Swan Vault Plus: Human-Verified Withdrawal Protection

Live video verification, Jade Plus signing devices, and a purpose-built recovery assistant give families and businesses greater control over their Bitcoin.

It’s no secret that younger generations increasingly feel like they are falling behind. Millennials face an affordability crisis. They are on track to be the first-generation not to exceed their parents in terms of job status and income.

It’s no wonder that a recent study published in JAMA Psychiatry on well-being across generations found that younger generations’ life satisfaction scores were lower across the board compared to their older counterparts.

Part of this widespread dissatisfaction is related to financial instability. I would argue a lack of financial security could be one of the most significant contributors to the negative sentiment felt by younger generations today.

Millennials are a generation that has already experienced two “once-in-a-lifetime” global financial crises since they entered the workforce. They were just starting to accumulate savings as the Federal Reserve pumped asset prices to the moon with their accommodative policies. Instead of benefitting from that asset appreciation, most millennials were left behind.

In Neil Howe’s recently published book, “The Fourth Turning is Here, ” he touches on how millennials are the most likely to believe that the current regime is fundamentally broken and needs to be overhauled, if not replaced entirely. He explains how young people don’t have hope today. They don’t feel like a future exists.

In this piece, I will break down some statistics that help illuminate why millennials feel this way, how the fiat system has failed them, and why Bitcoin could act as a saving grace for these younger individuals.

Homeownership is often considered the cornerstone of the American Dream. It is how households have historically built generational wealth, and it provides individuals with the space necessary to build families and create a legacy. Homeownership is deeply ingrained in the American psyche as a symbol of stability and success.

Today, due to central bank and government policies, home affordability stands at the lowest level in history.

This is a result of a combination of two things:

1.) Soaring home prices boosted by policy responses in the wake of the Global Financial Crisis

2.) the Federal Reserve hiking interest rates to combat soaring inflation.

Below is a chart highlighting the Federal Reserve’s balance sheet and the median U.S. home price since 2010. The trend is clear. As the Federal Reserve has performed massive amounts of Quantitative Easing over the last decade, buying up billions in mortgage-backed securities, the price of homes has sky-rocketed almost in tandem.

For older generations who already owned homes, this was fantastic. Central bankers pumped the value of their homes (and their net worth) without them lifting a finger. But for millennials who were still looking to purchase their first home after just entering the workforce, this was a catastrophic development. The Federal Reserve has been directly complicit in pushing the American Dream of homeownership out of reach for a large portion of millennials.

This is confirmed in the data when comparing millennial homeownership to that of previous generations. According to Apartment List, millennials have had the slowest transition from renters to homeowners. By age 30, 42% of millennials owned their homes, compared to 48% of Gen Xers, 51% of baby boomers, and nearly 60% of silents at the same age.

Millennials have been forced to become renters due to the high cost of homeownership today. This significantly impacts their ability to build long-term wealth. According to a 2019 Survey of Consumer Finances from the Federal Reserve, the median homeowner has 40 times the household wealth of a renter — $254,900 for the former compared to $6,270 for the latter.

Homeownership is not just about building wealth, though. A British study looked at data spanning multiple decades and found that being a homeowner has consistently been linked to a higher probability of conceiving a first child than those who rent over the last 30 years.

This corroborates a recent trend we’ve witnessed — the rapid decline in fertility and birth rates. Millennials are simply not having babies like previous generations. A 2021 Pew study found that 44% of non-parents ages 18 to 49 say it is not too or not at all likely that they will have children someday, an increase of 7 percentage points from 37% in 2018.

The number two cited reason behind medical reasons? “Financial reasons.”

Instead of starting families and owning homes — two critical milestones for financial success and long-term fulfillment — younger people are moving back in with their parents.

According to a recent Bloomberg study, a whopping 50% of people aged 18 to 29 live with their parents today and cite financial woes as the number one reason they choose to move back in.

Young people are moving back in with their parents to try to save money to maybe own a home one day. But they might be disappointed with how long they will have to stay there.

Today, it’s estimated that buying an average-priced home takes nearly 7 years of saving an average incomee. To put that into perspective, it took 2.4 years of time and labor to save for the cost of an average home in 1970.

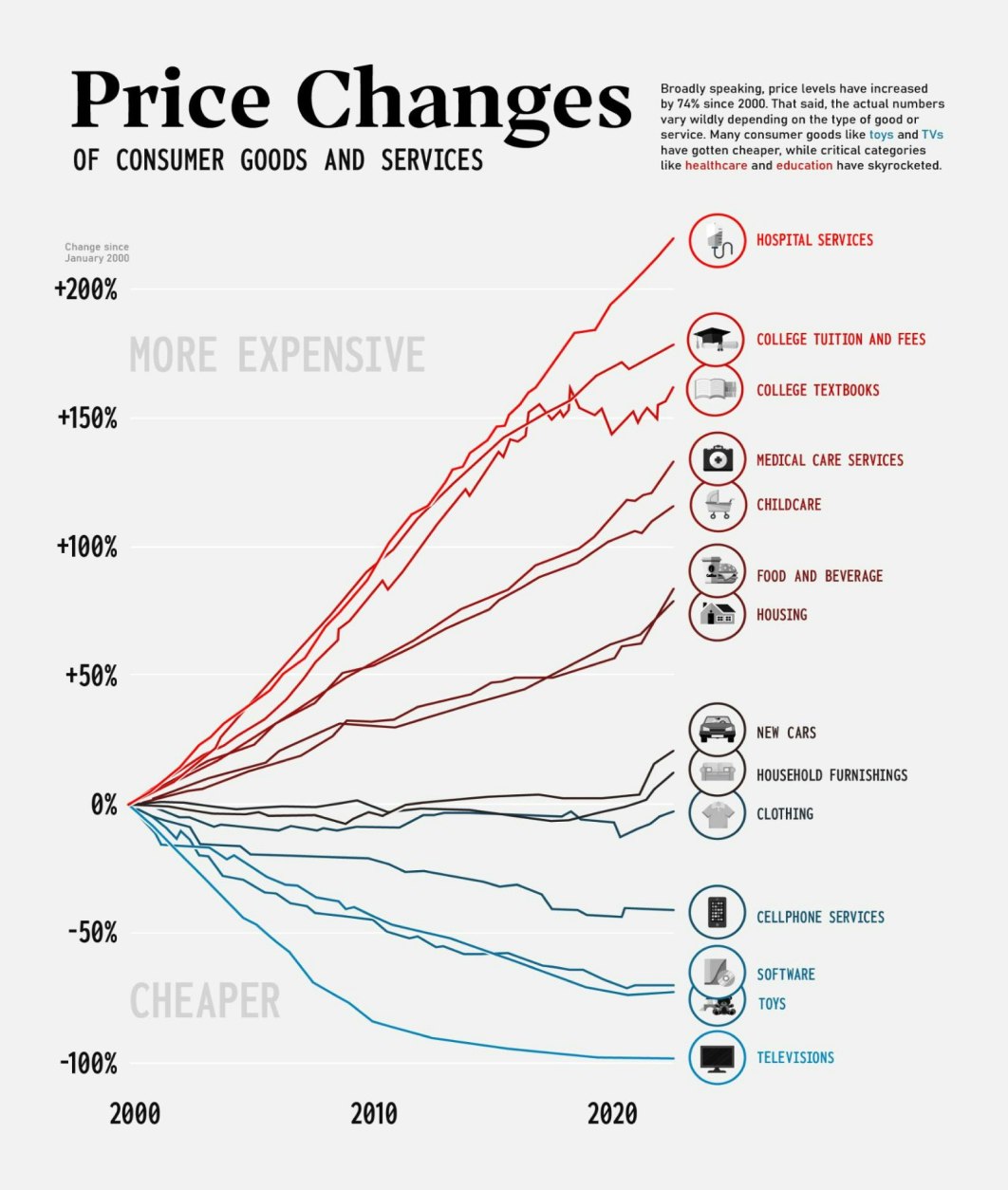

Younger folks are moving back in with their parents instead of focusing on starting families because living costs have soared. Inflationary policies have not only made homes unaffordable, but they have also increased the cost of essentials like food, healthcare, education, and transportation. Having and supporting a family has never been more expensive than today.

According to American Compass Executive Director Oren Cass, it now takes 62 weeks for a single-income family working at the median wage to afford essentials.

Given that there are only 52 weeks in a year, it’s not hard to see why this estimation is problematic.

This has occurred in part because nominal wages have remained stagnant. When comparing median income and median wealth between generations at 40 years old, one can see how wages have gone nowhere for millennials, while median wealth has declined, and median debt has soared.

When taking into account inflation, the picture gets worse. One can see that wage stagnation has been an ongoing trend for decades. A 2018 Pew research study showed how paychecks may have increased nominally, but they haven’t moved much in terms of purchasing power.

So, as wages have gone sideways, the cost of everything millennials need, like healthcare, education, and housing, has skyrocketed.

This has led to millennials acquiring more debt than any other generation before it, as they took on student loans, auto loans, mortgages, and credit card debt to try to make ends meet.

Total household debt for individuals aged 30-39 has increased 27% since 2019. It is the fastest pace of debt accumulation over a three-year period since the 2008 financial crisis.

Millennials are going into more and more debt to desperately try to achieve the American Dream that is moving farther and farther out of reach.

One viable option is investing in an asset with a strong potential to appreciate significantly in the coming decade. This would allow millennials to finally feel like they have caught up, and if it outperforms the rate of inflation and home prices, it could improve their quality of life and potentially allow them to finally purchase that home.

Bitcoin is an asset with a relatively small market capitalization. It’s still early in its adoption cycle, but if network adoption continues at its current trajectory, Bitcoin will demand a higher price, potentially much higher.

Given that the supply is fixed at 21 million, the more users that join the network, the higher the price of Bitcoin will go. Since Bitcoin’s supply is set in stone, only the demand side of the equation matters, and demand for a scarce, censorship-resistant, private, and digital monetary good seems to be increasing.

The chart below shows how the number of addresses holding at least $100 worth of Bitcoin has been growing at a steady rate.

Bitcoin is considered an “asymmetric bet” in the investment world. An asymmetric bet is an investment with a significant upside gain than the potential downside loss. In other words, you can invest a little to potentially return a lot.

Bitcoin’s track record is impressive. It has outperformed nearly all asset classes over long periods. Bitcoin’s compound annual growth rate far exceeds other asset classes like gold and the S&P 500 over longer time frames.

Not only is the potential return on investment attractive to millennials, but the beauty of Bitcoin is that they wouldn’t need to get approved for a mortgage to buy some. Millennials don’t need to buy a whole Bitcoin; they can purchase a fraction of one. And they can actually own Bitcoin without any debt attached. For many millennials, Bitcoin could be a way to build wealth when all other alternatives feel out of reach.

… And this is where millennials find themselves today. The fiat system has given them two recessions, stagnating wages, artificially inflated the price of homes, and has saddled them with copious amounts of debt just to keep up with the soaring costs of essentials like healthcare, food, energy, education, and transportation.

Bitcoin represents an opportunity to improve the well-being of this generation that has been dealt a bad hand. As such, Bitcoin symbolizes hope for a generation who increasingly feel their futures have been stolen from them by the traditional fiat system.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Live video verification, Jade Plus signing devices, and a purpose-built recovery assistant give families and businesses greater control over their Bitcoin.

Passkeys enable faster, more secure device-based logins (face/fingerprint) that reduce password risks and strengthen our Swan Guard security protections.

Swan Generations provides a unique service for parents, legal guardians, and others to make irrevocable gifts of real Bitcoin.