Swan Private Market Update #30

This Market Update report was originally sent to Swan Private clients on April 7th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

Since the banking crisis began, many market participants feared that a global financial crisis was right around the corner. In fact, after remarks from Swiss National Bank Vice President Martin Schlegel, it appears that these investors were not wrong to think this way. In an interview on Monday, Schlegel said, “Without the government-brokered takeover (of Credit Suisse), it’s very, very likely a financial crisis in Switzerland and worldwide would have happened.” It appears that the late Sunday government-sponsored shotgun acquisition of Credit Suisse was just enough to avoid a global financial crisis.

This Market Update report was originally sent to Swan Private clients on April 7th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

Today, investor worries about the banking crisis appear to have subsided in part due to the actions from central banks and governments to backstop depositors and provide liquidity to the banking system in its time of need. After the Federal Reserve announced its new Bank Term Funding Program, eased access to its discount window, and ramped up its USD liquidity swap lines from weekly to daily, it seems as if their response has been enough to prevent the banking crisis from spiraling out of control.

Only time will tell if these actions will be enough to prevent further bank contagion from spreading, but for now, these liquidity measures seemed to have done have plugged any cracks forming in the financial system. The response from central banks and governments has bolstered liquidity in the banking system but has done nothing to fix the underlying problem that is pervasive throughout the economy today: a breakdown of trust.

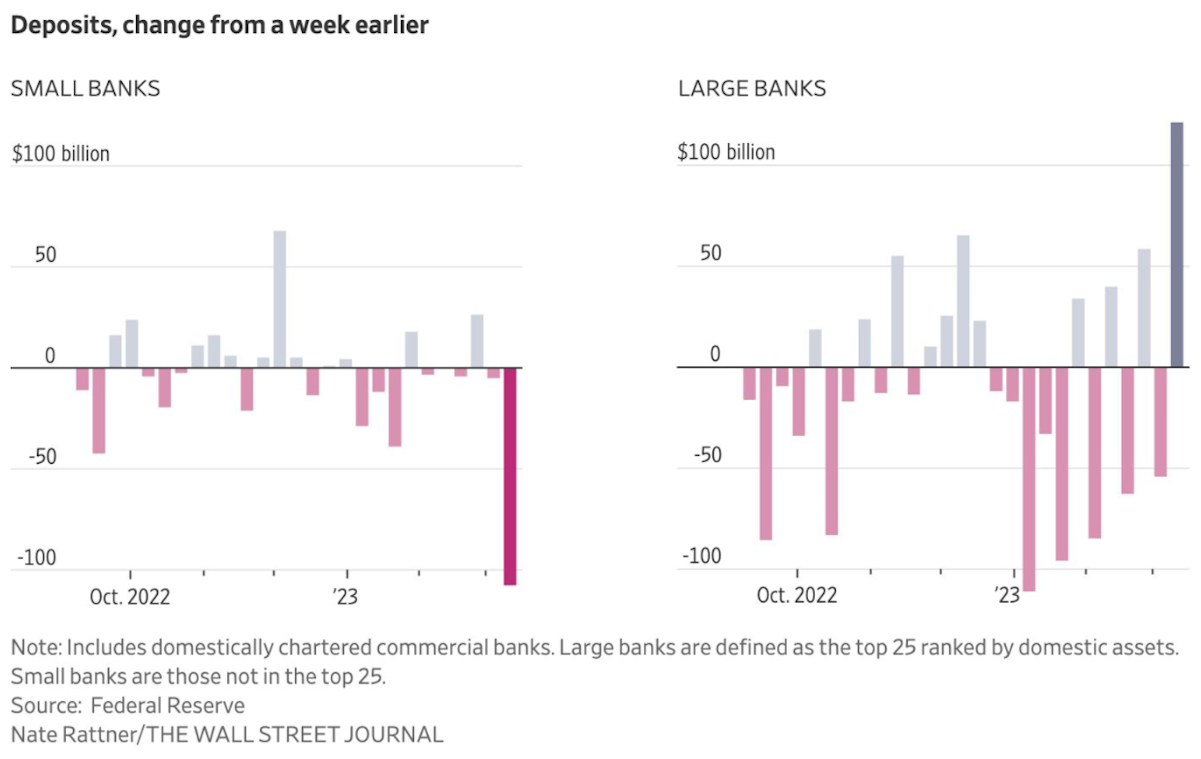

The first example of this breakdown can be observed in the continuous drain of deposits from smaller banks to larger banks. In the week following the collapse of Silicon Valley Bank, the top 25 US banks gained over $120 billion in deposits, while all the banks outside the top 25 lost $108 billion. This has been a record outflow for these small banks.

Depositors no longer trust that their money is safe in these smaller banks because they feel that smaller banks are less likely to receive a backstop from the Treasury and Federal Reserve in the event of a crisis compared to their too-big-to-fail counterparts.

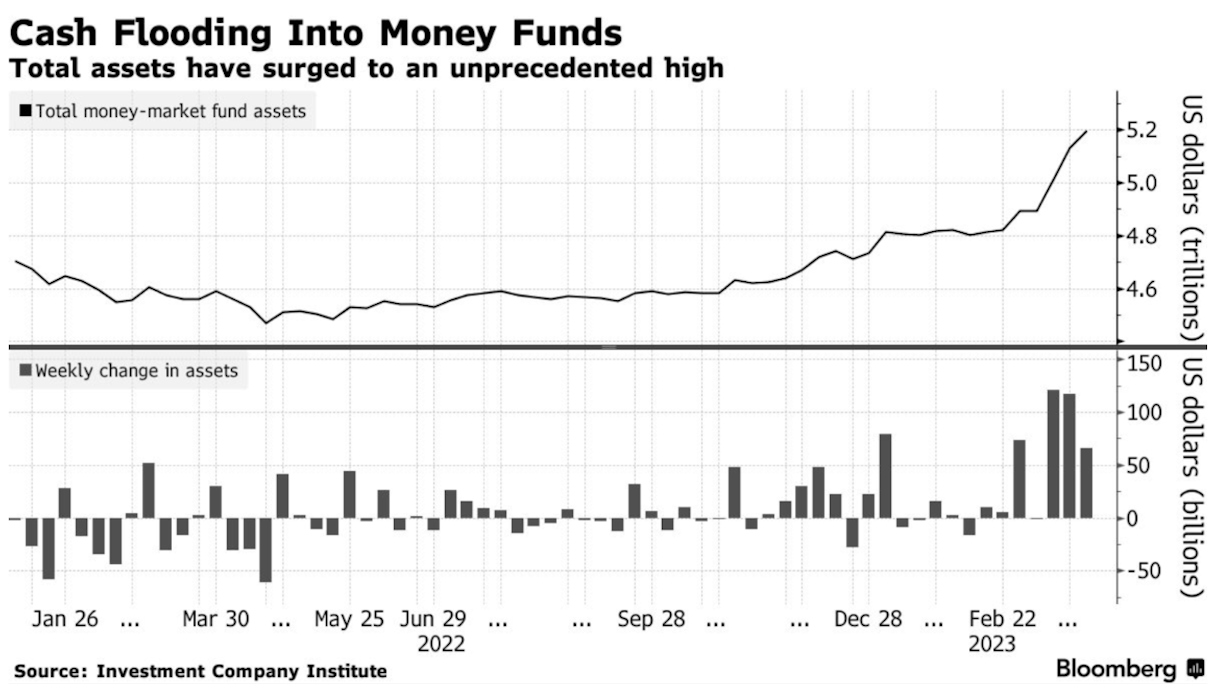

Not only are depositors leaving small banks for the safety of larger banks, but they are also fleeing to money market funds where they can earn a greater yield. Money-market funds saw inflows of $304 billion in the three weeks leading up to March 29th. This was a record, topping the $286 billion of inflows observed in three weeks in March 2020.

These record inflows into money market funds were partly driven by concerns over the health of these smaller lenders. Why trust a small bank when you can just park your funds in a money market fund and earn four times the yield?

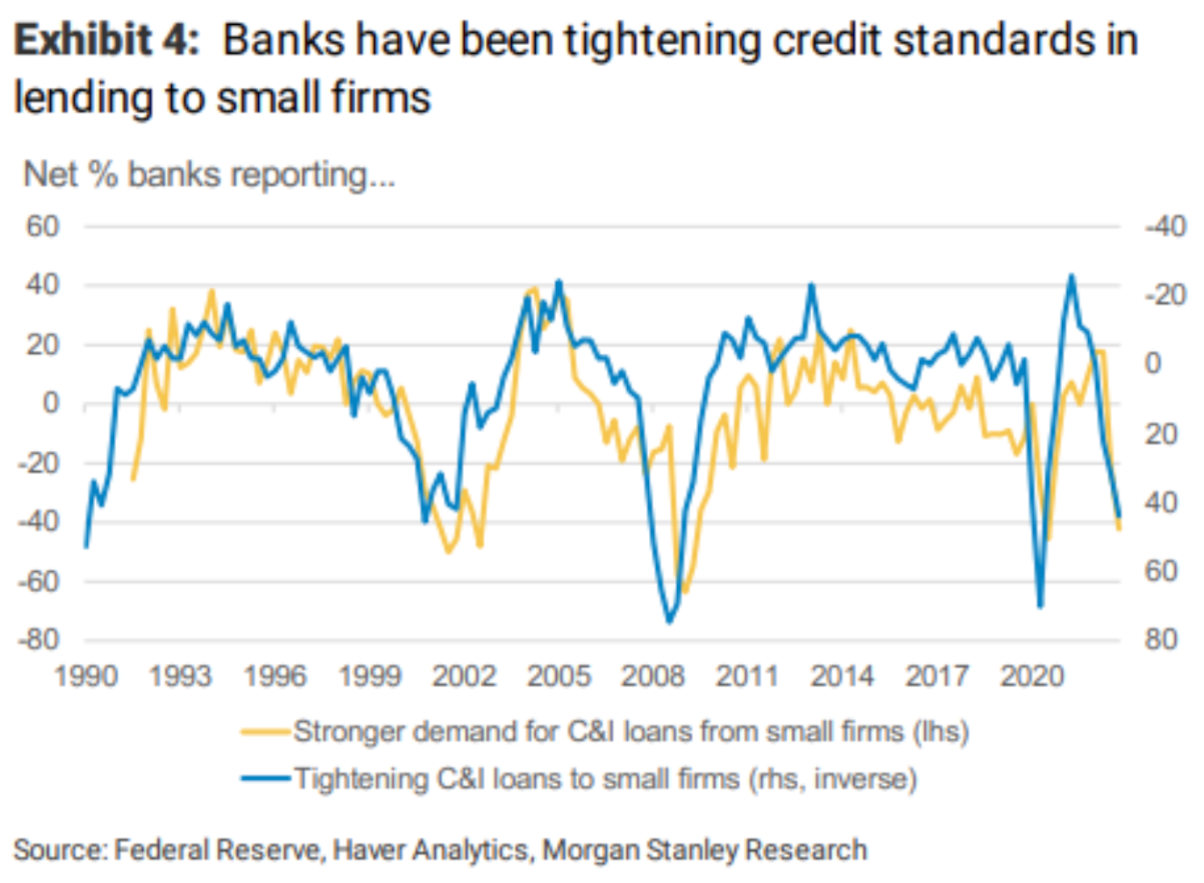

But the breakdown in trust is going both ways. As deposits flow out of these small banks, there is ample evidence that these banks have begun to tighten lending standards in the economy.

According to the American Bankers Association, deposit accounts represent 71% of bank funding today. Losing this source of funding undermines the business models of these small banks. They are left with two choices, they can raise rates on deposits, eating into their profit margins, or they can reduce the availability of credit in the economy.

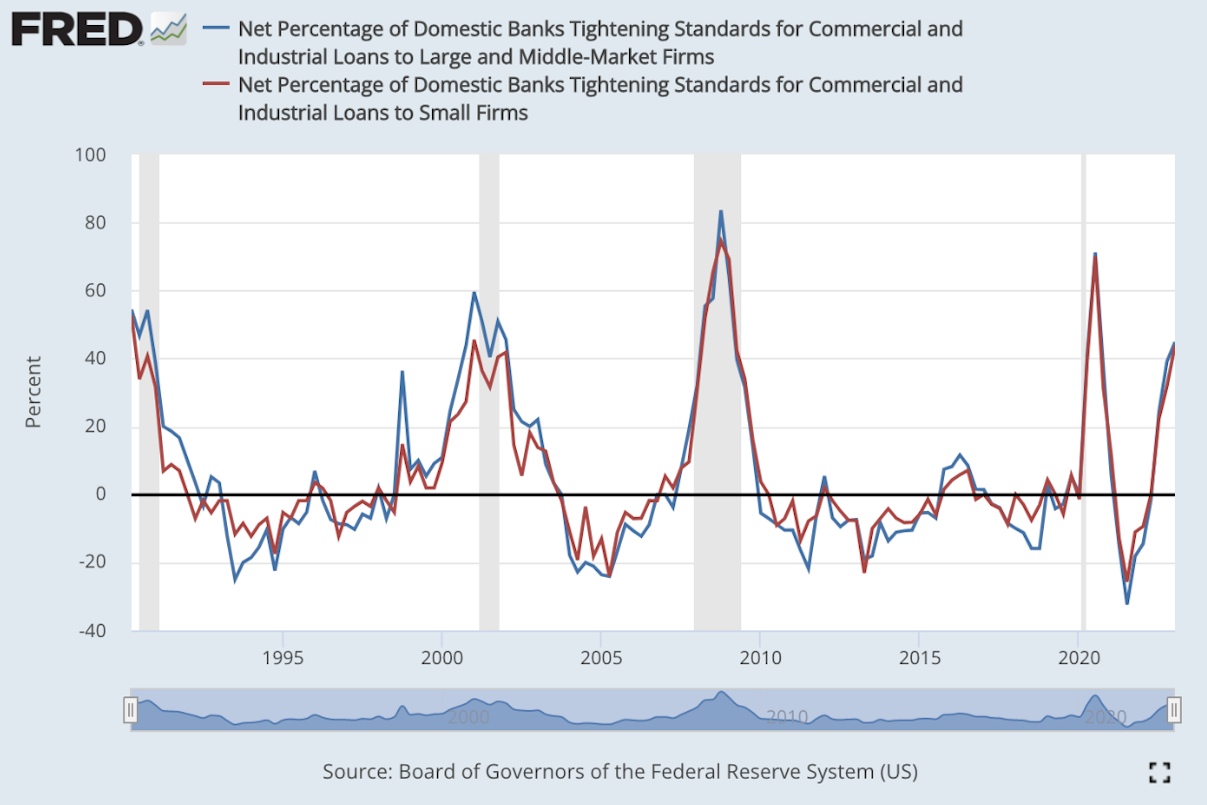

This trend can be seen in the percentage of banks reporting a tightening in their lending standards to small firms in the Senior Loan Officer Opinion Survey conducted quarterly by the Federal Reserve. Out of the 80 domestic banks and 24 branches of international banks surveyed, 43.8% said they have been tightening lending standards to small firms.

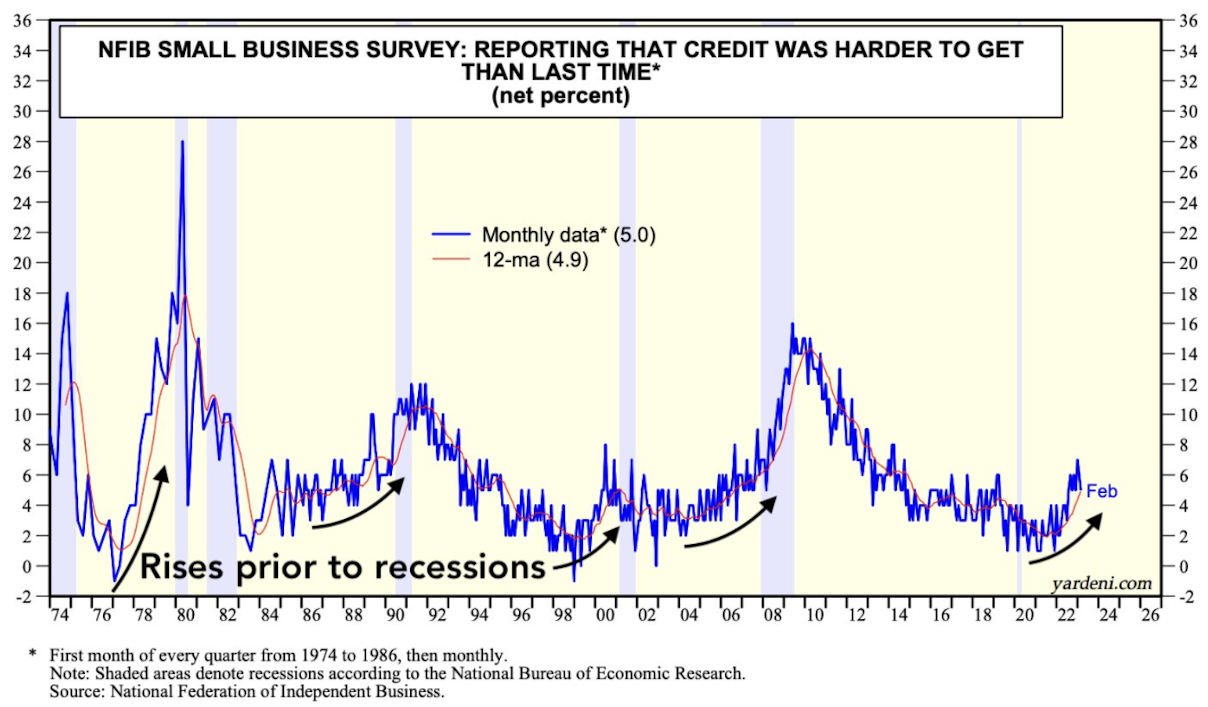

Small businesses have also confirmed this to be true in the latest NFIB Small Business Survey where an increased percentage of survey participants agreed that “credit was harder to get than last time.” Yardeni Research shows below how a rise in this reporting typically occurs before a recession begins.

This development has not just been observed with smaller firms. From the same survey, the net percentage of domestic banks tightening lending standards to large and middle-market firms has also contracted with 44.8% reporting that they have tightened standards.

And the trust is not only breaking down between consumers and banks, it’s also deteriorating between institutions. Companies that need to raise are finding it more difficult to do so in this environment of economic uncertainty. The conditions around the banking crisis are freezing up credit markets between entities.

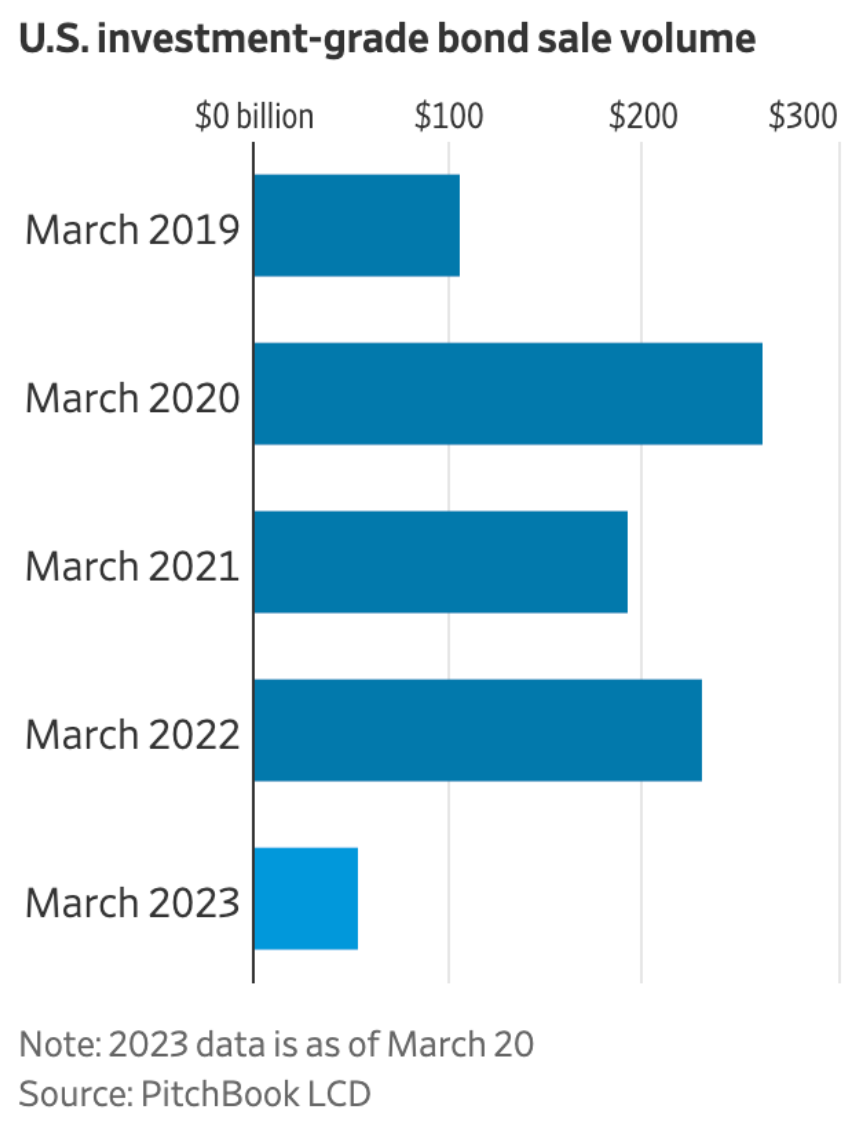

In the month of March, there was nearly $60 billion in new investment-grade bonds issued. This is heavily below the five-year average of $179 billion for this time of the year.

The past three years of corporate debt issuance are certainly skewed by low rates during the Covid era which led to corporations borrowing record amounts. January and February of this year saw roughly $150 billion each month in investment-grade corporate issuance. However, it is still noteworthy that March was such a light month. The banking crisis and associated market uncertainty were surely a big factor in March’s light issuance.

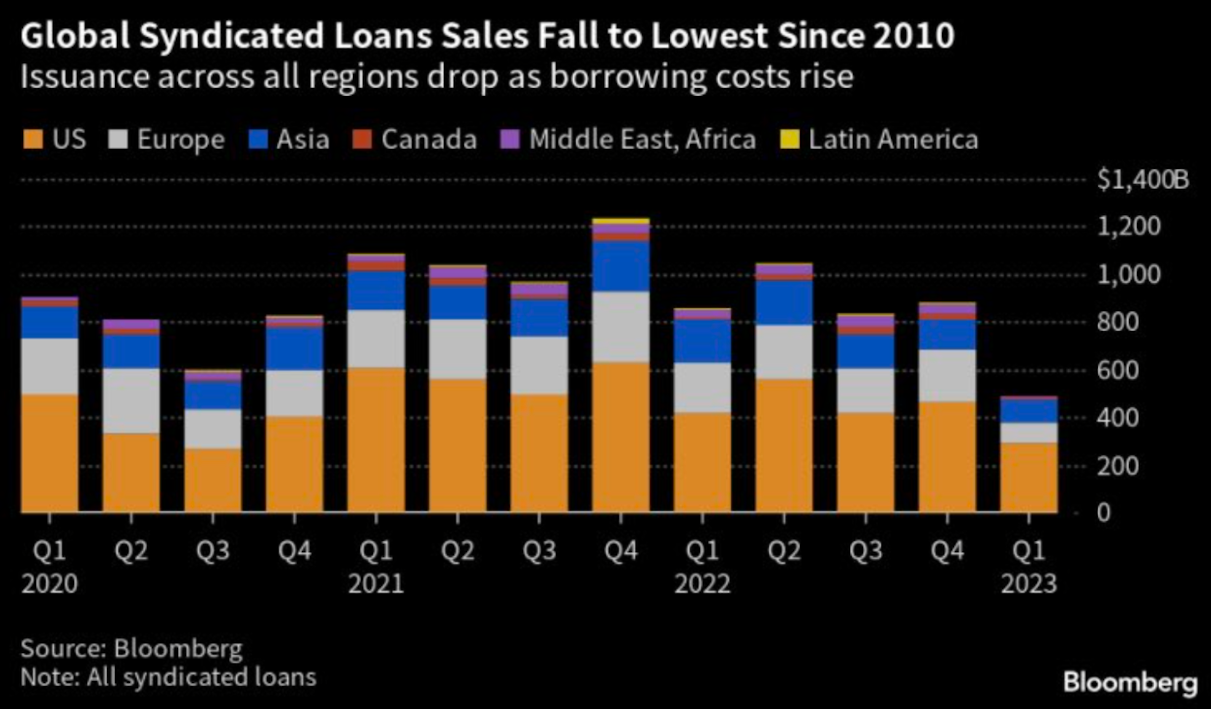

This trend can be observed in the syndicated loan market as well. The syndicated leveraged loan market is where large borrowers like corporations generally obtain loans from a group of arrangers like commercial and investment banks, which then sell them to other institutional investors like CLOs and private funds.

According to Bloomberg, global sales of syndicated loans fell -43% in Q1 to $493 billion, the lowest recording in 13 years.

Director of Leveraged Loans at AllianceBerstein, Scott Macklin, said “The new issue loan market was previously a Scooby Doo ghost town, especially after the bank failures,”

In addition, according to WSJ, corporations trying to raise in the high-yield junk bond market are finding it more challenging compared to when interest rates were low. These riskier corporations only raised around $5 billion in March, nearly 5x below the five-year average of $24 billion.

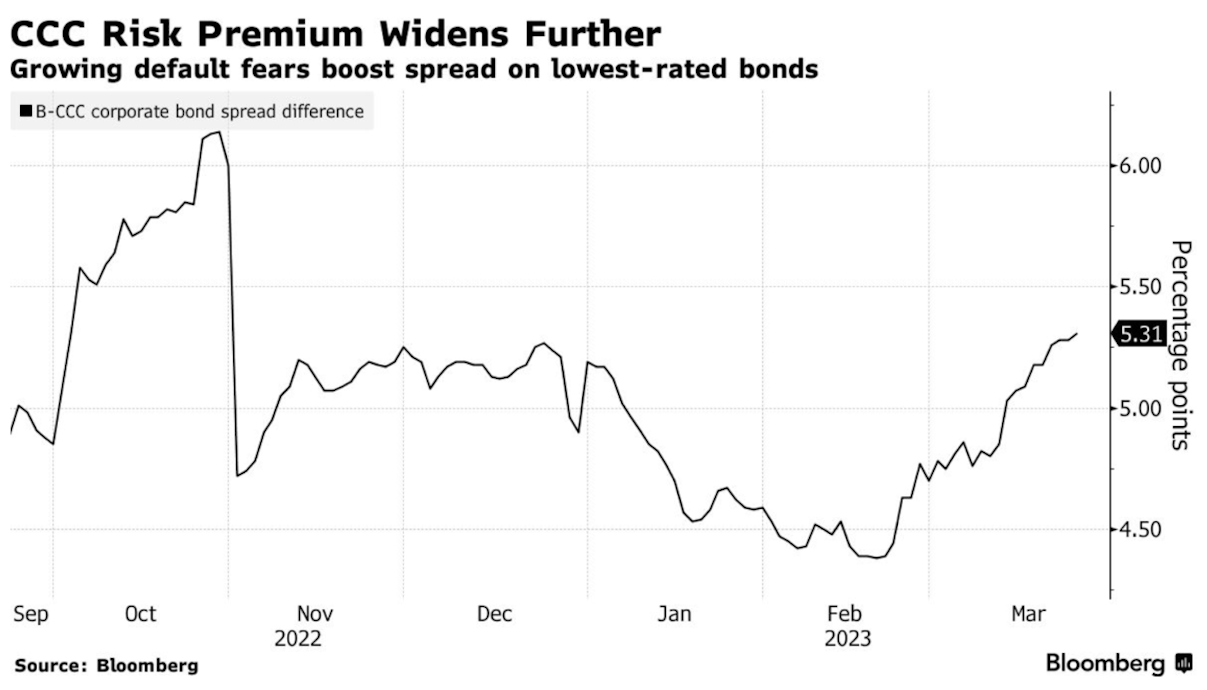

There was already evidence of the riskiest borrowers being left behind when the spread between the two riskiest tiers of bonds, B and CCC, continued to widen this month. It’s now around 531 basis points more expensive for CCC issuers to borrow compared to B issuers.

This spread is widening as investors are increasingly worried about the risk of defaults as the banking crisis unfolds, the Fed continues to hike rates, and many believe the economy is looking down the barrel of a potential recession. Traders no longer trust that these riskier corporations will be able to weather the storm, so they are seeking safer areas of the credit markets to invest instead.

The credit-based traditional financial system is built on trust, and right now, depositors don’t trust banks to protect their funds, banks are finding it harder to trust borrowers in this period of increased economic uncertainty, and corporations are finding it more difficult to raise capital. This is a toxic combination that could lead to a classic credit crunch which ultimately would result in slowing economic growth if it continues.

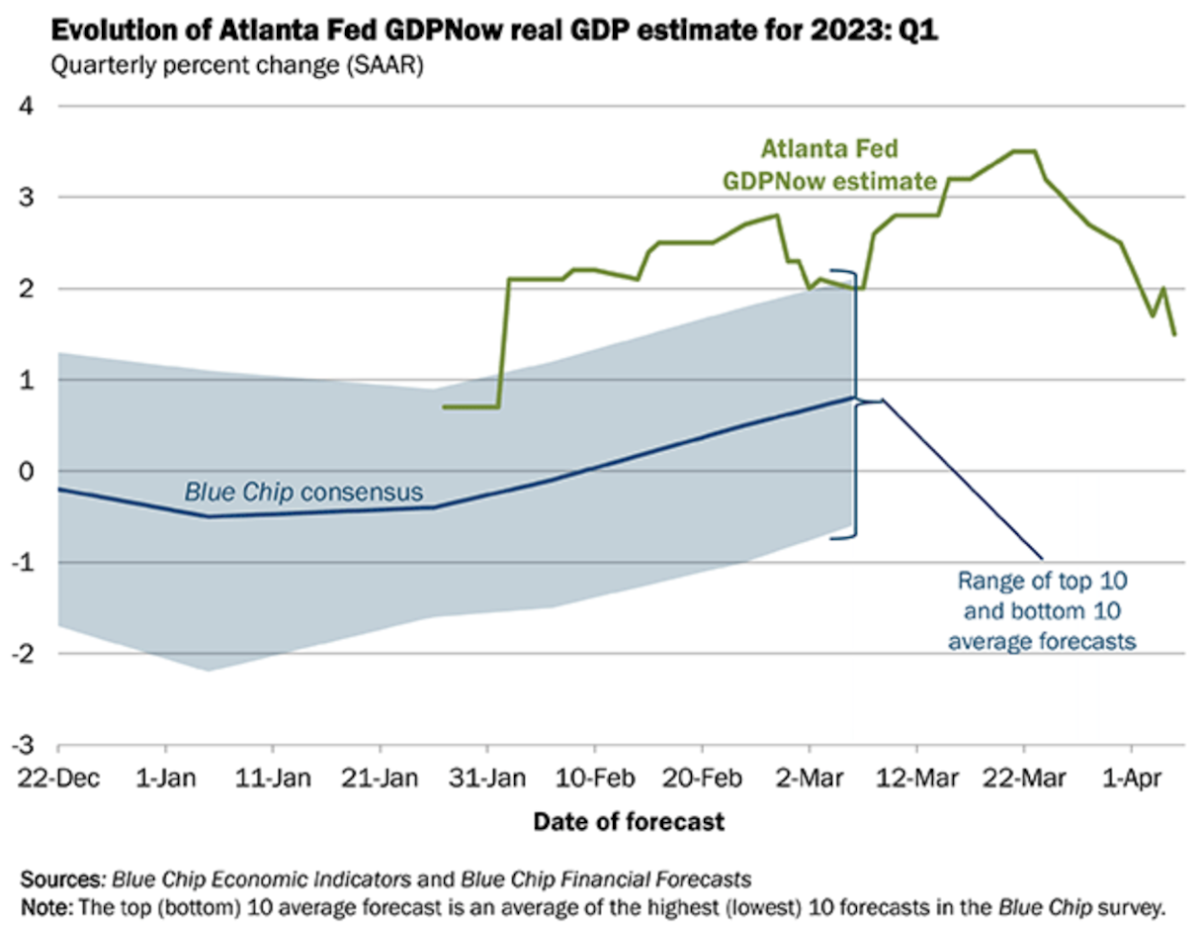

In fact, we are already seeing GDP estimates start to slow in response to the banking crisis and subsequent tightening in lending standards. The Atlanta Fed GDPNow estimate has now been cut in half to 1.5% from 3.5% only two weeks ago.

This reduction in GDP estimates is likely partly due to a week in which we saw a string of disappointing economic data releases. The ISM US Manufacturing Index contracted to 46.3, the lowest level in three years, and March ISM Services Index dropped significantly to 51.2, well below expectations, with new orders dropping from 62.6 to 52.2. Analysts expect tightening credit conditions to continue to impact these data points.

Employment metrics also disappointed to the downside with job openings coming in below expectations at 9.9 million openings, down from 10.6 million a month earlier. Company payrolls rose by just 145,000 for the month, down from an upwardly revised 261,000 in February and below the Dow Jones estimate of 210,000. These come with the unemployment rate still at a multi-decade low, so we will see if this trend in the labor market continues.

All of these dynamics point to decreased lending and slowing economic growth, which, all things considered, should be deflationary. But there was one development this week that added to the inflationary worries.

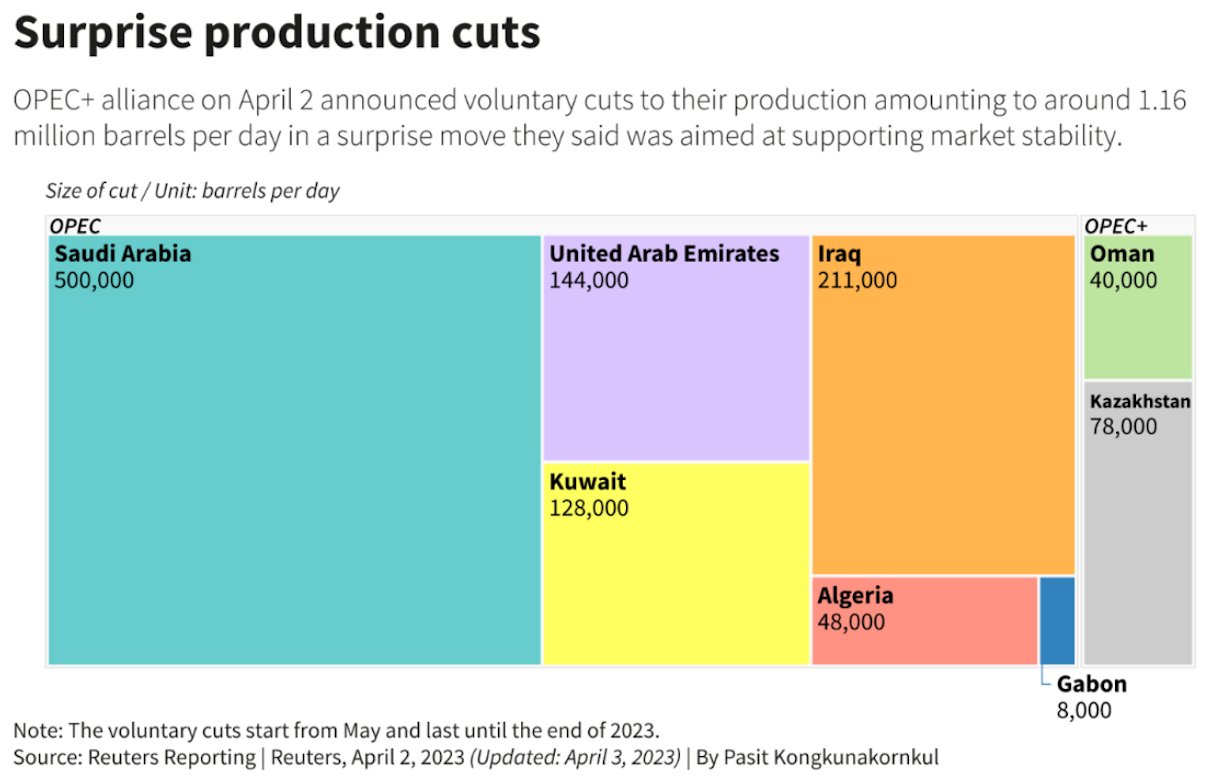

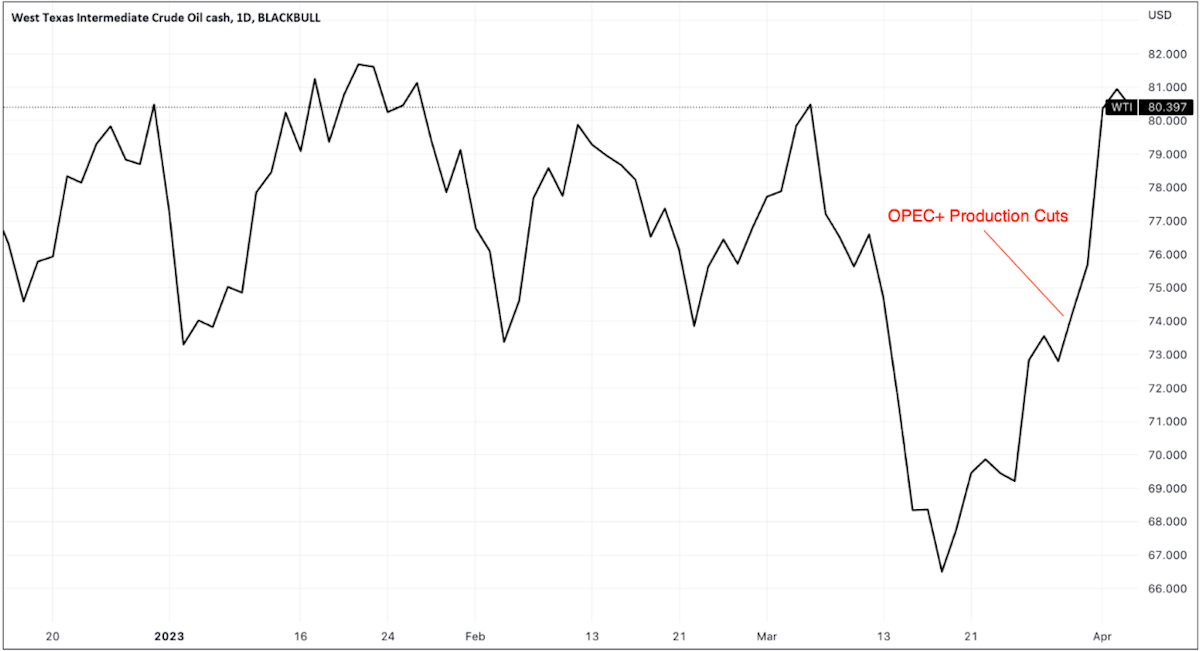

News came Sunday night that OPEC+ would cut its oil production across the board. The cuts will exceed 1 million barrels per day starting next month and continue through the end of the year.

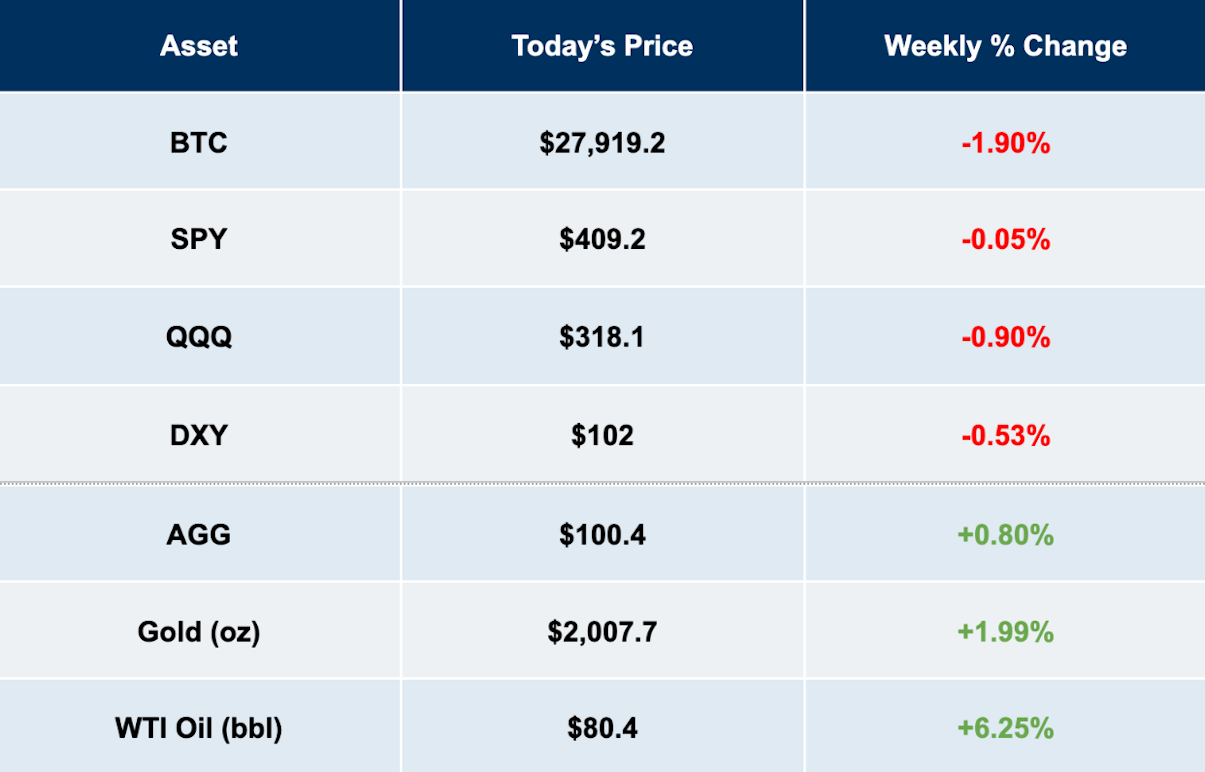

This reduction surprised markets, which had expected the cartel to hold output steady. In response to the production cuts, the price of oil shot up over 7% on Sunday night alone to over $80 per barrel.

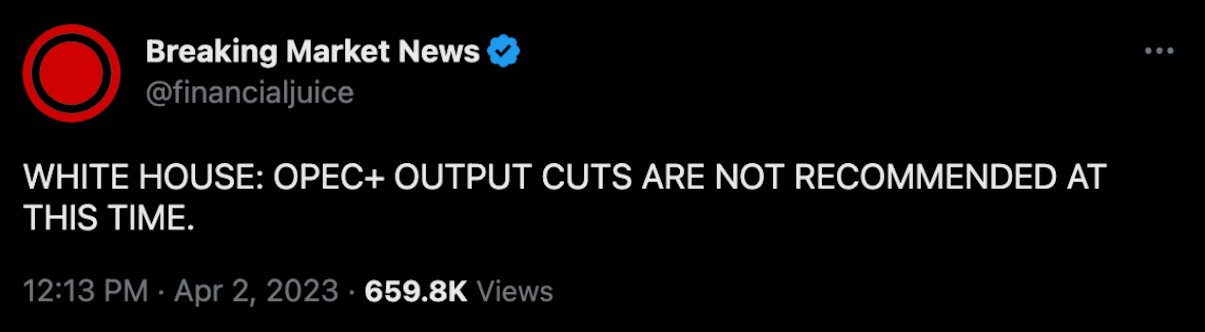

Analysts questioned why OPEC+ decided to cut production now, given the decision came outside OPEC+’s scheduled timetable for reviewing the supply and demand dynamics of the market. Some felt that this action was a geopolitical maneuver to keep the price of oil elevated to bolster US inflation as the Federal Reserve struggles to get it under control. The White House surely was not a fan of the OPEC+ decision, calling it “inadvisable.”

Others felt that this OPEC+ action was warranted due to signs of slowing oil demand. These net producers are cutting to bolster the price of oil in response to this low demand due to the importance of the price of oil to their local economies.

This recent OPEC+ move and the ongoing speculation around it is just another example of distrust growing in the global economy, this time, between countries.

This production cut comes as geopolitical tensions appear to be rising. Last week, the first yuan-denominated LNG trade occurred, leading to many headlines speculating on whether this is the beginning of the end for “King dollar.” Also, China and Brazil announced a new trade deal that bypasses the dollar. In addition, Xi Jinping and Vladimir Putin recently held talks in Moscow, which ended with Beijing and Moscow signing an agreement to bring about a “new era” of cooperation. President Xi Jinping wrote in a signed letter, “Our two sides have cemented political mutual trust and fostered a new model of major-country relations. Guided by a vision of lasting friendship and win-win cooperation, China and Russia are committed to no-alliance, no-confrontation and not targeting any third party in developing our ties. We firmly support each other in following a development path suited to our respective national realities and support each other’s development and rejuvenation.”

All of these developments point to a breakdown of trust in old trading relationships that could lead to a more fragmented, multipolar global economy.

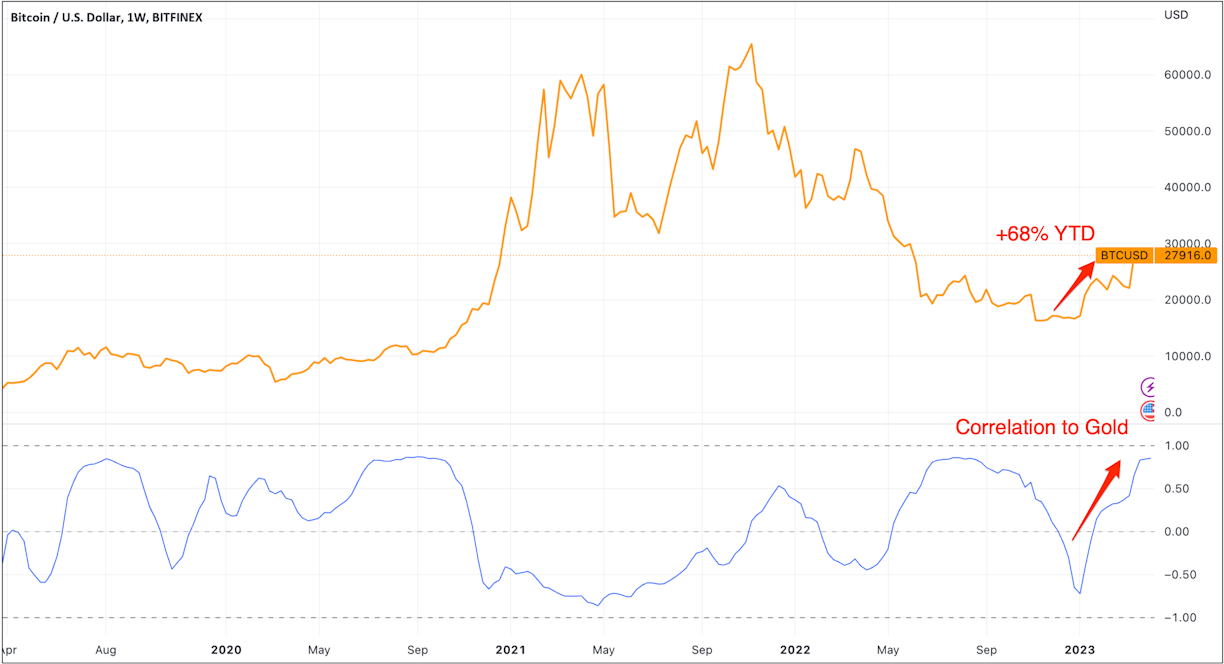

One of the best measures of growing distrust in the current monetary system is the price of gold. Gold recently broke through $2,000 per ounce and is nearing an all-time high.

This price action comes as central banks bought a record amount of gold in 2022, suggesting a geopolitical backdrop of mistrust and uncertainty.

And then there’s Bitcoin. Bitcoin is trustless digital money that was invented because of the inherent fragilities that exist in the trust-based credit monetary system. Just like gold, Bitcoin has benefited from the growing distrust spreading throughout the traditional financial system. Bitcoin is up +68% to begin the year and its correlation to gold has been growing steadily in 2023 as well.

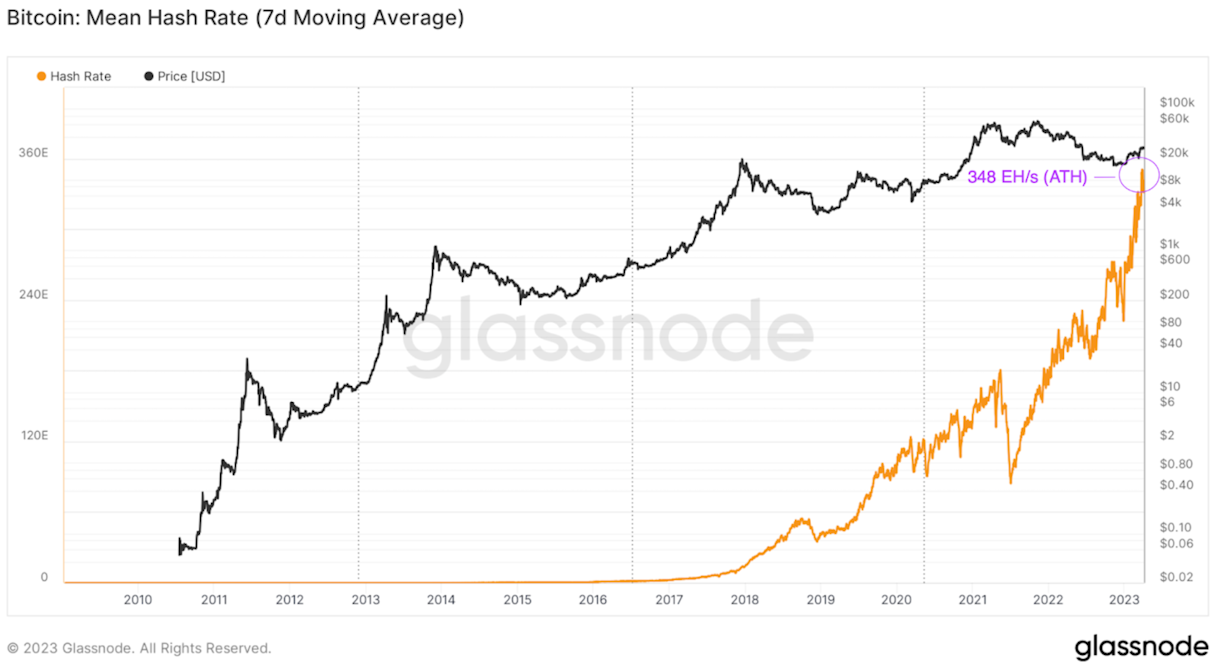

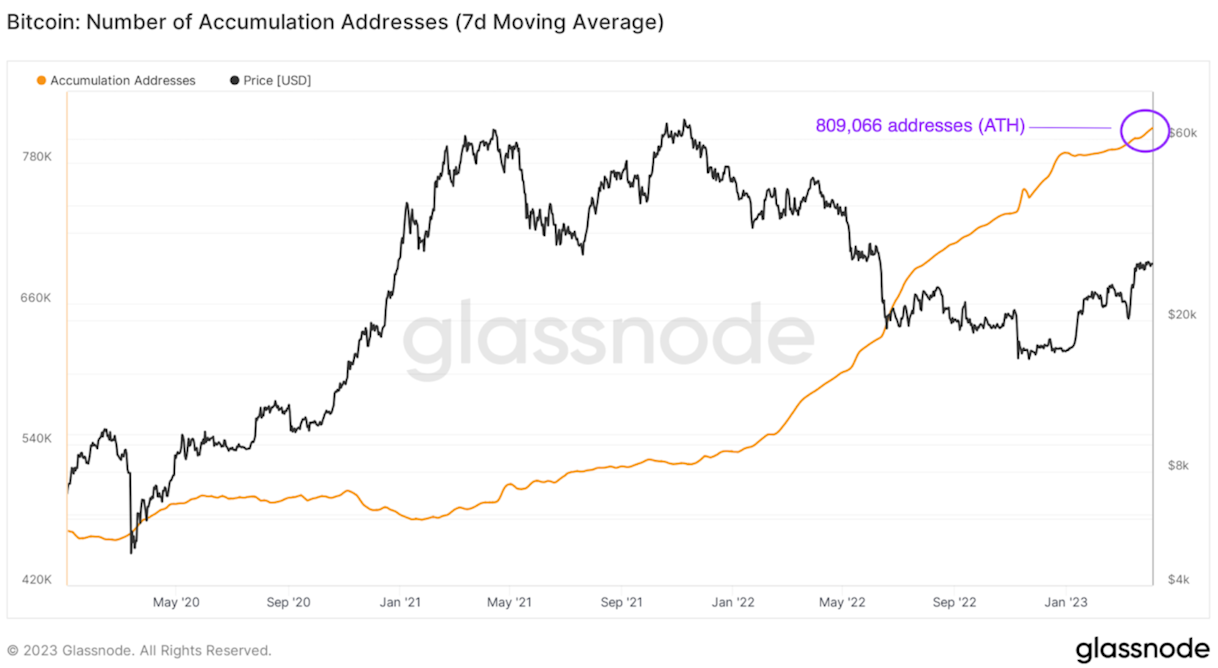

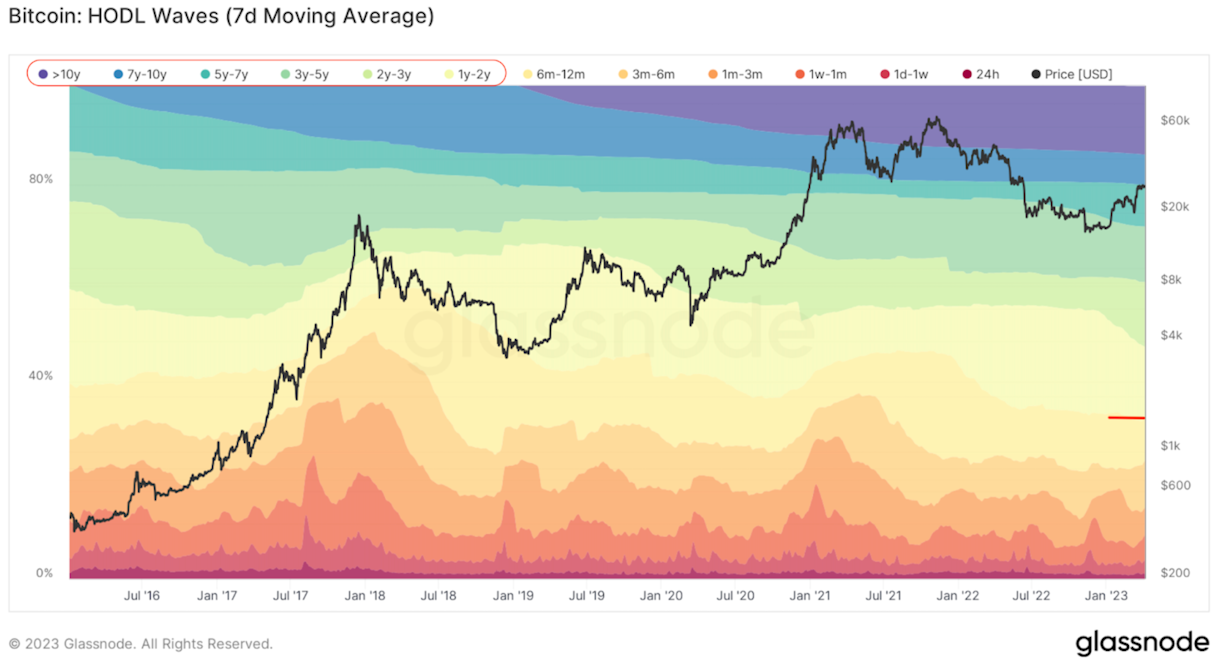

The increase in Bitcoin’s price has been even more impressive when one also takes into account some other metrics assessing the health of the network.

Bitcoin’s mean hash rate recently hit a new all-time high.

The total number of accumulation addresses, defined as addresses that have at least 2 incoming non-dust transfers and have never spent funds, has also reached an all-time high. Investors appear to be accumulating bitcoin at these bargain prices.

Furthermore, over 67% of on-chain, unspent Bitcoin transactions have not moved in over one year. Holders have continued to show unwavering conviction during this bear market. Diamond hands.

All of these charts, along with Bitcoin’s price action, paint a picture of strength and resiliency in the Bitcoin market, which is a stark contrast to what we are observing in the traditional financial system.

The rise of Bitcoin as the traditional banking system finds itself in turmoil has not gone unnoticed by regulators and market participants.

Since the fall of FTX in November, the broader cryptocurrency industry has come under severe regulatory scrutiny. Each week, there seems to be a new enforcement action, a new rule proposal, a new lawsuit, or a new cryptocurrency company leaving the U.S. due to regulatory uncertainty. In the past two weeks, we saw the SEC serve Coinbase a Wells Notice (a formal warning that they intend to recommend an enforcement action), Binance was sued by the CFTC for running an illegal derivatives exchange with poor compliance practices, cryptocurrency exchange Bittrex announced it will shutdown its U.S. operations due to regulatory uncertainty, and peer-to-peer marketplace Paxful announced it will be winding down operations due to “regulatory challenges…most heavily in the U.S.”

There has been a lot of conversation around whether these bank regulators’ actions are a top-down coordinated attack on the broader cryptocurrency industry. This has been dubbed “Operation Choke Point 2.0.” Since the start of the year, we have seen many different bank regulators crackdown on the crypto industry seemingly all at once. This came after two joint letters from the FDIC, Treasury, and Federal Reserve at the beginning of the year that outlined the increased risks for banks for doing business with cryptocurrency companies.

The main argument for why these recent coordinated actions are a form of illegal regulatory overreach was explained thoroughly in a white paper by the law firm Cooper & Kirk. A key excerpt:

“Operation Choke Point 2.0 deprives businesses of their constitutional rights to due process in violation of the Fifth Amendment. It is well settled that when a federal agency attaches a derogatory label to an individual or business, and this stigmatizing label causes the business to lose a bank account or broadly precludes them from the pursuit of their chosen trade, the agency has violated the Due Process Clause of the Fifth Amendment, unless if first afforded the individual or business a right to be heard.”

But has this really been a coordinated attack? Certainly, there has been some form of coordination, but that’s to be expected after billions of dollars of wealth was wiped out from the broader cryptocurrency industry that was selling unregistered securities to retail investors, and that was discovered to be full of fraudulent operations like Celsius and FTX.

Regulatory backlash is to be expected after some of the largest financial scams in recent memory were found to be pervasive in the broader cryptocurrency industry, as we have been saying here at Swan for years.

Regulators were caught asleep at the wheel and are now trying to do their jobs and protect people from unregistered securities, Ponzi schemes, and other scams. The fact of the matter is the law t clearly states what is and what isn’t a security. It doesn’t matter whether I or anyone else agrees with the law. If you think that retail investors should be protected from fraud and unregistered penny stocks, then you should feel the same about the cryptocurrency industry. To say otherwise would be morally inconsistent and hypocritical.

So right now, we are seeing a regulatory backlash in the wake of these cryptocurrency blowups. Bitcoin will continue to shine as a winner in the long term as the only cryptocurrency that is truly leaderless and decentralized. The other winners will be Bitcoin-only companies with honest operations who purposefully avoided providing their customers with access to other cryptocurrencies.

Banks will continue to decide on a case-by-case basis whether they want to increase their compliance costs by servicing Bitcoin companies. Some will say “no, ” but some will say “yes” because of the potential increased revenues that come from servicing an innovative new industry. There will always be a banker incentivized to bring in new business to the bank.

Whether this is a coordinated top-down attack or not is up for debate, and regulators coming out in full force against these cryptocurrency firms and projects that harmed retail investors should be expected. In the end, we think this helps Bitcoin adoption long-term. The broader cryptocurrency industry has long confused newcomers with false marketing and siphoning investor demand away from Bitcoin into inferior tokens. A regulatory attack on “crypto” will help cleanse the industry of bad actors and scammy projects, and will help speed up the demand for digital sound money, just as the world is beginning to need it more than ever before.

Market Overview

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Swan Guard brings world-class Bitcoin security with advanced risk controls, scam defense, and expert support — vigilantly protecting your Swan account and safeguarding your Bitcoin.

After managing a Swiss gold fund for 8 years, I realized Bitcoin surpasses gold as the ultimate store of value. Here’s why every gold investor should study Bitcoin closely.

Ben Werkman joins Swan as CIO. New LBE primer explains key concepts, implementation steps, risk management, and valuation approaches.