in the only truly decentralized monetary system of scale.

Can the same be said for the other assets which were under consideration? The general answer is no.

Bitcoin stands out among digital assets in many ways:

Decentralization and Legal Status: Bitcoin is the most decentralized digital asset and in no way passes the Howey Test or otherwise meets the definition of a financial security. All coins were mined after the protocol was released to the public rather than pre-mined, with no special advantage given to the protocol’s creator (s). It uses proof of work, which allows anyone with hash power to contribute to new block generation and, thus, new coin creation.

Scale and Liquidity: Bitcoin has been the largest and most liquid digital asset for 16 consecutive years since its inception. It benefits from massive scale and network effects, which are tremendously important when it comes to competition between monies or communication protocols. Size and liquidity matter, especially at the scale of nation-state purchases and sales.

Immutability: Bitcoin is the most immutable digital asset network. It has by far the most nodes of any network, and updates cannot be pushed to them. Many other cryptocurrencies have changed fundamental variables, such as monetary policy, whereas the Bitcoin network has maintained a rather consistent ruleset. Soft forks require a broad amount of consensus, and hard forks are nearly impossible to perform.

Censorship Resistance: It’s the most difficult digital asset network to censor, which is relevant for nation-states to be able to move their coins and use the network as an open transaction method. Beyond that, even if it were to be censored, such as with a 51% mining attack, it’s possible to uncensor the network by bringing on new hashrate. Existing miners cannot forbid new miners from entering the competition, and so a large country or group of smaller countries that find themselves censored have options to uncensor their coins and re-enable their participation in the network. This is in contrast to proof-of-stake systems, where existing stakeholders can potentially censor a network and prevent new entities from becoming stakeholders, thus creating a permanent lock that requires a successful fork to escape from.

Resilience: Proof of work is the most resilient against significant network problems. Proof-of-stake systems rely on circular logic, where stakeholders are defined by the current state of the ledger and the current state of the ledger is defined by stakeholders. As a result, if the network encounters a bug or otherwise goes offline, the primary way to restart the network is for major stakeholders to meet and coordinate a restart. By using energy as an external input for proof of work, Bitcoin avoids relying on circular logic, which allows it to recover from many critical errors via a bottom-up method of nodes and miners seeking out and building upon the chain that proveably has the most work put into it.

Overall, both as a 1) large, liquid, and reliable store of value and 2) as a censorship-resistant transaction method, Bitcoin is uniquely capable among digital assets of serving a strategic purpose to nation-states.

The majority of digital assets, outside of Bitcoin and a handful of others based on their creation method, are effectively digital securities. They often issue coins to founders and early investors, have an organization chiefly responsible for their ongoing maintenance, development, and advocacy, and use governance models such as proof-of-stake that operate similarly to shareholders.

In that sense, a government choosing to buy one digital asset and not another is similar to its own sovereign wealth fund buying shares in some domestic companies and not others. What criteria should be used when effectively “playing favorites” in this sense? Especially when there are indeed pre-mined coins associated with founders and early investors. There are considerable conflicts of interest to consider as well, especially if leaders within the government that have input into the purchasing decisions were involved in those early activities and premines and thus are in a position to benefit themselves.

One may argue that there is a similar conflict of interest with Bitcoin. In other words, a large holder of Bitcoin may advocate for a government to acquire Bitcoin as a strategic asset and thus benefit from the positive price action that may ensue. However, that’s no different than a gold holder advocating for a government to add more gold to its stockpile or to fill up its strategic petroleum reserve.

Ethically speaking, there are many landmines when purchasing digital assets with any sort of issuer or premine. Care should be taken to look for conflicts of interest among government leaders. Taxpayers can wind up serving as exit liquidity for digital asset insiders, with no strategic advantage provided to the nation-state or its citizens in the process.

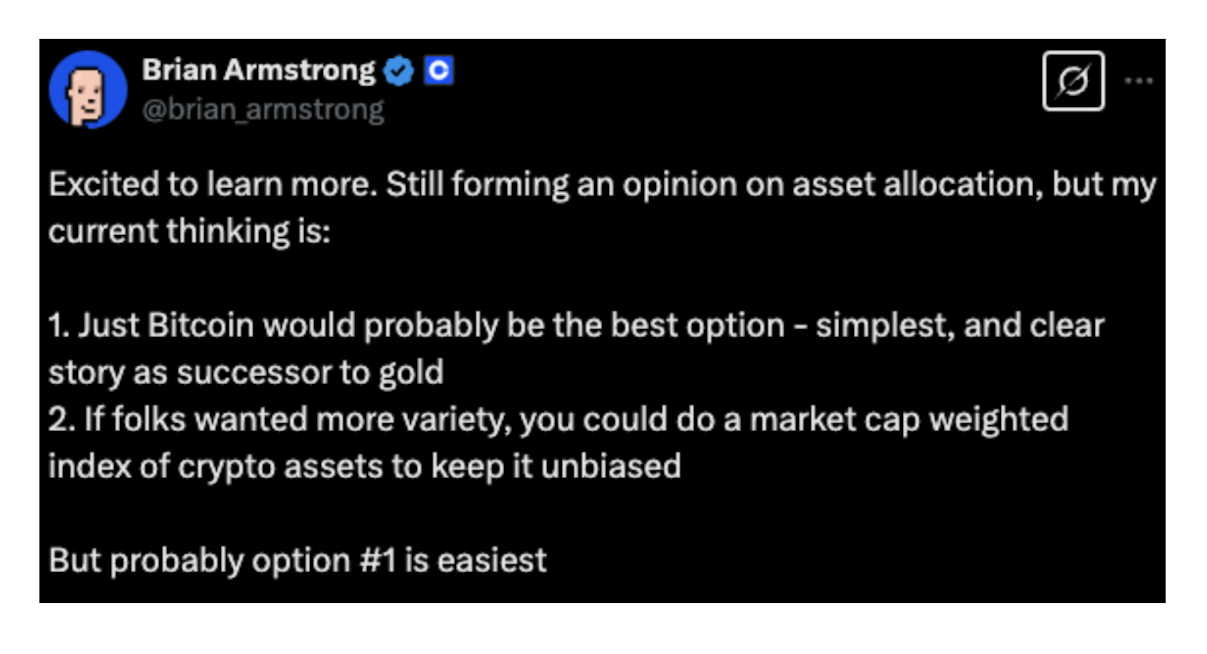

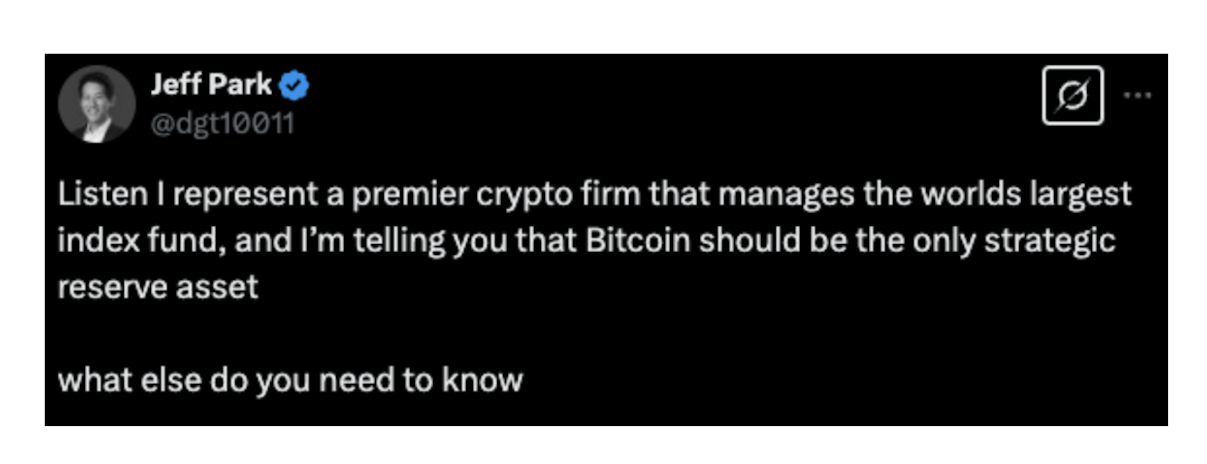

The initial announcement of the coming Crypto Strategic Reserve stood out for an interesting reason: industry leaders, who typically have financial stakes in various digital assets, are surprisingly unified in their stance. Despite their diverse interests, they advocated that the reserve should focus exclusively on Bitcoin.

Brian Armstrong, the CEO and Chairman of cryptocurrency exchange giant Coinbase, shared his thoughts on the announcement and threw his support behind Bitcoin.

Tyler Winklevoss, the co-founder and CEO of cryptocurrency exchange Gemini, shared that only one asset meets the bar for a strategic reserve.

Jeff Park, Head of Alpha Strategies and PM at Bitwise Asset Management, shared his thoughts from his position representing the world’s largest crypto index fund.

Renowned entrepreneur, investor, and thought leader Raval Navikant also commented on the appropriateness of using American taxpayer money to provide exit liquidity for assets that are not truly decentralized.

By now, I’m certain you can see the trend. There was general agreement that Bitcoin was the only digital asset that genuinely passes the test as a digital asset of true strategic importance to a nation warranting inclusion in a strategic reserve.

Yet lobbying is an effective and pervasive approach in the USA, resulting in many unanticipated outcomes. However, with the Executive Order, we now see that the Administration also understood the difference between the different assets and arrived at Bitcoin as strategic to the nation’s long-term interests.

The United States has taken a decisive step with the announcement of a Strategic Bitcoin Reserve, a move solidified by an Executive Order that correctly distinguishes Bitcoin from other asset classes while granting the necessary authorizations to build this reserve.

History has shown that monetary dominance belongs to the strongest, most resilient, and scarcest asset available. As the world transitions into a digital financial era, the U.S. faces a pivotal moment: embrace Bitcoin as a strategic reserve asset or risk falling behind as other nations recognize its unparalleled advantages.

Bitcoin is the only digital asset that meets every essential criterion for a sovereign reserve: decentralized, highly liquid, the most secure network in existence, a proven store of value, and a powerful geopolitical tool. Just as gold once anchored national treasuries, Bitcoin now offers the U.S. a chance to reinforce economic sovereignty, hedge against monetary debasement (yes, even its own!), and establish dominance in the emerging digital financial system.

The move is bold, and it shows the world the United States is looking forward and not relying on the present day or the past. They recognized the value of Bitcoin publicly on the global stage and signaled to the world the undeniable message that Bitcoin is here to stay.

Ben Werkman is a long-time Bitcoin advocate and entrepreneur, with a background in commercial distressed credit, technology consulting and strategic finance. He currently specializes in advising corporations on Bitcoin Treasury solutions, helping companies navigate the intersection of Bitcoin and corporate finance. Recognized as a leading analyst in Leveraged Bitcoin Equity (LBE) strategies, Ben has extensively covered the rise of Bitcoin-focused public companies, including MicroStrategy (MSTR), Semler Scientific (SMLR), and Metaplanet (3350.T). His expertise places him at the forefront of the discussion on Bitcoin-enabled treasury management and corporate strategy.

Lyn is an investment strategist at Lyn Alden Investment Strategy. She holds bachelor’s degree in electrical engineering and a master’s degree in engineering management, with a focus on engineering economics and financial modeling. Lyn has been performing investment research for over fifteen years in various public and private capacities.

Thoughts on Bitcoin from the Swan team and friends.

Bitcoin offers a strategic approach to investing. Here are the top 5 benefits: it reduces volatility risk, simplifies investing, lowers emotional stress, fosters discipline, and enables long-term growth.

Swan Vault is advanced Bitcoin security made simple. You don’t need a bank, but you don’t have to go it alone.