Swan Private Market Update

This report was originally sent to Swan Private clients on February 24th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

This report was originally sent to Swan Private clients on February 24th, 2023. Swan Private guides corporations and high net worth individuals globally toward building generational wealth with Bitcoin.

“Welcome those big, sticky, complicated problems. In them are your most powerful opportunities.” — Ralph Marston

High levels of inflation continue to be the main concern for individuals, businesses, and policymakers in 2023. The recent CPI inflation did not do much to quell these worries as January CPI came in above expectations at +6.4% YoY, down 10 bps on the month. But, of course, there was nuance in this headline number.

Most of the disinflation continues to occur in goods, with core goods CPI rising +1.4% in January and core services rising +7.2%. The overall declines in the headline CPI number were isolated in goods like used autos, but wages remain sticky. This is notable because Fed Chairman Jerome Powell made it clear that Core CPI service ex-shelter was a metric that he was tracking closely to measure how much inflationary pressures have eased. This metric declined 10 bps MoM but remains sticky at +6% YoY. This increases the likelihood that the Fed will have to hike higher and for longer.

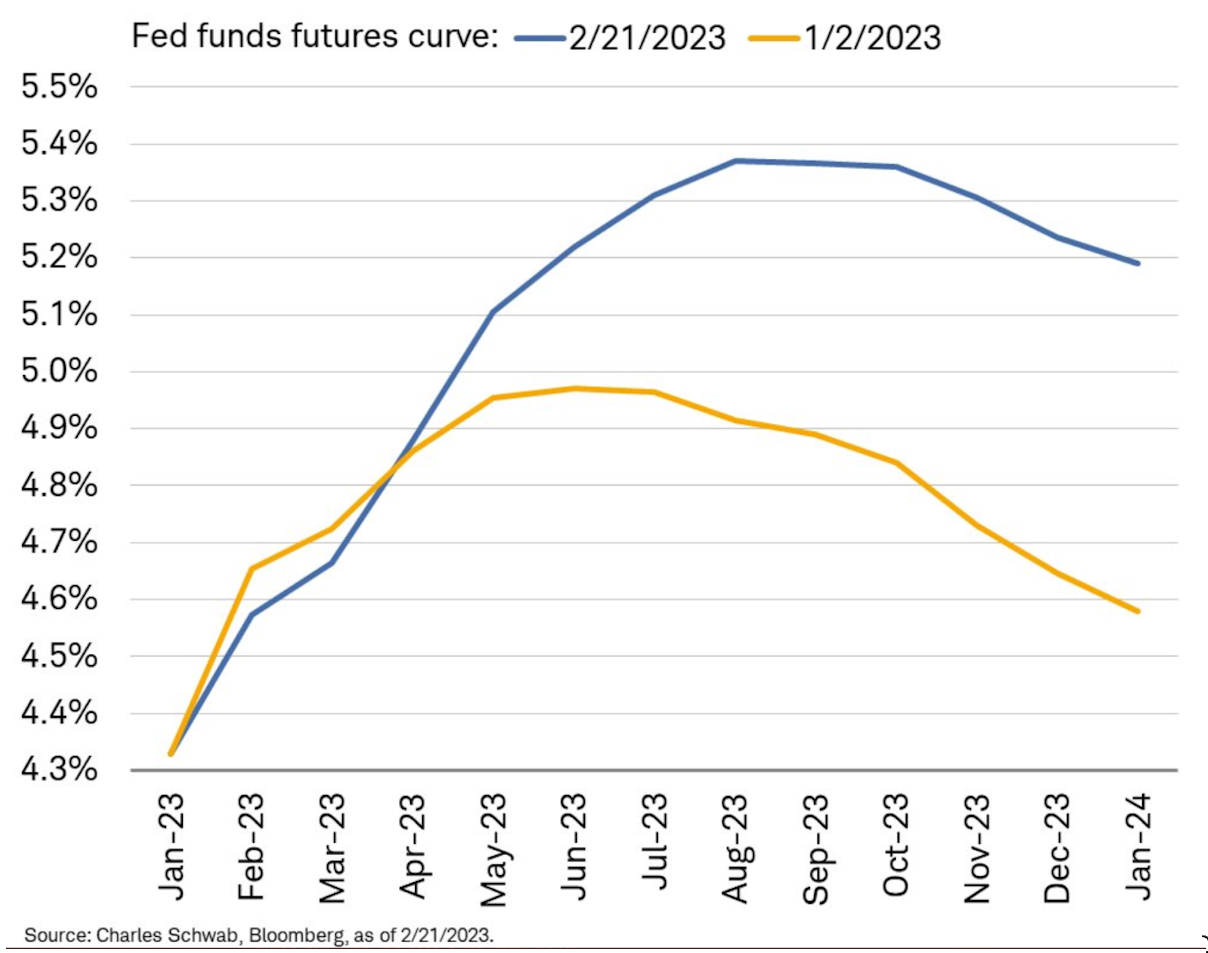

The market certainly took this CPI print as a sign that the vaunted “Fed Pivot” remains farther away than perhaps investors originally anticipated. The Fed funds futures curve is now showing that market participants expect a higher terminal rate at around 5.35% and for the Fed to not begin until the Fall of 2023.

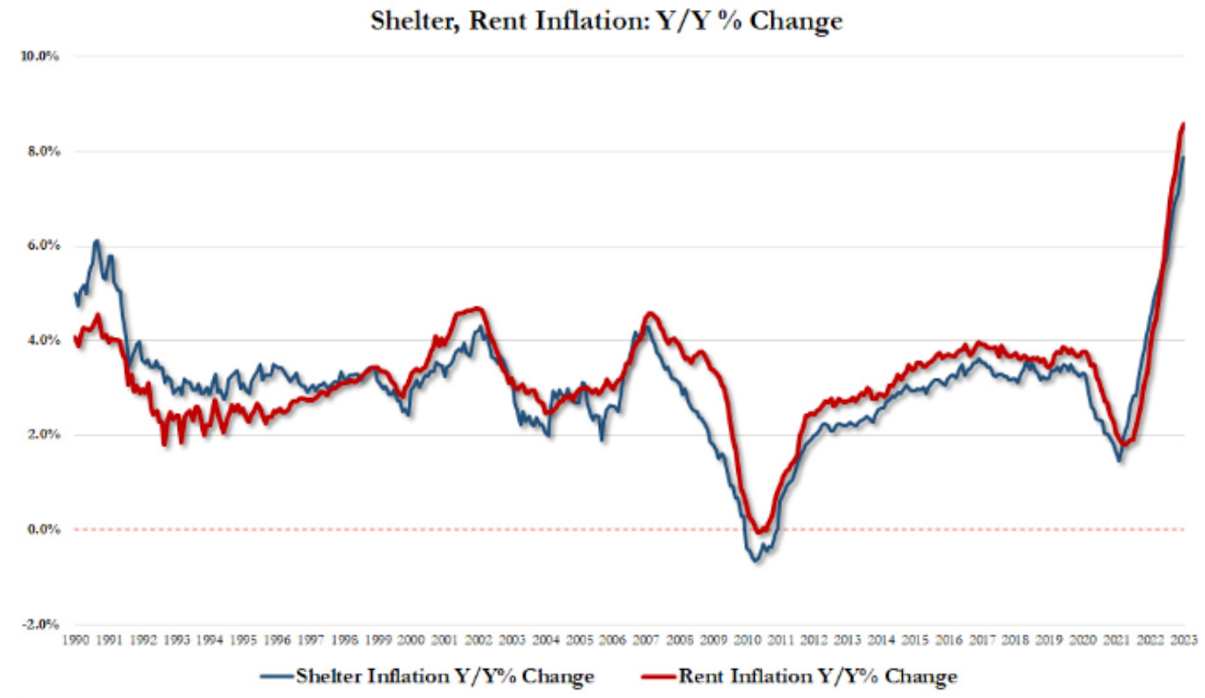

It was also noteworthy that the shelter component of the CPI basket was by far the largest contributor to the monthly headline increase, accounting for almost 50% of the monthly all-items increase.

This CPI print comes in as housing prices, housing sales, and rents have steadily declined in this new high-interest-rate environment.

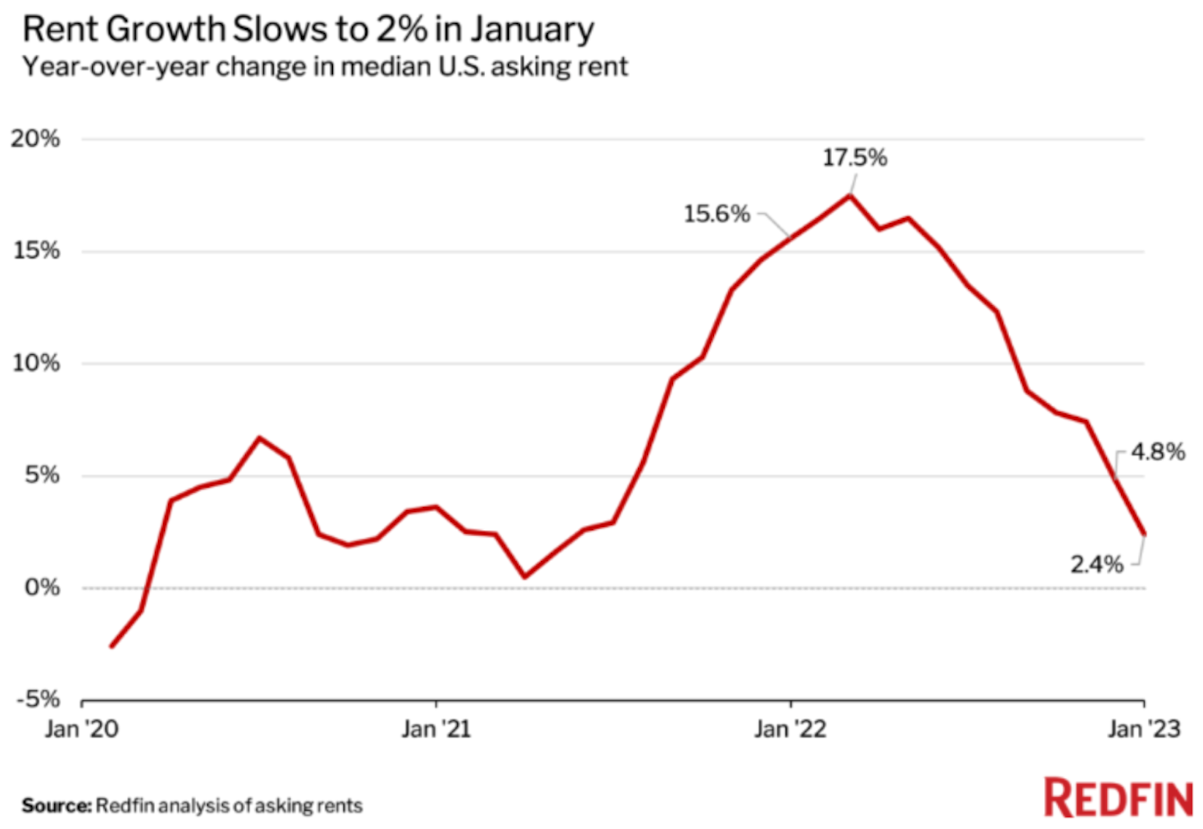

Rent growth has finally started to slow to begin the year.

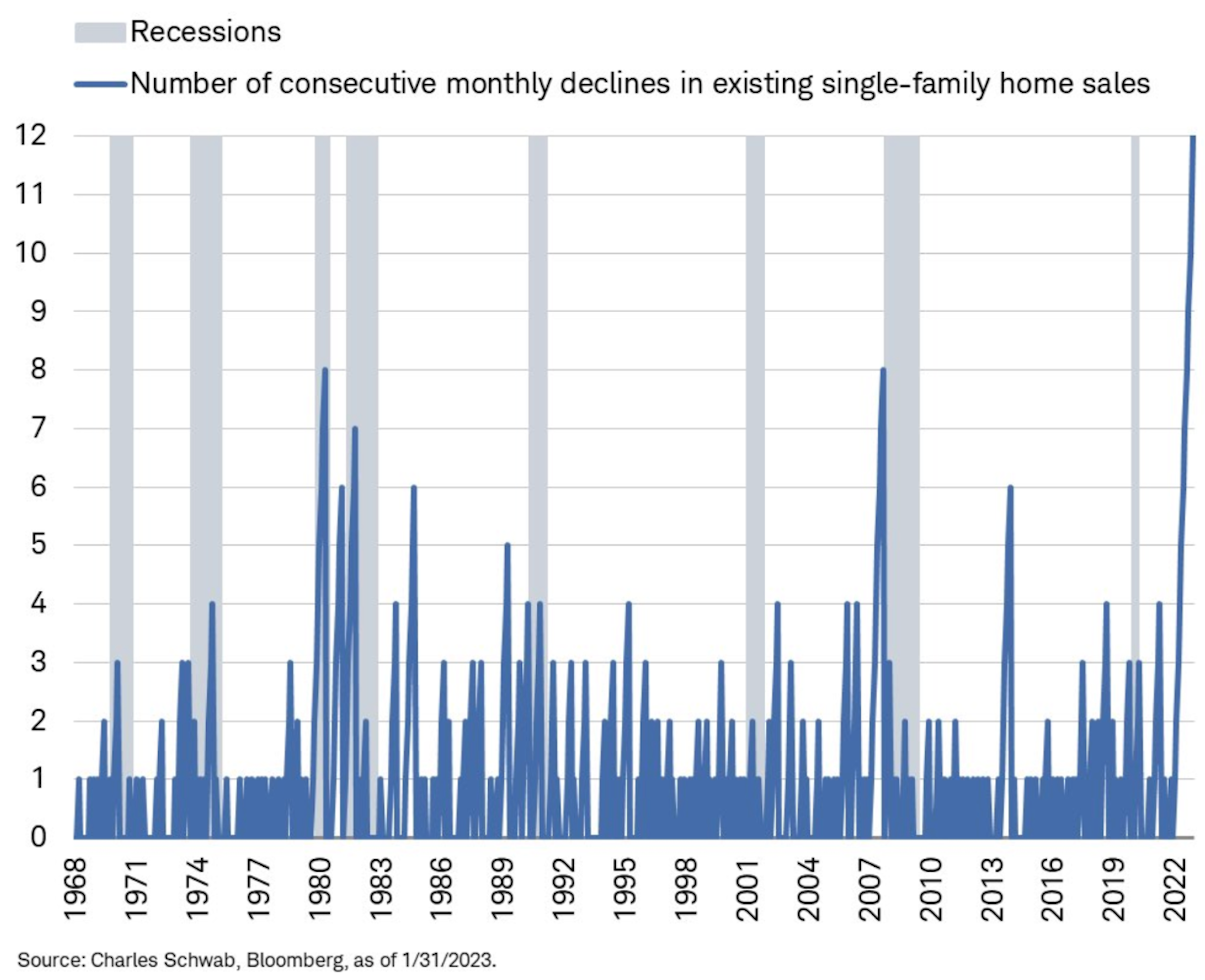

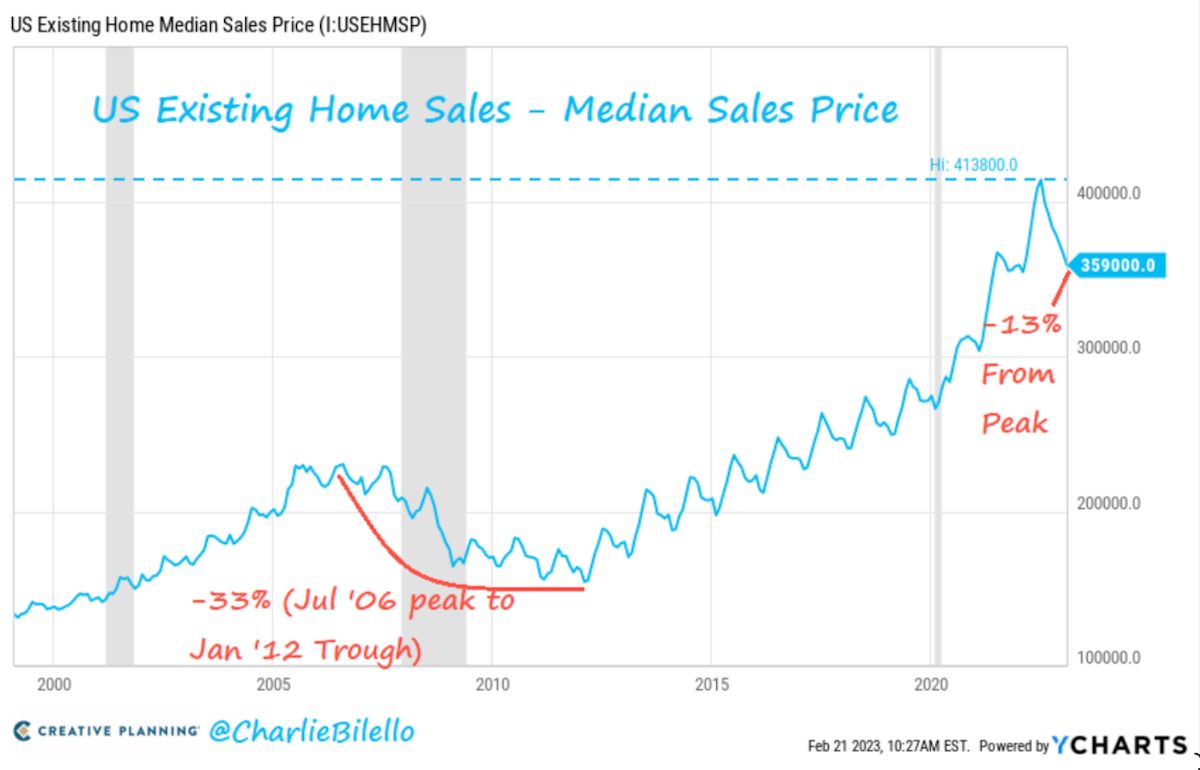

Home sales fell for a 12th consecutive month in January, the longest streak dating back to the 1960s.

It appears households that locked in a low, fixed-rate mortgage are not jumping at the opportunity to move to a new home when the average national 30-year mortgage now sits at 6.88%.

Due to low demand, house prices are beginning to fall even though this has yet to show up in the headline CPI numbers. The median U.S. home sales price has declined 13% from its peak and now sits at $359,000.

Due to the lagging effect of the shelter component of the CPI, this hints at the fact that the headline CPI is being propped up by shelter data that no longer reflects the present reality.

Given that the services sector continues to keep inflation sticky, we should expect the Fed to continue on its mission to bring inflation back down towards its 2% target by hiking rates further and holding them higher for longer. High rates should continue to put pressure on the housing sector, which eventually will show up in the CPI headline number.

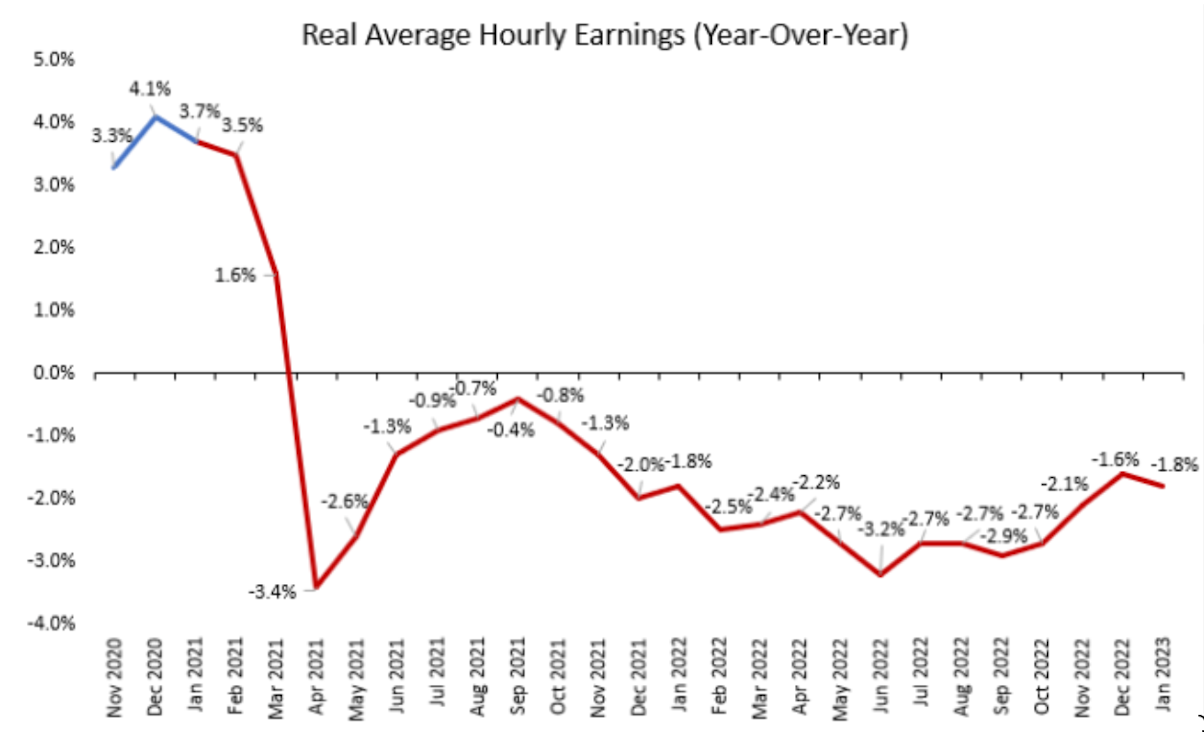

Speaking of wages…although wages continue to increase nominally, adding to the inflationary pressures, real wages YoY have been negative for 22 consecutive months.

BLS

Household wages are not keeping up with the pace of inflation. This loss in purchasing power will never come back. It is permanent, and it highlights why inflation is often labeled a “hidden tax.”

Despite CPI inflation remaining sticky, the growth rate has been declining for seven consecutive months. That brings us to the big debate that has been at the heart of the market for the last year or so, is this inflationary bout we are experiencing more structural in nature, or cyclical? In other words, is this inflation here to stay, or will we return to the pre-2020 trend of 1-3% inflation (at least based on the official CPI stats)?

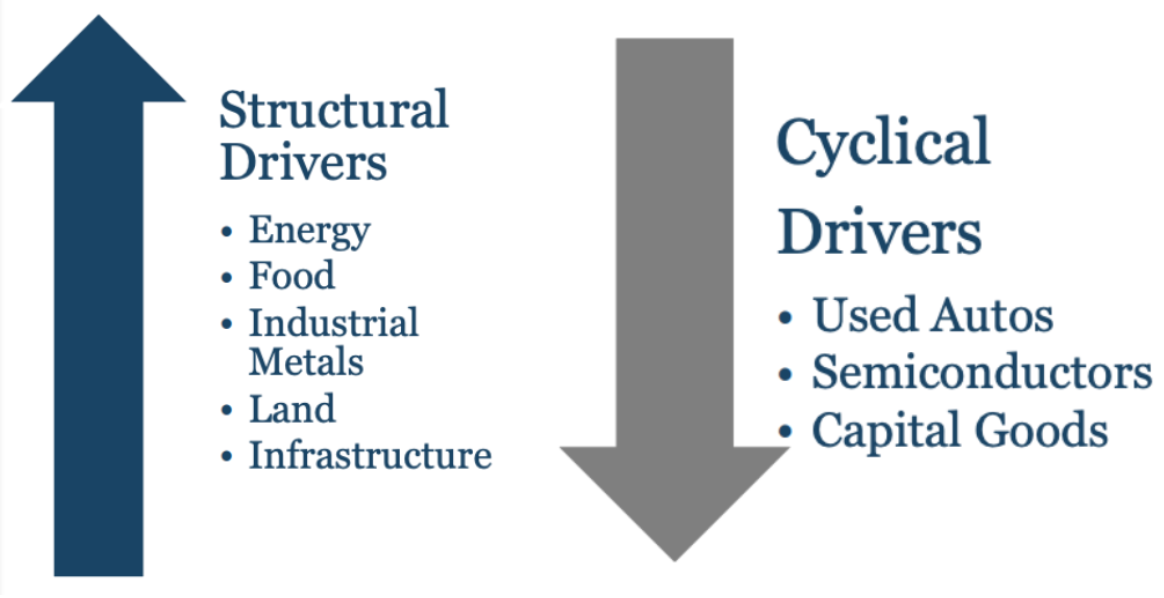

To answer this question, we need to consider what the structural and cyclical drivers of inflation are.

Structural inflation is driven by larger trends such as deglobalization, demographics (labor shortages), and slowing productivity due to underinvestment and falling education standards. These dynamics lead to supply-side constraints and increased scarcity in critical sectors like energy, food, industrial metals, and infrastructure.

Cyclical inflation is driven by things like the short-term credit cycle, pent-up demand, stimulus checks, abrupt changes in consumer behavior, and temporary supply chain disruptions that lead to shortages of items like semiconductors, capital goods, and used autos. These factors result in temporary price run-ups, and then the prices fall back down when supply and demand come back into equilibrium.

Horizon Kinetics

We have recently seen the price of used autos and semiconductors spike, and now they are coming back down, which has contributed to this fall in CPI inflation, but this may not be the time to claim victory over inflation just yet.

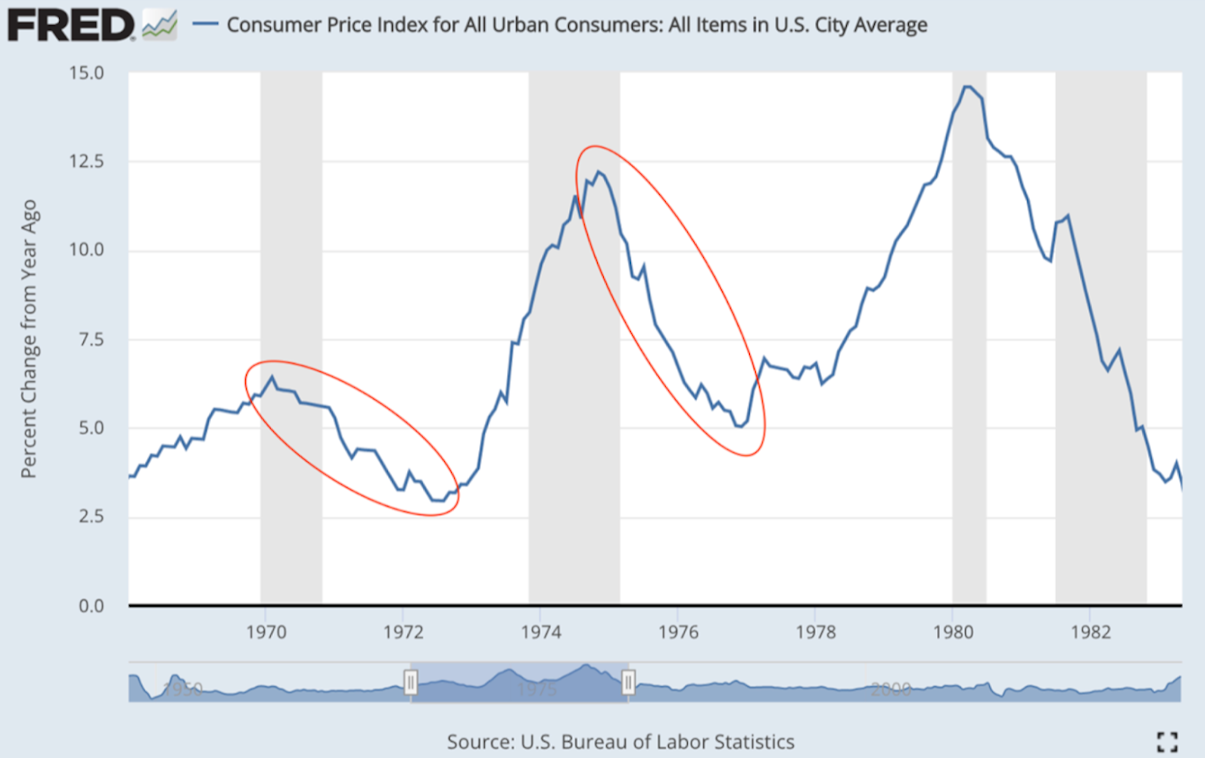

One only needs to look at a chart of the 1970s to see that there were years of disinflation where policymakers prematurely declared victory on inflation, only to see it come roaring back because of structural reasons. And keep in mind we are talking about disinflation here rather than outright deflation. As you can see in the chart below, the annual rate of CPI growth never fell below 2.5% for the entire 1970s decade.

Could this coming decade prove to be similar? Let’s look at some of the potential structural drivers of inflation…

Following decades of globalization, this trend is now reversing rapidly as global trade relations are breaking down, and now countries are beginning to rethink their supply chains. Globalization led to cheap labor, cheap raw materials, rising productivity, and low inflation. It is logical to expect deglobalization to have the opposite effects. Countries are now beginning to prioritize resiliency over efficiency in their supply chains, but this comes at a cost.

Since the pandemic began, the U.S. has been hellbent on reshoring critical infrastructure and manufacturing, like semiconductors.

The problem is that the reshoring of supply chains leads to higher manufacturing costs and takes years to become fully functional. This reshoring will lead to increased costs for consumers and structural supply shortages. This deglobalization trend is one main argument for why inflation will be structural in nature in the coming decade.

What about energy?

It is well known that the oil & gas sector has seen capital outflows and underinvestment in the last decade. Many energy analysts and industry insiders have been ringing the bell about the supply constraints that could lead to high energy prices for years to come, which would be inflationary.

The CEO of the largest oil producer in the world, Saudi Armaco, had a dire warning for the world last month,

“Today there is spare capacity that is extremely low,.if China opens up, [the] economy starts improving or the aviation industry starts asking for more jet fuel, you will erode this spare capacity.” — Saudi Aramco CEO Amin Nasser

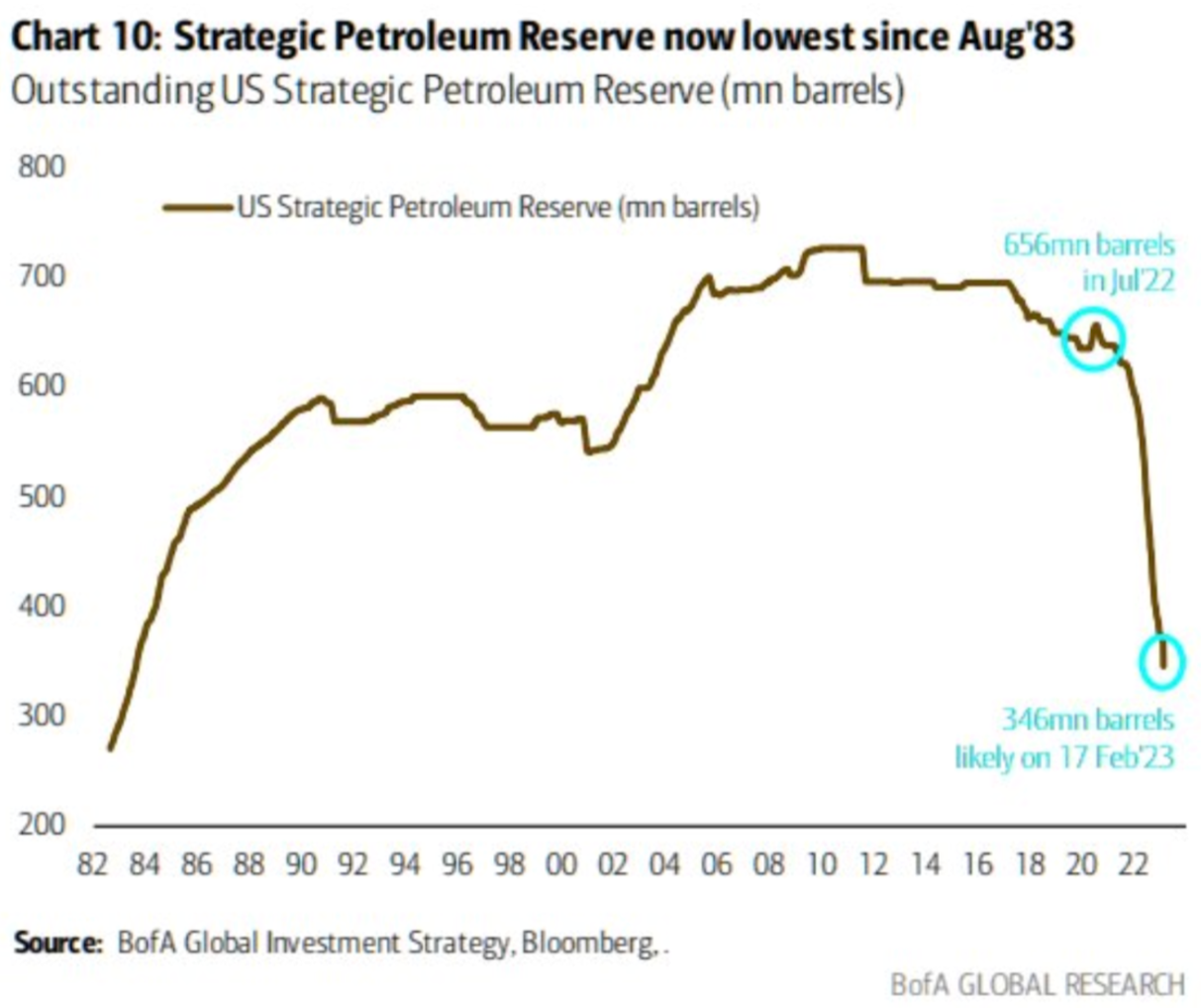

This warning comes as the Biden Administration recently sold 26 million barrels from the Strategic Petroleum Reserve after a 5-week pause to the selling. The SPR now sits at the lowest level since 1983.

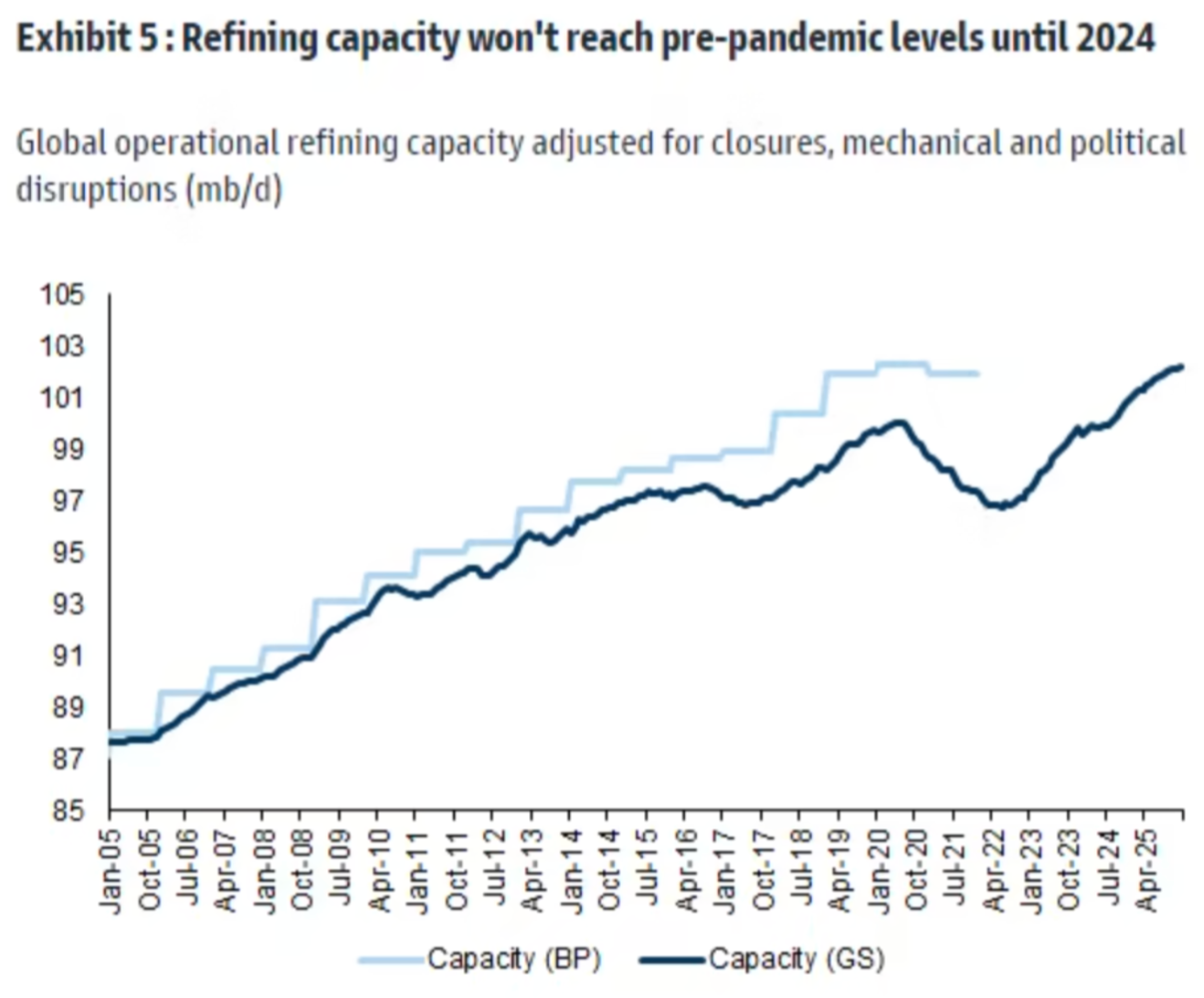

Not only is the available supply of crude oil apparently dwindling, the U.S. has also completely neglected to build out the infrastructure necessary to refine the oil into useable petroleum products like gasoline and diesel.

Here was Chevron CEO Mike Wirth last year on the matter, “We haven’t had a refinery built in the United States since the 1970s. My personal view is there will never be another new refinery built in the United States… You’re looking at committing capital 10 years out. That will need decades to offer a return for shareholders, in a policy environment where governments around the world are saying, ‘We don’t want these products.”

This problem isn’t isolated to the U.S. either. It is estimated that global operational refining capacity won’t reach pre-pandemic levels until 2024.

BP, IEA, IIR, Bloomberg, Goldman Sachs Global Investment Research

The price of WTI crude oil has been in steady decline since it peaked in June 2022 at $120/barrel and now sits at $75/barrel. But according to Goldman Sachs, this relief should not be considered long-lasting when one considers that China’s economy appears to be reopening, which will likely add more demand to the equation. Goldman Sachs states that this decline in oil prices will be short-lived because of “underinvestment, shale constraints, and OPEC discipline ensure supply does not meet demand.”

Structural supply shortages in energy will likely be a huge contributor to whether or not inflation will prove to be sticky or transitory in the coming years.

What about infrastructure?

When we fail to invest in our infrastructure, we pay the price. For too long now, the U.S. government has neglected its roads, dams, bridges, airports, and electric grid. Aging, decaying infrastructure results in increased transportation times and decreased productivity, which translates to higher costs for businesses to manufacture and distribute goods and services. These higher costs, in turn, get passed on to households in the form of inflation.

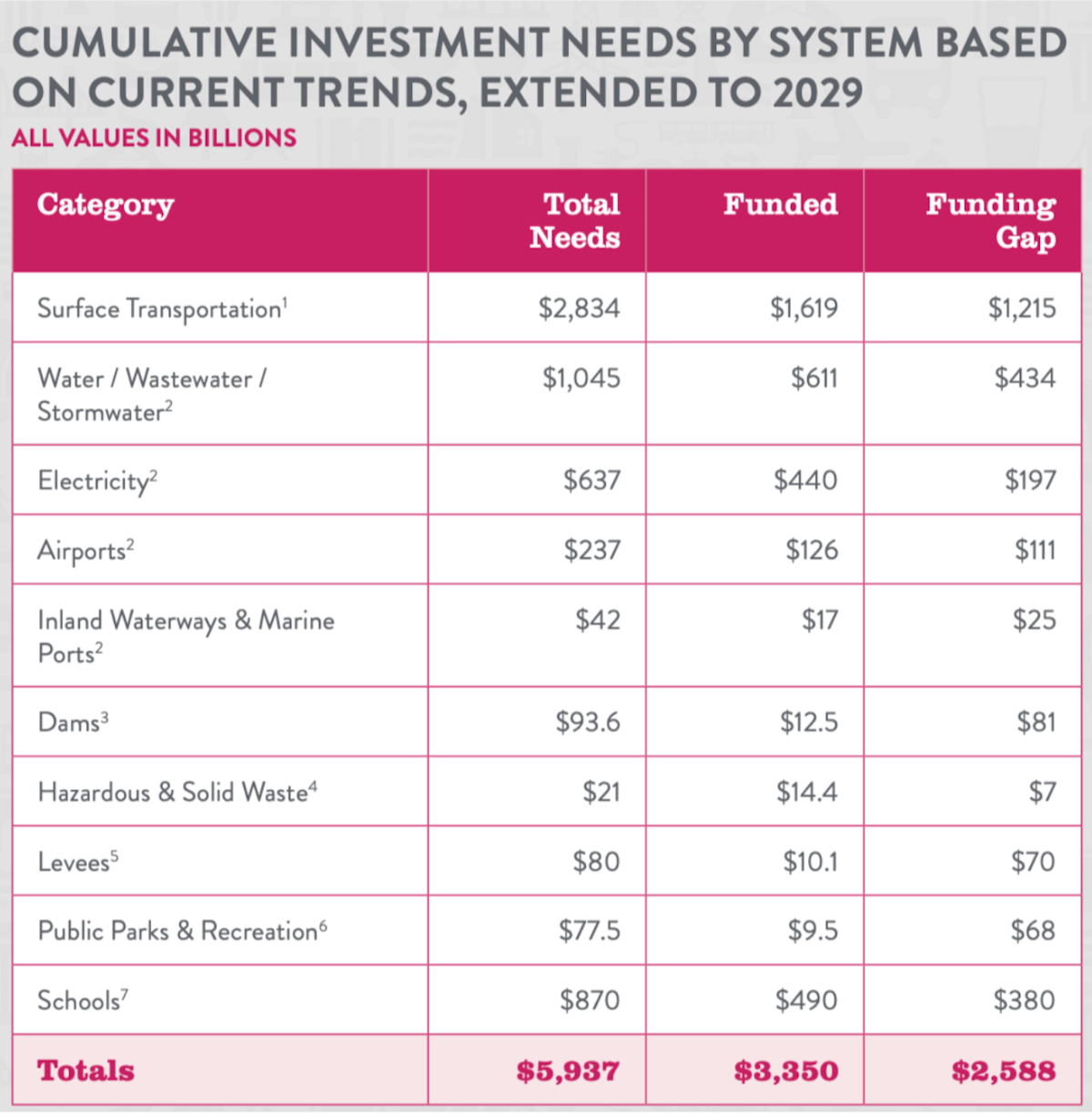

According to the American Society of Civil Engineers (ASCE) recent 2021 report card on America’s infrastructure, America was given a “C-.” The ASCE also acknowledged a huge funding gap when it comes to our infrastructure and wrote that a “failure to close that gap will have severe economic consequences.”

Today, the funding gap to bring our infrastructure up to a “B” grade is estimated to be $2.6 trillion dollars.

ASCE

Lack of investment in infrastructure is a driver of inflation both because of the inefficiencies in commerce and trade that it brings about, but also because of the government spending that will be required to fix it. Just last year, a $1.2 trillion dollar infrastructure bill was passed to address these needs.

Spending can be aimed at long-term investment in productivity, enhancing infrastructure, and research & development. This eventually has a deflationary effect. As long as productivity exceeds wage gains, then there is no lasting inflationary impulse. If investment is done wisely, added productivity will subdue inflation. If investment is done poorly, then it will only lead to more problems. Time will tell whether or not the government will be able to allocate these funds effectively to reverse this trend. Historically, let’s just say the government doesn’t have a good track record when it comes to allocating capital.

Our decaying infrastructure is another reason why inflation may prove to be stickier than many market participants believe.

When you combine all of these trends — the deglobalization, the energy supply constraints, and the underinvestment in our infrastructure– it all supports the argument that inflation will be more structural in nature this decade. The recent disinflation we are seeing in goods and services reflects the cyclical drivers of inflation rolling over, but the structural drivers of inflation remain. It’s important to remember what happened in the 1970s and don’t miss the forest for the trees. These structural dynamics and big trend changes are likely to result in higher costs and higher prices for years to come. So what are investors to do to protect themselves?

If inflation persists, investors would want to sell paper assets and buy hard assets such as real estate, gold, fine art, and Bitcoin, as well as allocate funds to equities with underlying hard assets such as oil and agriculture. But out of all of these options, only one has an absolute fixed supply and the asymmetric upside of an emerging technology. In addition, Bitcoin is the first digital hard asset, which gives it unique benefits such as portability and resistance to confiscation. These traits make Bitcoin an enticing opportunity for investors in this environment.

Bitcoin has started 2023 with a bang, up +41% YTD, but we expect more chop as the inflation outlook remains volatile and uncertain. At Swan, we continue to advocate for long-term thinking and long-term saving. If inflation proves to be structural in nature, Bitcoin will likely be one of the primary beneficiaries as it continues to be adopted as a hard monetary good around the world.

Market Overview

Tradingview — Prices as of 02/24/23

If you are planning to transfer or rollover more than $50,000, one of our Swan Private advisors will assist you. Get started here.

Sam Callahan is the Lead Analyst at Swan Bitcoin. He graduated from Indiana University with degrees in Biology and Physics before turning his attention towards the markets. He writes the popular “Running the Numbers” section in the monthly Swan Private Insight Report. Sam’s analysis is frequently shared across social media, and he’s been a guest on popular podcasts such as The Investor’s Podcast and the Stephan Livera Podcast.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

Live video verification, Jade Plus signing devices, and a purpose-built recovery assistant give families and businesses greater control over their Bitcoin.

Passkeys enable faster, more secure device-based logins (face/fingerprint) that reduce password risks and strengthen our Swan Guard security protections.

Swan Generations provides a unique service for parents, legal guardians, and others to make irrevocable gifts of real Bitcoin.