Swan Bitcoin IRA

Bitcoin is the ultimate asset for your retirement. Create a tax shelter for exponential returns! Get started in less than 2 minutes. Book a call with one of our Bitcoin IRA specialists today!

This is the first article in a series from Swan Research, our new department focused on bringing deep research and analytics to Bitcoin. This team is led by our Chief Investment Officer, Rapha Zagury, who joined Swan earlier this year. Previously he ran a few desks at Wall Street in major firms like Goldman and Merrill while covering some of their largest clients. After leaving New York and Wall Street, he founded a couple of companies including OpenCo, one of the largest credit fintechs in LATAM. In true Bitcoin spirit, Rapha will be open-sourcing his models and tools so you can run the numbers yourself.

Let’s get straight to the point.

You want to maximize the value of your retirement portfolio so you can enjoy life to the fullest without worrying about your finances, right?

Great. We’re on the same page.

The next question is: Should you hold Bitcoin in a retirement savings vehicle such as an Individual Retirement Account (IRA)?

We believe the answer is YES simply because holding Bitcoin may increase the expected returns of your retirement portfolio. In this article we’re going to cover:

Bitcoin is the ultimate asset for your retirement. Create a tax shelter for exponential returns! Get started in less than 2 minutes. Book a call with one of our Bitcoin IRA specialists today!

When planning for retirement, exploring ways to reduce your tax burden is important. After all, the more you pay in taxes, the less you have left over to enjoy your life.

An Individual Retirement Arrangement (IRA) is a tax-advantaged savings vehicle held by individuals in the U.S. While this article is focused on American retirement accounts, similar options exist in other countries.

Most Americans are familiar with 401(k) plans, similar to an IRA, except they are issued through your employer. When you leave that employer, you can “rollover” your 401(k) balance into an IRA you control.

This article will briefly explain the benefits of leveraging tax-advantaged retirement vehicles. However, the primary focus will be on two things…

Why Bitcoin deserves a place in every retirement portfolio

What percentage should you allocate to Bitcoin

The primary benefit of an IRA (Traditional, Roth, etc) is the potential for tax savings. The less of your money that goes to taxes, the more you have to enjoy your retirement.

Depending on your IRA type, the potential tax benefits will look slightly different. We’ll explain the differences in the next section.

Another key benefit of long-term savings vehicles such as an IRA is compounding returns.

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.”

- Albert Einstein

The longer your money has to grow, the more powerful the compounding effects will be. So, start investing as soon as possible, and let time and compounding work their magic.

With a Traditional IRA, you contribute pre-tax income. Below certain income thresholds, you can deduct your contributions from your taxable income in the tax year you make them, which can reduce your tax bill for that tax year. Since you didn’t pay taxes on the way into your Traditional IRA, you will owe taxes on the money when you withdraw it in retirement.

If you withdraw money from a Traditional IRA before age 59 ½, you may owe a penalty in addition to any taxes owed.

With a Roth IRA, you contribute post-tax dollars. This means you don’t get an immediate tax deduction. However, any earnings within the account grow tax-free, and you won’t owe taxes on qualified withdrawals in retirement. In addition, you can withdraw your contributions (but not the earnings) at any time without owing taxes or penalties.

Anyone with earned income (such as a salary or wages) can contribute to an IRA. This includes both Traditional and Roth IRAs, although there are some income limitations for Roth IRAs. In addition, if you are married, you can contribute to an IRA even if you don’t work, as long as your spouse has earned income.

For 2023, traditional and Roth IRAs' maximum annual contribution limit is $6,500, or $7,500 if you are 50 or older. This amount can be split between different types of IRAs or other accounts as long as the total contribution doesn’t exceed the annual limit.

A 401(k) is an employer-sponsored retirement plan. Like Traditional IRAs, you contribute with pre-tax income. Many employers will match employee contributions, which is an excellent incentive. When you leave the company that sponsored your 401k, you can convert it into a Traditional IRA you manage.

Many 401k plans restrict what assets you can hold. Employers give you a short list to choose from, and everything else is off-limits. However, if you convert your 401k into a Traditional IRA, you will have full control over what assets you want to invest in. You know, in case you wanted more Bitcoin ;)

Additionally, there are no tax implications for converting your 401k to a Traditional IRA, so long as the funds are rolled over within 60 days from one account to another.

If you have a retirement portfolio, consider adding Bitcoin. While Bitcoin is often associated with volatility and risk, there are several reasons why it makes sense as a long-term investment.

Bitcoin gains can grow tax-deferred (IRA) or tax-free (Roth IRA)

Bitcoin increases your asset diversification (reduces correlation to other assets)

Bitcoin may increase your risk-adjusted returns

Bitcoin may help protect you from the effects of inflation (monetary debasement)

Assets with high expected returns (as we believe with Bitcoin) work well in an IRA because any price appreciation will grow tax-deferred (or tax-free in the case of a Roth IRA).

Peter Thiel famously bought seed stage equity in Facebook inside his Roth IRA. Thiel started his Roth IRA in 1999 with less than $2,000; by 2021, it was worth over $5 billion.

The best part? Because he owned Facebook stock inside this Roth IRA, the earnings are tax-free, which would save him about $1 billion by avoiding capital gains tax if he retired today.

Most people have a standard 60/40 allocation in their retirement accounts. This means 60% stocks and 40% bonds. Typically, stocks and bonds are “inversely correlated, ” which means when stocks are going down, bonds are going up, and vice versa. This is a diversification strategy designed to minimize risk while maximizing returns. Historically, this has made sense.

Do you know what increases your diversification even more? Yep, you guessed it, Bitcoin.

This is because Bitcoin has a low correlation to traditional assets like stocks and bonds. The end result is your overall portfolio may have better risk-adjusted returns with Bitcoin in the picture.

Remember that standard 60/40 portfolio? If you invest in the standard retirement portfolio, your expected annual returns would be around 7%.

Not bad. Now let’s compare that to Bitcoin…

Although past performance does not guarantee future results, it is worth noting that since its inception in 2009, Bitcoin’s price has increased by an average of over 100% per year. While there have been periods of volatility and sharp price declines, the long-term trend has climbed higher and higher.

This doesn’t necessarily mean you should all-in on Bitcoin in your IRA. Even adding a small allocation to your retirement account can make a big difference.

In the next section, we’ll run the numbers to show the returns we may potentially see after adding Bitcoin to our portfolio.

In addition to its potential for high returns, Bitcoin can help preserve your purchasing power in the face of inflation.

Inflation can have a massive impact on the purchasing power of your money over time. For example, the purchasing power of $1 in 1913 is now worth less than 3 cents due to inflation.

This is caused by central bankers continually printing more money. When the growth of the money supply outpaces the growth of real goods and services, we see price inflation.

By contrast, Bitcoin has a fixed maximum supply (21 million) that cannot be inflated away. This means it can help protect against the debasement of fiat currencies like the U.S. Dollar.

However, it’s important to note that while Bitcoin can protect against inflation over the long term, there is no correlation between Bitcoin and short-term inflation. In fact, Bitcoin’s price can be volatile in the short term due to various factors such as market sentiment, regulatory changes, and technological developments.

Adding Bitcoin to your IRA can potentially provide diversification, higher returns, and protection against the effects of inflation over the long term.

However, as with any investment, it’s essential to do our research, understand the risks involved, and consult with a financial advisor to determine if Bitcoin is a suitable addition to your portfolio.

Hold your IRA with the most trusted name in Bitcoin.

Ok, now that you’re convinced Bitcoin deserves a place in every retirement plan/portfolio, let’s talk about what % allocation makes sense…

Alright, let’s see what may happen to your returns after adding BTC to your retirement portfolio.

We will use our open-source Bitcoin Retirement Calculator to help us run the numbers. Feel free to enter your own assumptions. This is part of a new initiative called Swan Research (more on that below).

We’re going to analyze 3 common scenarios we’re hearing from our clients (names are anonymized)

Hal: 25-year-old Bitcoin mega Bull setting up his first IRA

Alice: 35 years old, 2 kids, moderate savings, and bullish on Bitcoin but needs to stay diversified

Bob: 55-year-old, successful career, healthy savings, wants some Bitcoin exposure but cannot justify excessive risk this close to retirement age

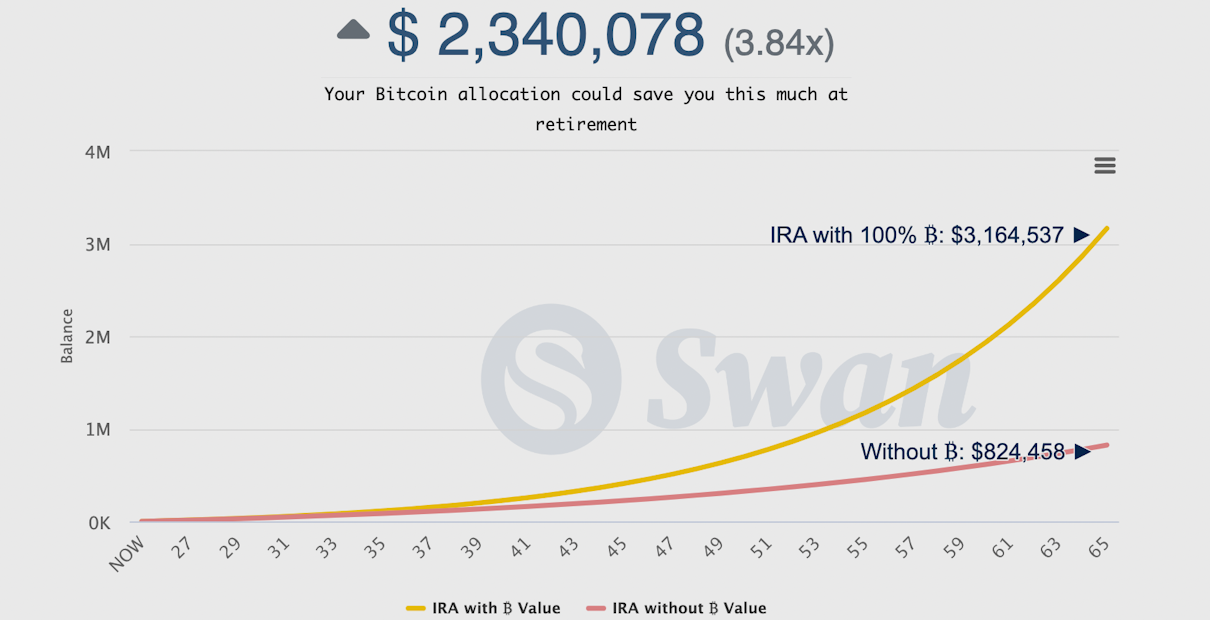

Hal is 25 years old, single, and just got his first “real job.” He has no savings but decided to set up his first IRA. He has about 40 years to invest before retirement and has a high-risk tolerance.

Hal expects an annual return of 10% from Bitcoin and 7% from a 60/40 portfolio, respectively. He anticipates that the price of Bitcoin at the time of his retirement in 2063 will be $1.3 million.

Hal expects his 60/40 portfolio to have an annual return of 7% over the next 40 years. He expects Bitcoin to hit $1.3M by retirement (2063) which reflects a projected average annual return of 10%.

After running the numbers based on his projected Bitcoin price at retirement, Hal discovered that if he allocates 0% of his portfolio to Bitcoin, he can expect to have $824k by the time of his retirement. On the other hand, if he invests 100% of his IRA in Bitcoin, he can expect to have $3.2 million by retirement (3.8x more money) should Bitcoin reach or exceed his projection.

Hal is optimistic about Bitcoin’s future growth potential and has decided to allocate 100% of his IRA to Bitcoin. He understands the risks associated with investing in a volatile asset and is willing to accept them in pursuit of achieving his financial goals. By doing so, he hopes to accumulate a larger retirement fund, which he can use to enjoy his golden years.

Assumptions for Hal:

25 year old, single

Planning to retire at 65 (40-year time horizon)

IRA starting balance of $0

$6,500 annual contribution

Projected annual returns (BTC) = 10%

Projected annual returns (60/40 portfolio) = 7%

Projected BTC price by time of retirement (2063) = $1.3M

Running the Numbers:

With a 0% allocation to Bitcoin, Hal expects to have $824k by retirement

With a 100% allocation to BTC, Hal expects to have $3.2M by retirement

$2.3M more in his retirement account (3.8x more money) should these projections become true

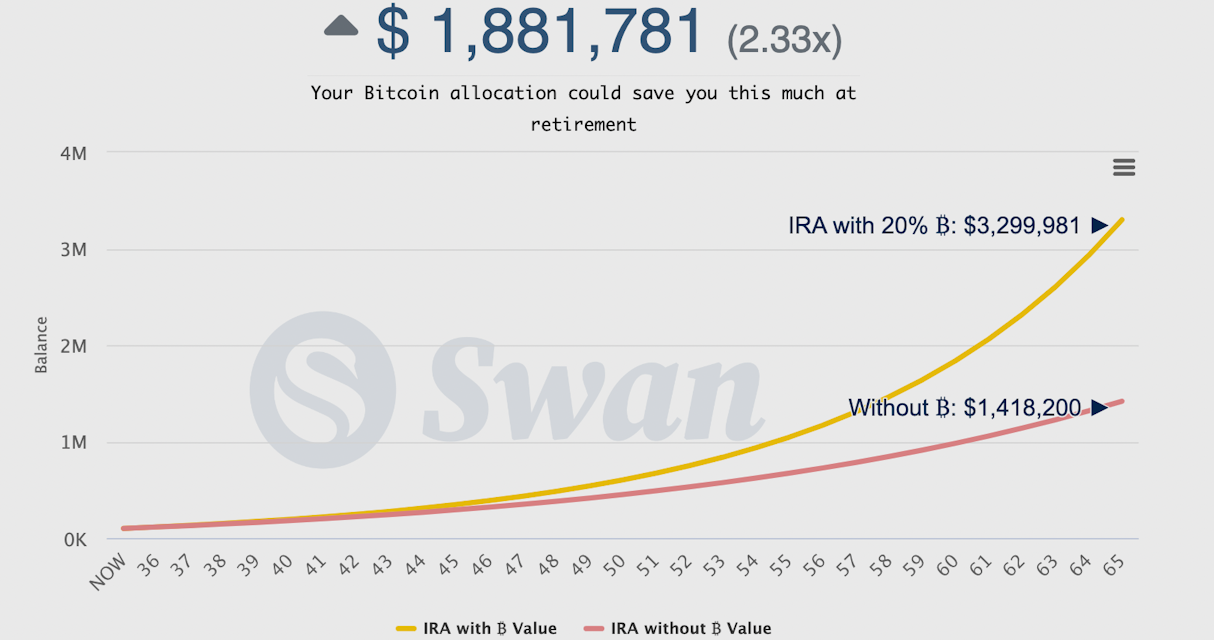

Alice is a 35-year-old married woman with two kids who is interested in investing in Bitcoin. She already has a moderate amount of savings and is bullish on the future prospects of Bitcoin. However, she wants to maintain a well-diversified investment portfolio.

Alice currently has her retirement account invested in a standard 60/40 portfolio. She expects it to return 7% annually on average.

Alice makes some assumptions to evaluate the potential benefits of adding Bitcoin to her investment portfolio. She plans to retire at the age of 65, which gives her a 30-year investment horizon. She estimates that Bitcoin will reach $1.9M by her retirement in 2053, reflecting a projected annual return of 15%.

After running the numbers based on her projected Bitcoin price at retirement, Alice discovers that if she maintains a 0% allocation to Bitcoin, she can expect to have $1.4M in her retirement account by the time she retires. However, if she adds a 20% allocation to Bitcoin, she can expect to have $3.3M (2.3x more money) in her retirement account, should Bitcoin reach or exceed her projection, while still maintaining a diversified portfolio.

Assumptions:

35 years old, married with 2 kids

Retiring at 65 (30-year time horizon)

IRA starting balance of $100k

$6,500 annual contribution

Projected annual returns (BTC) = 15%

Projected annual returns (60/40) = 7%

Projected BTC price by time of retirement (2053) = $1.9M

Alice currently has her retirement account in a standard 60/40 portfolio however she wants to add a 20% allocation to Bitcoin

Running the Numbers:

With a 0% allocation to Bitcoin, Alice expects to have $1.4M by retirement

With a 20% allocation to Bitcoin, Alice expects to have $3.3M by retirement

$1.8M more in her retirement account (2.3x more money) should these projections become true

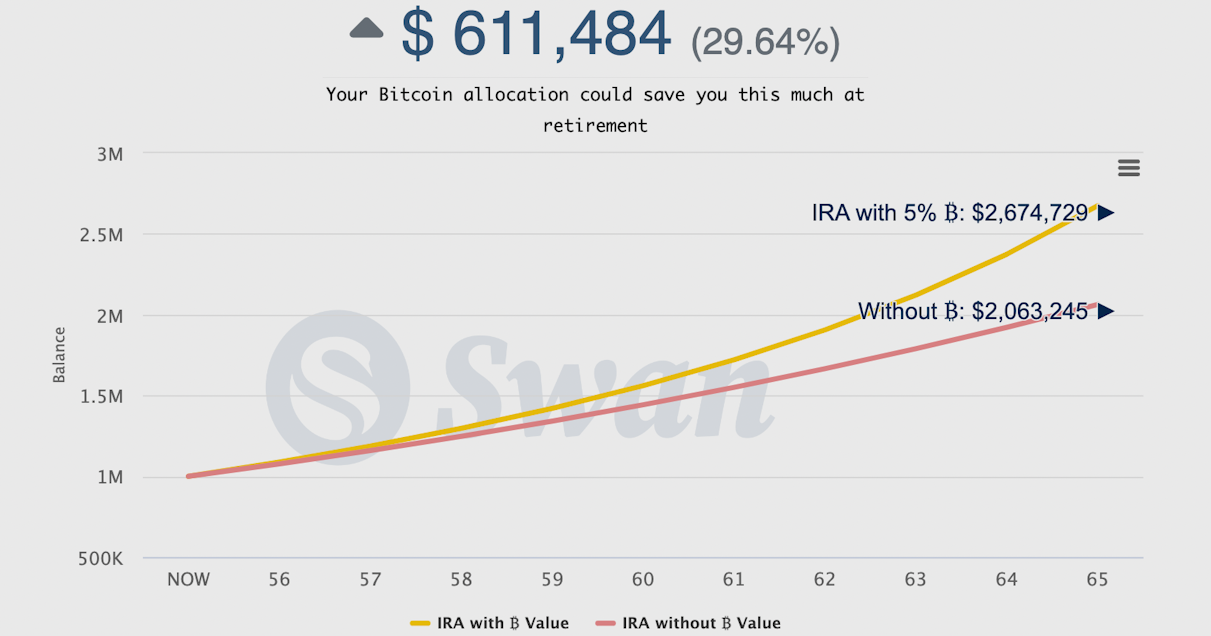

Bob is a 55-year-old individual who is married and has seen his children graduate from college. Bob has been diligently saving for retirement and has a starting IRA balance of $1 million. He plans to retire by age 65, which is only 10 years away. He is looking for investment options that can help him maximize his returns to secure a comfortable retirement.

Bob’s current portfolio comprises a standard 60/40 mix of stocks and bonds. However, he is considering adding a 5% allocation to Bitcoin. Bob believes that Bitcoin can provide him with the potential to earn higher returns than traditional investments.

Bob expects his 60/40 portfolio to have an annual return of 7% over the next 10 years. He projects Bitcoin to hit $400k by 2033, which reflects an average yearly return of 30%. Since Bitcoin has averaged over 100% annual returns over the last decade, and while understanding that past performance does not guarantee future results, he also thinks 30% is a conservative assumption.

By managing his initial position size (5%), Bob hopes to boost his overall portfolio returns while offsetting the volatility associated with Bitcoin.

Assumptions for Bob:

55 year old, married filing jointly, kids already graduated from college

Retiring at 65 (10-year time horizon)

IRA starting balance of $1M

$6,500 annual contribution

Projected annual returns (BTC) = 30%

Projected annual returns (60/40) = 7%

Bitcoin price by time of retirement (2033) = $402k

Bob currently has his retirement account in a standard 60/40 portfolio however he wants to add a 5% allocation to Bitcoin

Running the Numbers:

With a 0% allocation to Bitcoin, Bob expects to have $2.1M by retirement

With a 5% allocation to Bitcoin, Bob expects to have $2.7M by retirement

$611k more in his retirement account (30% more money) should these projections become true

We cannot provide financial advice. Even if we could, choosing your Bitcoin allocation depends on your time horizon, personal goals, conviction, and risk tolerance.

Hopefully, the three scenarios above have helped you envision how Bitcoin might make sense for your retirement planning.

If you want to play around with different scenarios, we encourage you to run the numbers yourself using parameters that would make sense based on your anticipated retirement age, desired allocation and projected Bitcoin price.

Want to run the numbers for yourself?

As part of Swan Research, our Bitcoin retirement calculator is open-source. Feel free to play around with the model.

If you have questions about the model or adding Bitcoin to your IRA, email me at Rapha@swan.com.

Here at Swan, our mission was simple: let’s create the best Bitcoin IRA product on the market.

This means easy to use, enterprise-grade custody, simple and transparent fees, and best-in-class service.

Learn more about Swan IRA here.

Setting up a Swan Bitcoin IRA is quick and easy

Create a Swan Account (if you don’t have one already)

Open a Swan IRA (2 clicks)

Fund your account with a Transfer, Rollover, or contribute directly via ACH, wire transfer, or direct deposit

Swan Research builds on Swan’s mission of driving adoption and education by providing tools, research, and open-source code that explore Bitcoin’s groundbreaking effects on the financial world.

This project acts as a lab for experimenting with new and sophisticated ideas to make them available to everyone. The team at Swan Research is dedicated to pushing the boundaries of what is possible with this revolutionary technology.

Through Swan Research, users can explore cutting-edge ideas related to Bitcoin, including new investment strategies, alternative financial models, and innovative ways of understanding Bitcoin. Based on the Open Source ethos, the project is available to anyone interested in Bitcoin and wanting to learn more about this fascinating technology. Whether you are a seasoned Bitcoin investor or just getting started, Swan Research is an exciting new resource providing valuable insights and opportunities.

Have an idea for a model we should build? Email me at Rapha@swan.com or send me a DM on Twitter @alphazeta.

An IRA can be a valuable tool for saving for retirement and building wealth over time. Whether you choose a traditional or Roth IRA, the tax advantages and potential for compounding can help you achieve your financial goals.

Adding Bitcoin to your IRA can be a smart long-term investment strategy, as it can provide:

Diversification.

The potential for higher returns.

Protection against the effects of inflation over the long term.

However, it’s essential to understand and manage the risks involved, including volatility and custody.

By researching, seeking professional advice, and staying informed about market developments, you can decide whether adding Bitcoin to your IRA is right for you.

Ultimately, the key to building a successful retirement plan is to start early, stay disciplined, and be patient. With the right strategy and mindset, you can create a secure and prosperous future for yourself and your loved ones.

Hold your IRA with the most trusted name in Bitcoin.

This article is provided for educational purposes only, and cannot be relied upon as tax, accounting, legal, investment, or other advice. Past performance is not indicative of future performance. Bitcoin is a young, volatile, risky asset, and sudden large and sustained drops in price may occur from time to time. Swan makes no representations regarding the performance, tax consequences, or investment suitability of any structure described herein, and all such questions should be directed to a relevant advisor of your choice. The Bitcoin Retirement Calculator is only intended to show the projected investment performance based on parameters set by you, and in using this tool, you acknowledge that the results generated by placing various parameters through this tool are only projections of hypothetical performance that may be useful in assisting you in deciding how best to potentially incorporate a Bitcoin allocation in your IRA.

Rapha is the Chief Investment Officer and Head of Research at Swan Bitcoin. He previously spent his career on Wall Street as Managing Director of Deutsche Bank, and later as the Founder of Open Co.

Brandon is an entrepreneur, writer, speaker, and passionate Bitcoiner. His articles have been read by more than 2 million people online. Most well known for exploring the parallels between bitcoin and mycelium.

News

More NewsThoughts on Bitcoin from the Swan team and friends.

No longer a niche commodity, Bitcoin now finds itself a prime fixation of the US Executive Branch.

The SAB 121 repeal mirrors the end of Glass-Steagall in 1999, which played a major role in the 2008 financial crisis. Bitcoiners should listen to history and be more cautionary about SAB 122.