July 18, 2024

Dear colleagues,

Clients first started asking me about Bitcoin in 2017, and I told them it was digital Beanie Babies.

I explained that although Bitcoin’s supply may be capped at 21 million, that doesn’t make it scarce because anyone can create an unlimited amount of new “crypto” tokens. I told them that Bitcoin was a hype-fueled bubble, a purely speculative asset, and a foolish long-term investment.

I was wrong.

After ignoring Bitcoin for the next three years, I noticed in 2020 that it wasn’t dead yet. I decided that if I was going to continue dismissing it, I needed to at least read a book about it. So I read The Bitcoin Standard by Saifedean Ammous and Inventing Bitcoin by Yan Pritzker.

I quickly learned that brilliant people from multiple industries and disciplines had answered all my initial objections to Bitcoin dozens of times. In two years, I read more than 40 books about Bitcoin, monetary history, computer science, Austrian economics, and central banking. I listened to podcast interviews like The Saylor Series and read blogs like Nick Szabo’s Unenumerated.

Today, I believe Bitcoin is the most important financial innovation that will happen in my lifetime. It took me hundreds of hours of research to conclude, so I do not expect to convince you of it with this letter. My goal is to convey a simple message to the wealth management industry: You need to study Bitcoin.

Bitcoin will impact every area of financial services. If you’re a financial advisor, it will disrupt your business and your career.

That may sound like a bold claim. If you’re skeptical, I invite you to accept this letter as a challenge. Do what I did: I thought Bitcoin was stupid, but I wanted to know it was stupid, so I started researching it. And I discovered something far more interesting.

I think you’ll discover that too.

In 1911, Marshal Ferdinand Foch declared that airplanes were “Interesting toys, but of no military value.”

A few years after that, Foch served as the supreme allied commander during the First World War (1914-1918).

The Imperial War Museum webpage for “The Underworld” notes that: “Between May 1917 and May 1918, more than 300,000 people used the tube to shelter from German aeroplane attacks.”

In hindsight, it’s easy to mock Marshal Ferdinand Foch, but it’s worth noting that airplanes had only existed for eight years when he said that. Bitcoin had only existed for eight years when clients started asking me about it in 2017, and back then, the most common opinion I heard about it from financial professionals was eerily similar: “Bitcoin is interesting technology, but it has no real value as an asset.”

I still hear financial professionals saying this. Like Foch did with airplanes, they judge Bitcoin based on how it fits within the existing paradigm. Because of that, they fail to understand Bitcoin fundamentally and do not see what it is becoming: a new paradigm altogether.

Bitcoin is digital money. It’s easy to overlook how profound that is. After all, most U.S. dollars don’t exist in physical form. They exist only as digital entries in a bank’s ledger. So don’t we already have digital money? We already make digital payments without Bitcoin, so what problem is it solving?

We, in fact, did not have digital money before Bitcoin. We had digital credit. In her book Broken Money, Lyn Alden describes how new telecommunication technologies like the telegraph and the telephone created a massive divergence between the speed of payments and the speed of settlement. In the late 19th century, it became possible to transmit payment information worldwide at the speed of light. Gold, however, can’t move that fast.

As a result, the global monetary system evolved as an interbank credit network with gold at the base layer. This enabled the high-volume, high-frequency exchange of bank-issued credit claims on gold, while the burdensome final settlement of physical gold only needed to occur periodically between banks. However, this system had a major flaw: Expanding the gold supply requires significant time, energy, and resources. Issuing additional credit claims does not.

This led to a fractional reserve banking system that granted a small number of institutions the enormous privilege of expanding the credit-money supply at virtually no cost. The result was that credit claims on gold in circulation vastly exceeded the amount of physical gold backing those claims. Every central bank in the world eventually defaulted on its obligation to redeem credit claims on gold, culminating in Richard Nixon closing the gold window permanently in 1971. This ushered in the modern age of fiat money — currency backed by nothing, with no connection to the real world to limit its supply.

This is the fundamental problem Bitcoin solves. In the words of Bitcoin’s pseudonymous creator:

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.”

– Satoshi Nakamoto

Bitcoin is a bearer asset. It is no one’s liability. Delivery of Bitcoin constitutes the final settlement of a payment. Unlike gold, Bitcoin can be sent across telecommunication channels because the payment information is the money.

Bitcoin is often described as “digital gold.” That’s a helpful analogy for someone trying to wrap their head around what it is, but it’s insufficient. It would be like describing the internet as a digital newspaper in 1990. It isn’t wrong, but it fails to capture the significance of the new technology and what the existence of that technology implies for the future.

Like gold, Bitcoin’s scarcity is enforced by the unforgeable costliness of energy. Anyone can expand the gold supply, but it costs energy to do so, and there is no way around that cost. The same is true for Bitcoin, except Bitcoin has a supply cap of 21 million. At the time of this writing, about 19.7 million Bitcoin have been mined so far, and it will take over a century to mine the rest.

This makes Bitcoin the scarcest monetary good in human history. Because it’s digital, it can be divided, stored, verified, and moved at a marginal cost that approaches zero—all without the use of a trusted intermediary.

We have never seen anything like that before!

The debate over the military usefulness of airplanes got settled pretty quickly when bombs started falling from the sky. Adopting superior military technologies, such as gunpowder and the airplane, is not optional. Nations either adopt them or they get outcompeted by those that do. The same is true for superior monetary technology.

As Saifedean Ammous has said, “History shows it is not possible to insulate yourself from the consequences of others holding money that is harder than yours.”

Rather than trying to convince you of Bitcoin’s theoretical merits or of its future prospects, I invite you to simply look up. The “bombs” are starting to fall.

In 2020, MicroStrategy became the first public corporation to adopt Bitcoin as its primary treasury reserve asset. Michael Saylor, the founder and Chairman of MicroStrategy, described his company’s dilemma in 2020 as “hundreds of people working as hard as they can and going backward.”

Saylor has noted that the U.S. dollar money supply expanded by a historical average of about 7% per year over the last century, and that expansion accelerated in 2020. Saylor recognized that the cash and credit instruments MicroStrategy held on its balance sheet could not generate a yield as high as the rate of monetary debasement. This meant that the corporate treasury was dilutive to shareholders. Saylor also recognized that, except for a few technology companies with large network effects, it is not reasonable to expect a mature business to continue growing its cash flows at the rate of monetary debasement every single year.

MicroStrategy made an initial investment of $250 million of its corporate treasury into Bitcoin. Today, MicroStrategy holds 214,400 Bitcoin worth about $15.2 billion, acquired at a total cost of $7.538 billion. It acquired most of that by issuing equity and convertible debt, yet the company’s Bitcoin per share continues to increase. While MicroStrategy’s treasury of cash and credit was dilutive to shareholders, Saylor makes the case that its Bitcoin treasury is accretive.

MicroStrategy published their Bitcoin Initiative Roadmap for any corporation to use. A recent change to the FASB accounting rules for Bitcoin also allows GAAP-compliant corporations to hold Bitcoin on their balance sheets without artificially impairing their financial statements through indefinite intangible accounting (which used to be the rule for Bitcoin). On May 28th of this year, Semler Scientific became the latest public company to adopt Bitcoin as its primary treasury asset.

Pension funds and endowments have the same long-term treasury problem as corporations and are also adopting Bitcoin. For example, in the first quarter of 2024, the State of Wisconsin Investment Board added $160 million of exposure to its state pension fund. And on June 3rd, the University of Austin (UATX) announced the creation of the first long-term Bitcoin endowment.

On January 10th, 2024, the SEC approved 11 spot Bitcoin ETFs. This made it possible for financial advisors in the US to offer clients exposure to Bitcoin through a traditional security. As of market close on June 6th, 2024, the combined AUM of these ETFs had grown to about $61.5 billion. I believe introducing these ETFs has reversed the burden of proof for financial advisors and Bitcoin. Instead of fighting to justify offering Bitcoin to clients, advisors and their firms now need a good reason not to offer it.

When the Bitcoin protocol began in 2009, the asset had no monetary value whatsoever. Bitcoin monetized organically on the global free market. Now, there’s over a decade of reliable price history.

Bitcoin’s price has increased by about 60% per year for the last 10 years, from around $600 in June 2014 to around $70,000 in June 2024 at the time of this writing.

Bitcoin’s market cap is now around $1.4 trillion. This sometimes causes people to believe they “missed out, ” but that is a mistake. While no one knows what returns will be in the future, I believe the majority of Bitcoin’s returns lie ahead. That’s because Bitcoin is not a tech stock. It’s an entirely new asset class. It competes as a store of value with gold, bonds, stocks, and real estate, but it is still tiny compared to those asset classes.

Bitcoin’s price behaves differently from those of other assets. Roughly every four years, the Bitcoin issuance rate gets cut in half. When the protocol began in 2009, Bitcoin miners generated 50 new Bitcoin every 10 minutes on average. In 2012, that got cut in half to 25. Most recently, in April 2024, it reduced from 6.25 to 3.125. So far, Bitcoin’s price has seemed to follow a 4-year cycle corresponding to the issuance halving.

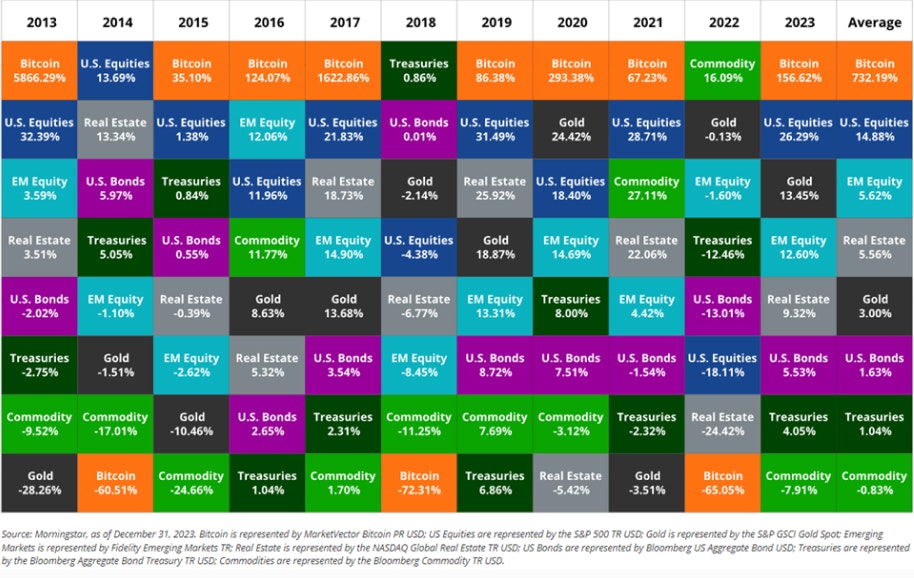

If you rank historical asset class returns from best to worst by calendar year, it’s clear that Bitcoin does not behave like any other asset. Based on this historical price behavior, its potential to enhance the diversification and risk-adjusted returns of a portfolio should be obvious.

You may not care about Bitcoin, but if you’re a financial advisor, you do not have the luxury of ignoring it.

The last five decades of fiat money have stimulated a massive artificial demand for wealth management services. A large portion of our industry only exists because the currency bleeds purchasing power every year. I won’t pretend to know precisely how large that portion is, but if you reflect on all the clients you’ve ever worked with, I suspect you’ll see that what I’m saying is true.

Many clients would avoid investments altogether if they could, but they know that if they want to become or remain wealthy, they can’t simply save in a savings account. Inflation forces would-be savers to take investment risks they otherwise wouldn’t, and many of them hire professionals (like us) to help them navigate the complexities of the investment world.

Bitcoin may be volatile, but it is not an investment. Bitcoin is money. For the first time in at least 50 years, saving money over the long term is a winning proposition again. Bitcoin provides an alternative to investing, and more and more people are embracing that alternative.

I talk to investors almost every week now that fit the following description:

Within 10 years of retirement

7-figure investable net worth

More than 50% allocated to Bitcoin

Some are 100% allocated to Bitcoin (besides short-term savings).

Of course, we discuss diversification. They’ve all thought about that. However, many of these investors held their net worth in Bitcoin from the 2021 peak of $69,000 to the 2022 low of $16,000, then back up to over $70,000, and they never panicked. They know what they own. They often ask me: “Why would I want to own anything else?”

Sometimes, there’s a very good reason why they should own non-Bitcoin assets. Sometimes there’s not. Either way, I enjoy having these discussions with investors, and the only reason I can have them is because of my knowledge of Bitcoin. That’s why these investors reached out to me in the first place.

To modify a quote I used earlier: “History will show it is not possible to insulate your advisory practice from investors choosing to hold an asset that is harder than anything you can offer them.”

It’s happening now.

If you are serious about understanding how you can embrace Bitcoin to best serve your clients and grow your business, please get in touch. I’d be happy to share what I’ve learned with you.

You can reach out to Matt at matt.golliher@vistainvestment.net

Vista Investment Partners (Vista), a federally registered investment adviser under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Vista, Form ADV Part 2A & 2B can be obtained by visiting: https://adviserinfo.sec.gov and search for our firm name. Neither the information nor any opinion expressed is to be construed as solicitation to buy or sell a security of personalized investment, tax, or legal advice.

The information herein was obtained from various sources. Vista does not guarantee the accuracy or completeness of information provided by third parties. The information in this report is given as of the date indicated and believed to be reliable. Vista assumes no obligation to update this information, or to advise on further developments relating to it.

Hold your IRA with the most trusted name in Bitcoin.

Matt Golliher is a Financial Advisor with Vista Investment Partners. He lives in Richmond, IN, with his wife, Devra. Matt became a Bitcoiner in 2020.

Along with educating his clients, colleagues, and community about Bitcoin, Matt focuses on helping Bitcoiners who need traditional wealth management and financial advisory services.

If you have any questions or would like to contact Matt, you can do so using the contact information below.

News

July 18, 2024

July 16, 2024

July 16, 2024

July 12, 2024

Thoughts on Bitcoin from the Swan team and friends.

With its launch in the center of global finance, Swan Bitcoin empowers New Yorkers to build lasting wealth with Bitcoin financial services and expert guidance.

We are excited to share the latest improvements to the Swan Bitcoin mobile app, streamlining your Bitcoin buying and storage experience.