This Time is Different

No longer a niche commodity, Bitcoin now finds itself a prime fixation of the US Executive Branch.

In this article

Timing Bitcoin trades can be an extremely stressful endeavor; why not take the pressure off with dollar-cost averaging?

TL; DR: Bitcoin dollar-cost averaging (DCA) is a strategic investment approach that involves regularly investing a fixed amount in Bitcoin regardless of its price. This method reduces the risk associated with market volatility, simplifies the investment process by eliminating the need to time the market, lowers emotional stress by promoting a steady investment mindset, fosters disciplined saving and investing habits, and supports long-term growth by leveraging Bitcoin’s potential for appreciation over time.

Dollar Cost Averaging (DCA) is an investment strategy where you invest a fixed amount of money into an asset, such as Bitcoin, at regular intervals, regardless of its price.

Recurring Buys: A dollar-cost average (DCA) strategy is also commonly referred to as 'recurring buys or puchase.'

Consistent Investment: DCA involves investing a fixed amount of money into Bitcoin at regular intervals, regardless of the price. This approach helps mitigate the impact of market volatility.

Reduced Risk: By spreading out investments over time, DCA reduces the risk of investing a large amount in Bitcoin at a market peak, thereby lowering the potential for significant losses.

Simplicity and Discipline: DCA simplifies investment, removing the need to time the market. Investors set a schedule (daily, weekly, monthly) and stick to it, promoting disciplined investment habits.

Cost Averaging: Over time, DCA can help achieve a lower average cost per Bitcoin unit compared to making a one-time purchase, as it takes advantage of market fluctuations.

Emotional Management: This strategy helps manage emotions by avoiding impulsive decisions based on short-term market movements, allowing investors to focus on long-term goals.

Sign up with Swan

Visit the Swan Bitcoin website.

Click on the “Get Started” or “Sign Up” button.

Enter your email address to create an account.

Log in with your link

After signing up, you will receive a “link” in your email.

Open your email and click the link to log in to your Swan account.

Verify your identity

Follow the on-screen prompts to verify your identity.

You will need to provide personal information and documentation (such as a photo ID) to comply with KYC (Know Your Customer) regulations.

Link your bank account

Once your identity is verified, proceed to link your bank account.

Provide your bank account details and authorize Swan to make transactions.

Start your savings plan

Set up your recurring buy plan by choosing the amount you want to invest and the frequency (daily, weekly, or monthly).

Confirm the details and start your automated Bitcoin savings plan.

Swan will automatically withdraw funds from your bank account and purchase Bitcoin according to your specified schedule.

NOTE: DCA’ing Bitcoin is a similar strategy to investors who automatically reinvest dividends from stocks into buying more shares in several ways:

Consistency

Dividend Reinvestment: Automatically reinvesting dividends ensures that you consistently put any earned dividends back into the stock, buying more shares regularly whenever dividends are paid.

DCA in Bitcoin: With DCA, you invest a fixed amount of money into Bitcoin at regular intervals (e.g., weekly, monthly), regardless of the price.

Cost Averaging

Dividend Reinvestment: By reinvesting dividends automatically, you buy shares at different price points, which can average out your cost basis over time.

DCA in Bitcoin: Similarly, by purchasing Bitcoin regularly, you buy at various prices, averaging your cost basis and potentially mitigating the impact of market volatility.

Compounding Growth

Dividend Reinvestment: Reinvesting dividends helps compound growth since the dividends buy more shares, which can earn more dividends.

DCA in Bitcoin: Regular investments in Bitcoin can lead to compounding growth if the value of Bitcoin increases over time.

Passive Strategy

Dividend Reinvestment: This is a passive investment strategy where the reinvestment happens automatically, requiring no active management.

DCA in Bitcoin: DCA is also a passive strategy. You set a schedule and amount to invest, automating the process to avoid market timing.

Long-term Focus

Dividend Reinvestment: This strategy is typically part of a long-term investment plan aimed at growing the value of your portfolio over time.

DCA in Bitcoin: DCA is often employed by those looking to build their Bitcoin holdings over the long term without worrying about short-term price fluctuations.

Both strategies leverage regular and automatic investments to reduce the impact of market volatility and focus on gradual growth over time.

Bitcoin is well known for its volatility. Typically initiated after a supply issuance halving, Bitcoin bull markets have exceeded 100x returns, contrasted against bear market corrections that can dip as low as 70-80%.

How does one choose an entry point without losing one’s mind (or one’s pants)?

There are two main ways of investing — lump sum and dollar cost averaging.

Lump Sum Investing: involves taking your desired allocation of a particular asset and throwing it all in at once.

Dollar Cost Averaging: spreads the investment, allowing individuals to build their positions over time.

Swan has extensively analyzed the difference between lump sum and dollar cost averaging. Generally speaking, a lump sum is mathematically superior, but that doesn’t account for the toll volatility can take on the human psyche.

NOTE: Most of the time, Bitcoin goes sideways or down. It’s only a select few days that Bitcoin goes up, but when it does, it really goes up. It’s best to avoid trying to time those things.

We’ll discuss this in more detail below.

Dollar-cost averaging shines during the manic price run-ups that Bitcoin has experienced every few years. Often characterized as bubbles, these run-ups are unpredictable, and nobody really knows if, when, or how far the price will fall following an exponential trend.

This following chart demonstrates, however, that when you buy the top with a lump sum purchase, it takes as long as 1,227 days to return to your break-even point.

Swan Bitcoin

Talk about some severe pain.

On the flip side — if you resist the urge to FOMO all-in to Bitcoin in a bull market, your dollar cost average has the potential to buy dip after dip… all the way down the other side of that price peak. The result is a potentially significant reduction in the days it takes to break even after a bear market correction.

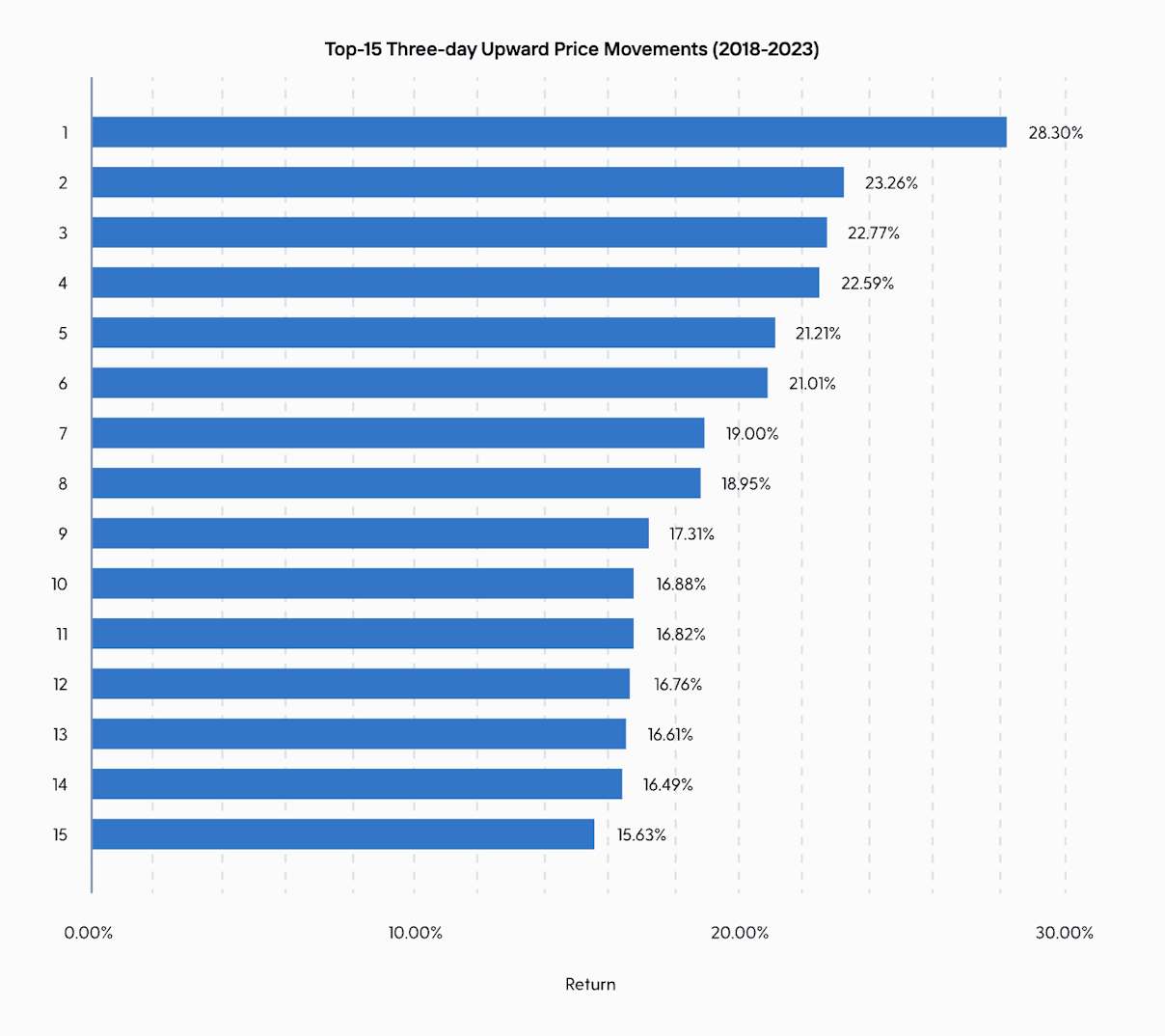

Swan analysis illuminates just how risky trying to time the market can be. The chart above shows the 15 highest 3-day return periods for Bitcoin from 2018-2023.

Swan Bitcoin

That’s 45 days out of 1,826 — or only 2.5% of the time!

“If an investor had missed these 15 largest 3-day periods during this time period, their total return was -84.6%. This was during a period when the total return of Bitcoin increased by +127%!.”

By dollar-cost averaging, you avoid the age-old decision pitfall of trying to time the market and missing out on the gains. Trading is ultimately a loser game, with very few participants making money. Time in the market is much more important than timing the market.

Remember that gym you signed up for after your New Year’s resolution 2017?

It took you about 3 and a half years to realize you were still paying for the membership even though you only went for the first two months. That’s basically dollar cost averaging—with the caveat that it’s actually a productive expense to forget about.

Dollar-cost averaging promotes disciplined investing by taking the discipline out of it entirely. Set it and forget it, then let your money work for you. DCA also removes emotional baggage from the equation — provided you have the discipline to stick to your plan.

Generally speaking — the purpose of a plan is to make decisions ahead of time so you don’t have to think as hard.

Imagine this scenario:

Bitcoin hit $69k for the second time this year. Every analyst is calling for an imminent run to $100k by the end of the year.

Bitcoin dips to the $50k mark from there. Influencers are adamant it’s a temporary and healthy price correction before continuing on the moon trajectory.

What’s a guy to do?

Stick to the DCA plan and do nothing?

FOMO buy the dip with the rest of your liquid savings?

If you said 2, unfortunately, you were in for a lot of pain. Bitcoin continued to grind lower for 12 straight months, eventually hitting as low as $16k. DCA for the win in this scenario. Emotional FOMO buyers be forewarned.

Encouraging long-term investment strategies

Schwab studies also validate these claims — timing the market is proven repeatedly to be a fool’s errand. Of course, timing the market ideally would increase your returns — that’s an obvious conclusion, but how hard is it actually to do that.

As mentioned above, it only took 45 days out of 5 years to flip your returns from 127% to -84.6%. That’s the magic of DCA’ing Bitcoin. You can get outsized returns from effectively doing nothing. Set it and quite literally forget it.

Explanation of how dollar-cost averaging can potentially result in higher returns

Taking advantage of market dips and fluctuations

Examples of successful dollar-cost averaging strategies

Dollar-cost averaging does not necessarily have higher returns than lump sum investing; it’s more of a tool to manage price risk and emotions and help build your position in a way that won’t keep you up at night.

That being said, DCA’s performance speaks for itself through cost-weighted autoregulation for those of us without six-plus figures of cash to throw around at a time.

Check out this Swan research piece on Lump Sum vs. DCA investing for an in-depth analysis of optimal strategies. For those seeking the cliff notes version- here are the key points:

In general, lump-sum strategies outperform DCA strategies, except when individuals invest all their available funds right before an extended period of downward price action.

The longer an investor took to deploy capital, the more they underperformed compared to a lump-sum investment.

Dollar-cost averaging adds flexibility to your portfolio by preventing you from getting in too deep, too fast.

Let’s illustrate this using the classic Davey vs. Ben example:

Davey

Davey decides to get in on that Bitcoin price action before it shoots off to the moon and never returns again.

He invests 10% of his net worth in Bitcoin in a single transaction.

Later that week, Bitcoin dropped 15% in a day over unfounded regulatory concerns. Davey has a panic attack and sells his entire position at a loss.

Ben

Ben decides to allocate strategically to Bitcoin to preserve his family’s wealth and purchasing power for generations.

Ben starts a dollar-cost averaging plan amidst the early 2021 bull market hype.

Ben feels the pull of FOMO as Bitcoin takes off towards all-time highs but resists the urge to break from his plan.

Ben buys the 2021 top.

Ben buys the 2023 bottom. Ben buys every price in between the two and beyond.

It is now 2024, and Bitcoin is hovering below all-time highs, but Ben’s investment is significantly in the green. He’s inadvertently over-allocated to Bitcoin based on his original goals. Still, he understands what he owns now and continues to accumulate regardless.

Earn Free Bitcoin as part of your DCA strategy. Learn more.

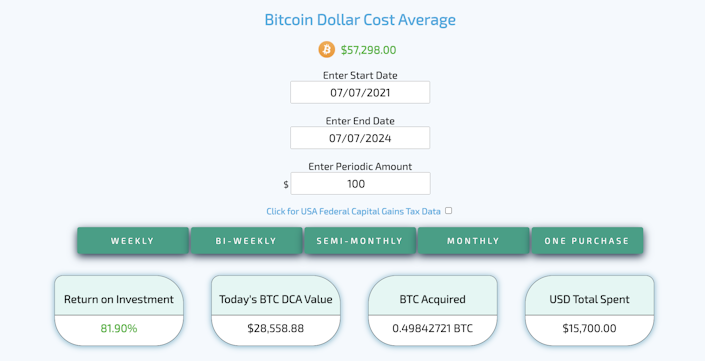

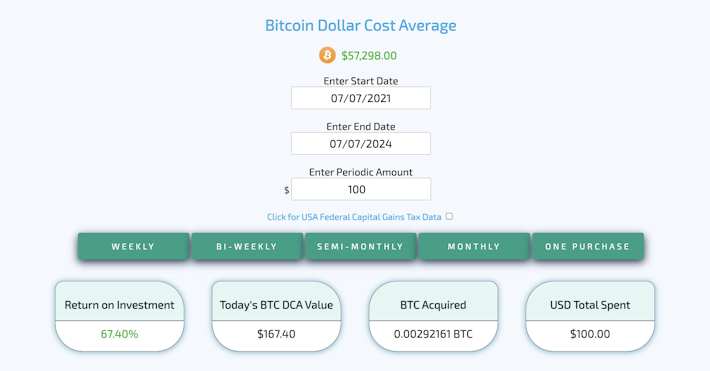

Start your children out young and set up a recurring buy plan and start stacking sats with Swan. By the time they reach 18, the price could be in $100,000's.

Don’t use Coinbase for DCA. You don’t own the BTC in the account and Coinbase is consistently in trouble with the U.S. government. Learn how to delete it in 3 simple steps here.

Fees: 0.99%*

Custody Provider: BitGo Trust Company

Trustpilot Rating: 4.6 / 5 out of 1,136 reviews

Apple App Store: 4.8 / 5 out of 1.5k reviews

Google Play Store: 4.4 / 5 out of 619 reviews, 50,000+ downloads

Account Minimum: $2

Investment Options: +150 alternative cryptocurrencies

Fees: 0.5% to 4.5%

Custody Provider: Coinbase Custody Trust

Trustpilot Rating: 1.8 / 5 from 9,351 reviews

Apple Store App: 4.7 / 5 from +1.7M reviews (#13 in Finance)

Google Play Store: 4.5 / 5 from +839k reviews, +10M downloads

Keep those hands diamond — be a Bitcoin Ben and just say no to FOMO. Adjusting investment amounts based on personal financial situation

Dollar-cost averaging also allows flexibility based on personal financial circumstances. Though Bitcoin is a great long-term store of value, I wouldn’t necessarily classify it as a savings account just yet.

If you allocate too much and need some cash, you could sustain some losses in the short term. If you build your position with patience through dollar-cost averaging, you can always put it on pause to address emergencies without having to panic sell.

Sign up for Swan today!

Hold your IRA with the most trusted name in Bitcoin.

Mickey Koss became a freelance writer in the Bitcoin space in an attempt to build a proof of work portfolio for when he left the Army. He graduated from West Point with a degree in Economics before serving in the Army for nearly a decade. He became orange pilled in graduate school and is now a regular contributor to Forbes, Bitcoin Magazine, and Bitcoin News. He’s been on popular podcasts such as BTC Sessions’ Why Are We Bullish, and is a regular on Café Bitcoin.

Drew, a class of 2013 Bitcoiner, is a Research Analyst for Swan Bitcoin.

He has worked in institutional VC/PE, FinTech, and DLT consulting for over six years. He also brings over twelve years of experience working with national nonprofits and start-ups in education and software development in several leadership roles.

Thoughts on Bitcoin from the Swan team and friends.

No longer a niche commodity, Bitcoin now finds itself a prime fixation of the US Executive Branch.

The SAB 121 repeal mirrors the end of Glass-Steagall in 1999, which played a major role in the 2008 financial crisis. Bitcoiners should listen to history and be more cautionary about SAB 122.

Bitcoin is the only digital asset that meets the necessary criteria for a sovereign reserve, given its decentralization, liquidity, security, and geopolitical significance.